Summary

FedEx announced the accelerated retirement of its old, high cost aircraft. Our thesis on FDX focuses on the FedEx Express restructuring opportunity. A key component of that restructuring is the need to eliminate high cost old aircraft. Broadly, we believe the Express restructuring is a meaningful inflection point in FDX’s operating history, as the company refocuses substantial attention and capital spending on improving Express margins. Today’s announcement appears to be a meaningful acceleration of that restructuring.

From our standpoint, the accelerated retirements are an extremely positive development. As long as the company is able to maintain adequate capacity and manage the accelerated schedule, the elimination of high cost aircraft should bring forward the margin improvement that is the core of our thesis. We have no doubt that the street will focus on what the retirements imply for the demand environment. That said, looking at the scale of the acceleration in retirements, it seems possible that there will be a subsequent announcement related to accelerated deliveries/contracted capacity/network restructurings that facilitated todays announced actions (i.e. it may not be all because of weaker demand.)

For what seems to be a very meaningful announcement, we would have preferred more specifics. However, anything that attacks FedEx Express’s cost disadvantage relative to competitors while rationalizing excess capacity should be a welcome development.

Positive: Should Have Been Done Years Ago, So Faster Is Better

Accelerating the retirement of 86 aircraft out of a fleet of a few hundred commercial jets is a very meaningful move. It also highlights the scale of FedEx’s high cost aircraft problem/opportunity. Further, by our count, FedEx still has over 20 727s, which are now scheduled for retirement by July 1, 2013. This move should pull forward substantial restructuring benefits.

While it is difficult to pin a number on exactly what the benefit of the accelerated retirements will mean for FY2014 without more specifics, we believe the improvement will be substantial relative to our former expectations. If we assume 30-35 incremental aircraft or so are retired before the end of FY2014, our first cut estimate is $300-$600 million in FY2014 savings relative to our previous expectations (we still had them with some 727s). That estimate could be low because of increased density in certain routes from capacity reductions. It is difficult to estimate the timing of the additional retirements from the information provided and we have not assumed a revenue impact from the retirements or any impact on pricing. As we get additional information, we will revise the estimated savings, but that is our best guess tonight.

Estimation error aside, our first cut estimate should emphasize the substantial scale of the renewal programs and the impact of the announced accelerated retirements. It will be interesting to see if FY 2014 estimates move higher as the street incorporates today’s announcement.

Negative: Suggests Demand Outlook Has Eroded

“We can accelerate retirements of the MD-10, the 727 or the A310 fleets, if demand erodes. If demand were to rebound significantly, we have the ability to operate these assets until incremental lift can be acquired.” David J. Bronczek 10/10/2012

This accelerated retirement schedule certainly may suggest that FedEx Express projects “slower economic growth than previously forecast.” While that may be seen as a negative, the operating environment for FedEx Express will be what it will be. At the margin levels achieved last quarter, there was so little profitability that Express really did not matter. Margin expansion is critical for FedEx Express and accelerated aircraft retirements should expand margins. Capacity reductions in the face of weak demand also tend to be rational.

However, it may not all be demand related. As indicated on the FYQ3 earnings call, network restructuring may have allowed for capacity reductions targeted at older aircraft.

“While FedEx Ground and FedEx Freight posted solid financial results, the third quarter was very challenging for FedEx Express due to continued weakness in international air freight markets, pressure on yields due to industry overcapacity, and customers selecting less expensive and slower-transit international services. In response, as Dave Bronczek will tell you after Alan Graf's remarks, beginning April the 1, FedEx Express will decrease capacity to and from Asia and will aggressively manage traffic flows to place lower-yielding traffic in lower-cost networks. We are assessing how these actions may allow FedEx Express to accelerate the retirement of more of its older, less-efficient aircraft as part of our fleet modernization program begun several years ago. We remain focused on our strategic cost reduction programs, which are ramping up and on target.” - Frederick W. Smith 3/20/2013

No Need for Ground/Express Integration

While some have called for the integration of the Express and Ground networks, we do not see a need for that. FedEx Express has plenty of scale in the Americas to compete. FedEx Express should attack its own costs structure, as it is doing, before risking the substantial labor cost advantages that FedEx Ground enjoys.

For Perspective…

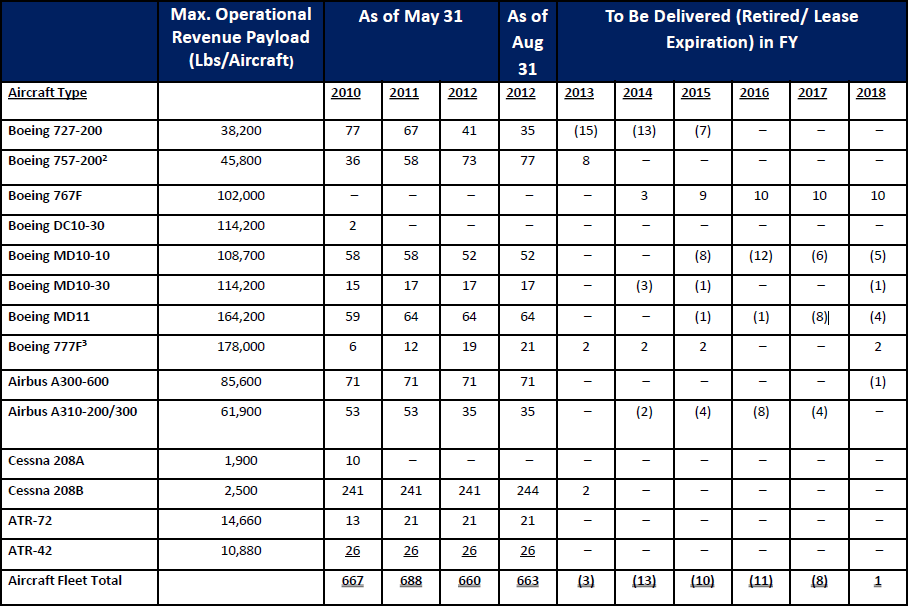

The table below shows an expected aircraft schedule as of November 2012. The changes announced today are likely to alter the schedule substantially.

Valuation

You can see here some of the reasons we do not like a simplistic sum of the parts valuation approach, but we find the estimates in the table below useful for understanding the opportunity inherent in the FedEx Express restructuring. The table suggests nearly 70% upside in FDX shares if the restructuring is successful and little downside if it is not (assuming FedEx Express does not start to lose meaningful amounts, which seems unlikely to us).