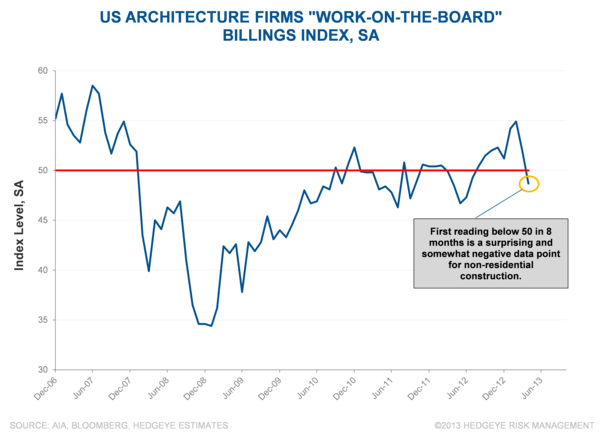

The Architectural Billings Index (ABI) fell out of bed in April, signaling contraction for the first time in eight months. The index is supposed to lead non-residential construction activity by 9-12 months. The index suggests that, while non-residential construction activity may continue to strengthen through 2013, it may soften around year-end/early 2014. The weaker ABI is a potentially negative data point for a number of non-residential construction exposed companies/industries, such as TEX, MTW, URI, Steel & E&Cs. Given the significant optimism around the non-residential construction rebound, it is a noteworthy reversal.