Some apparel licenses will prove massively unstable in '09 as licensees pull back on investing in content. Some will miss minimums, and will lose business that some currently think is a lock.

Here's an issue that people are not focusing on, but should be - the risk associated with stability in cash flows from licensing streams. The apparel industry is riddled with examples whereby content owners license out their brand to others that have more expertise in a specific product area or consumer segment. Standard royalty agreements are usually in the 6-10% range, net of costs allocated by corporate. In other words, what is a smallish revenue event translates to a meaningful EBIT event given 100% incremental margin. With zero capital at risk, such arrangements are almost always ROIC-enhancing.

I have a high degree of confidence that we are entering a phase of the cycle where these licensing relationships will be strained meaningfully. We'd all be irresponsible not to consider the strategic implications.

Think about it like this... Let's say you are a mid-size company whose EBIT is derived evenly between your own content and content you license from other companies. For the past 7 years, the industry has had every bit of wind at its back (import quota changes, FX, input cost deflation, strong consumer) such that everyone made money - even the marginal players. Now we're in a multi-year period where the opposite is a reality, and many mid-tier brands will go away. So now your top line is rolling, you've underinvested in your brands, flowed through too much FX and sourcing benefit to your bottom line instead of plowing back into your model. So now what? You're probably cutting costs reactively and irresponsibly to keep your head above water. Do you cut costs out of your own content? Or from what you were allocating toward another company's content that you licensed and ultimately will return to them? I'd challenge anyone to find me a company that would opt to damage its own content over another's.

CEOs of companies that license a meaningful proportion of their EBIT (PVH, GES, ICON, to name a few) will argue that there are fixed amounts that partners need to contractually invest each year, which is controlled in part by the company owning the brand. Yes, there are usually fixed dollar amounts or percentages that are required for reinvestment, but that ALL leave plenty of room for unhealthy behavior on the part of the licensee. Remember when Jones Apparel Group said that its Lauren, Ralph, and Polo Jeans business was fine and was 'locked up' for years? 'Nuff said. DCFs don't matter when a business segment you have in your model suddenly ceases to exist.

All it takes is some bad investments (or lack thereof) and a couple of quarters of missed minimums, and the content owners could usually take back the business at will.

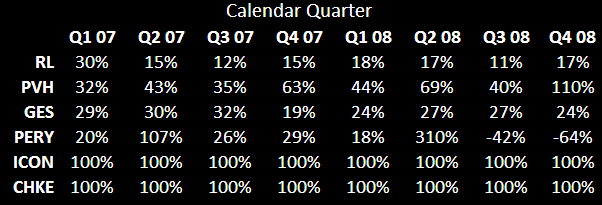

The table below shows the percent of EBIT for some major brands derived from licensing. Part There will be some big winners and big losers beginning in '09 folks...