“Economics is haunted by more fallacies than any other study known to man.”

-Henry Hazlitt

That’s the opening sentence to one of the best introductory books on markets that you’ll ever read: Economics in One Lesson. Hazlitt wrote the book in 1962, then republished it again in 1979. The quote is timeless. It’s also cyclical.

Our everything Japan Jedi, Darius Dale, and I spent the day seeing clients in Boston yesterday and we had some colorful debates about what both the New York Times and The Economist are all of a sudden championing as “Abenomics.”

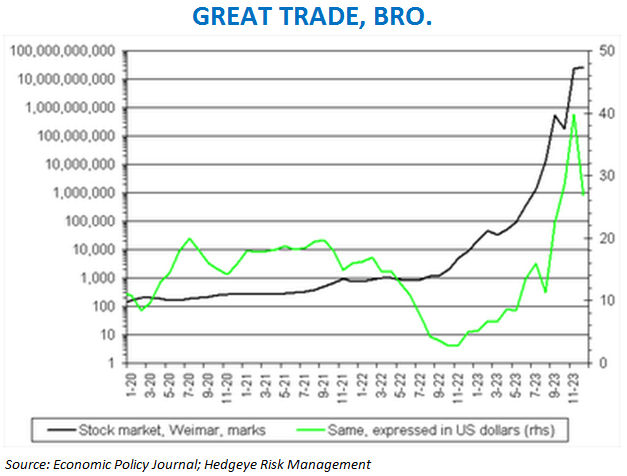

To be crystal clear on our conclusion on how we think this ends for the Japanese people: in tears. Never mind a country that starts doing it with a quadrillion in debt, there has never been a country in the history of humanity that has devalued their way to long-term economic prosperity. Championing Japan’s economics today is the equivalent of cheering on the Weimar Republic circa 1924.

Back to the Global Macro Grind…

The exciting thing about getting long the Weimar Republic’s stock market in the early 1920s is that you would have crushed it on the long side. The devastating thing was the other side of the trade – The People, their liberties, and purchasing power got crushed too.

Try some anti-gravity (economic or physical) exercises at home, and let me know how it ends. As a general rule, what goes up comes down, fast. The Yale Economics Department didn’t teach me that, btw. Incredibly, Keynesians believe they can “smooth” gravity.

The Weimar Nikkei was down another -5.2% last night. It’s down -13% from its Policy To Inflate high of May 22. That’ll leave a month-end mark. So will the implied volatility this kind of a move perpetuates throughout our interconnected global macro ecosystem.

What is a Policy To Inflate?

- A Policy To Inflate is an explicit (and implicit) strategy to debauch and devalue the currency of your people

- Bernanke is the “innovation/communication” dude who taught the Japanese to roll this out (without calling it what it is)

How do you devalue?

- As Bernanke’s boy, Paul Krugman, suggested to the Japanese in 1997, you need to “PRINT LOTS OF MONEY”

- And, ideally, have your conflicted/compromised politicians spend their brains out on borrowed moneys, at the same time

Then you have to overlay the almighty “communication tools” (i.e. central planners whispering inside info to “consultants” who then tell fund managers and/or bark about how much more you can print if/when you feel like the stock market needs more juice).

This communication tool thing has the potential to be a lot more powerful today than it was for the Germans in the 1920s, primarily because the distribution pipe for our conflicted/compromised media is exponentially larger.

Remember, any lie can live for as long as people are dumb enough to believe it. I don’t think the media is as dumb as they are cornered. If they don’t broadcast this Fed, BOJ, and ECB propaganda, they lose access to the only meaningful content they have left.

BREAKING NEWS: central planner A says B to reporter C in the WSJ and/or English Major D @CNBC – markets react!

People who are paid to believe lies inspire us. So we are going to publish the Hedgeye Risk Management Top 10 things a hard core Bernankian is going to tell you in a meeting about the benefits of 0% interest rates and burning your currency.

At the top of the list will be things like “exports”, “competitiveness”, etc. These aren’t new arguments. But what’s fascinating about them is that they are the same fear-mongering and regressive arguments that central planners have been making since the 1920s.

Losers make excuses when their plans aren’t working. For Abenomics to work, we need to see sustained real (inflation-adjusted for local currency) economic growth.

In the short-term, they might get the illusion of that – it’s called inflation. In the long-run, what do they care about what they really get? On that score they’d agree with Keynes too; in the long-run they (and the Weimar Nikkei) will be dead.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST10yr Yield, VIX, Nikkei225, and the SP500 are $1, $101.06-103.98, $83.31-84.61, 100.41-103.69, 2.01-2.18%, 12.35-15.11, 130, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer