This note was originally published at 8am on May 20, 2013 for Hedgeye subscribers.

“I was very pleased to read a prediction that the price of gold will nosedive.”

-Ronald Reagan

Can you imagine if Obama got up in front of his old media paparazzi and talked about Gold like that? Reagan did in 1980. That’s because someone advising him actually understood the marketing message - #StrongDollar, Strong America. It’s pro-growth.

Instead of taking a victory lap on that and talking about the most bullish development in American Purchasing Power in a decade, let’s talk about how the IRS scandal is a “partisan fishing expedition designed to distract” Americans.

Distract us from what? Our liberty and freedom being encroached upon by conflicted politicians again, or Gold nose diving?

Back to the Global Macro Grind…

If you’ve never been on a fishing expedition, I can hook you up with my peeps (Luch and RP). They’ll take you up into the bushes of Northern Ontario where you might want to bring a gun.

Word has it that this year’s Canadian black bear population could be massive. There’s lots of Gold up near Red Lake, Ontario. And with Gold -19.3% now for 2013 YTD, the Gold Bears are hungry.

What happens when a commodity bull comes across a hungry Gold bear on a camp trail in the dark? If for only behavioral observations, last week’s CFTC futures and options data might help answer that:

- Total Commodities net long contracts were up +1.1% wk-over-wk to +588,482 contracts

- Farm Goods saw the biggest net long buyers +15% wk-over-wk to +270,486 contracts

- Silver’s net long position was eviscerated (-72% on the week!) to +1,413 contracts

All the while, bears dog piled the total short position in Gold short contracts to its highest position ever (74,432 contracts).

So how is it that a bull becomes a bear in the downward dog pile position so fast anyway?

I don’t want anything to do with my nose diving into something like that.

How about stocks?

Last week’s #StrongDollar bulls brought the thunder, with both the US Dollar Index and the SP500 closing at fresh YTD highs. In the year that even a hockey player could do it, here’s the updated score:

- US Dollar +1.3% wk-over-wk to +5.6% YTD

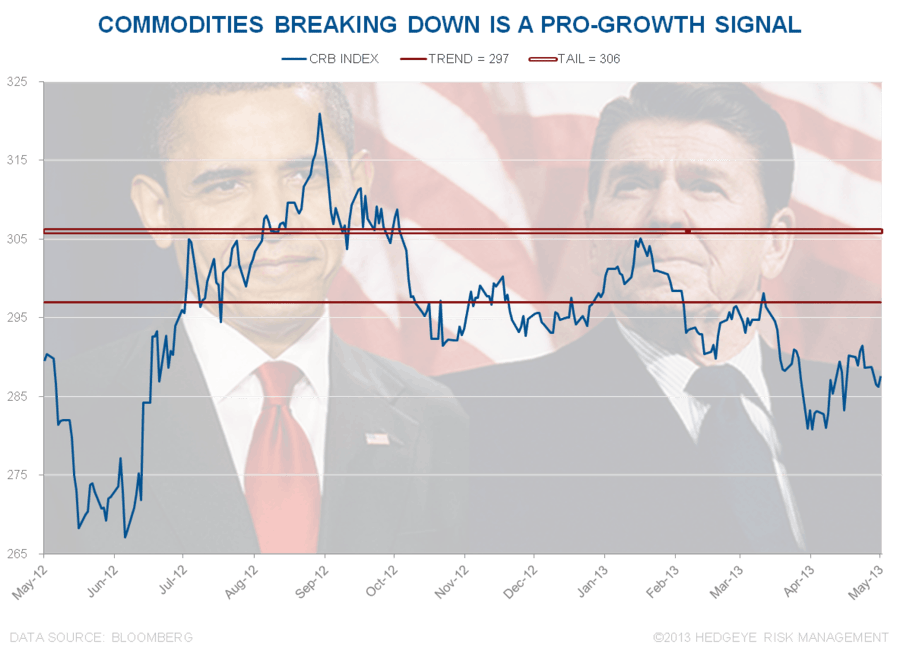

- Commodities (CRB Index) -0.4% wk-over-wk to -2.5% YTD

- SP500 and Russell2000 +2.1% and +2.2% wk-over-wk, to +16.8% and +17.3% YTD, respectively

Get the Dollar right, and you get a long of other things right.

How about bonds?

- Treasury Bond Yields lagged again this week, big time, with the 10yr UST Yield rising to 1.95%

- UST Yield Spread (proxy for economic growth) widened by another 5bps wk-over-wk to +171 basis pts wide

- Financials (XLF) love it when Yield Spread widens like that; they’re already +6.7% for May

Sell in May and go away? If US stock market bears just sold Gold and/or Treasuries in May, they’d have nailed it.

What else is ripping in May?

- #StrongDollar, Strong Consumer Discretionary Stocks (XLY) = +5.4% in May and +21.3% YTD

- High Short Interest Stocks = +12.6% in the last month and +21.0% YTD

- Low Yield (Higher Growth) Stocks = +11.4% in the last month and +21.9% YTD

It won’t take Americans or their compromised politicians long into their yield chasing expedition to realize that people are bidding up #GrowthAccelerating as bear scraps are issued to the #EOW (end of the world) trade. You should be very please to read that.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $$1351-1424, $101.32-105.29, $83.18-84.71, 101.21-104.36, 1.88-2.01%, 12.13-13.81, and 1643-1672, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer