Investing Ideas Updates:

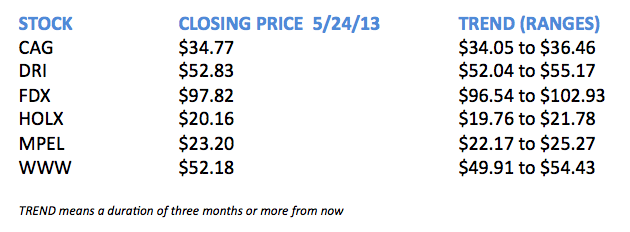

- CAG: Consumer Staples sector head Rob Campagnino has no update this week on ConAgra. (Please click here to see the latest Stock Report on CAG.)

- DRI: Restaurants sector head Howard Penney says recent events at JPMorganChase give Darden Restaurantsshareholders something to meditate on. Jamie Dimon’s retaining the twin roles of CEO and Chairman of the Board raise corporate governance questions that will affect other industries. In the Restaurants sector, DRI shares this structure – says Penney, to the shareholders’ detriment. DRI Chairman/CEO Clarence Otis “has been keeping a low profile of late,” writes Penney, and with good reason, given “the industry-lagging operational performance of Darden’s brands.”

US industry is slowly moving away from having one person in both Chairman and CEO roles – around 41% of S&P 500 companies separate the roles, up from only 21% in 2001. Penney says Dimon’s victory may be seen as a general stamp of approval for all executives who currently hold both roles. In DRI’s case, he suggests, “substandard operational performance could potentially be ameliorated by structural changes,” the first of which might well be separating the top positions, which would hold the CEO more directly accountable for operational decisions.

Penney says “DRI is in need of a CEO that is focused on the operations of the individual brands. We have heard from more than one shareholder suggesting that the current CEO is detached from the operating side of the business and does not know the numbers.” If a CEO doesn’t understand the operation of the business, and doesn’t even know revenues, costs and profits, it seems the only CEO-like job left for him to do is to travel in the corporate jet.

This could go a long way towards explaining why DRI has underperformed the average stock in its segment by 59% over the last three years. Penney likes the stock here – and he increasingly likes the possibility of activist shareholders crying “enough!” (Please click here to see the latest Stock Report on DRI.)

- FDX: Industrials sector head Jay Van Sciver has no update this week on FedEX. (Please click here to see the latest Stock Report on FDX.)

- HOLX: Healthcare sector head Tom Tobin acknowledges that Hologic has done poorly recently, but continues to like the fundamental picture. And he notes an increase in short interest to levels that could presage a bullish move for the stock. Tobin looked at the controversy surrounding Hologic’s cervical cancer screening business, citing new cancer screening guidelines that “strongly suggest women be tested every three years instead of the customary once a year that has been the norm for some time.”

Tobin and his team reviewed the state of cervical cancer screening (Pap tests) and human papillomavirus (HPV) testing across different payer classes and age groups. They found that Pap appears over-utilized – but HPV appears under-utilized. And, new guidelines notwithstanding, Obamacare looks like a tailwind to both types of testing. The bear case is simple arithmetic: Pap tests go from yearly, to once in three years, causing HOLX’s Pap business to decline by two-thirds.

Tobin points out that those same guidelines also call for HPV testing. He thinks the net is either no disturbance to overall testing, or maybe even a mild increase. Most important of all, for the time being it will be very hard to change people’s habits. Women have largely gotten programmed to have the annual check, and most patients certainly like the security of getting that clean bill of health.

Engrained behaviors are hard to change, especially if it means voluntarily going from annual security to triennial doubt. Guidelines? Maybe not. (Please click here to see the latest Stock Report on HOLX.)

- MPEL: Gaming, Lodging and Leisure sector head Todd Jordan has no updates on Melco Crown Entertainment this week. (Please click here to see the latest Stock Report on MPEL.)

- WWW: Retail sector head Brian McGough likes this “expensive” stock right here, right now. His model indicates WWW could produce 25% EPS growth over the coming 3 years, while at the same time taking down debt levels, a combination that he believes should have the stock trading at more than a double over the next 2-3 years.

The risks are the stock’s already high price and implied P/E of over 30. But McGough thinks for the downside to be realized, WWW needs to suffer a combination of bad European sales, a horribly bad winter both here and overseas, and a complete failure of the “new boat shoes” model.

It isn’t often that an analyst likes a stock for short-term Traders and for long-term Investors. McGough likes WWW for both – and even for intermediate-term Undecideds. Expensive today. Lots more expensive over the next couple of years. (Please click here to see the latest Stock Report on WWW.)

Macro Theme of the Week: Mandibular Manipulations

The story so far:

As he embarked on what was to be the first of a series of moves intended to stabilize the US financial markets, Federal Reserve Chairman Ben Bernanke – former Princeton economics professor and renowned expert on the Great Depression – admonished Congress that “lacking much experience with this option, we do not have very precise knowledge of the quantitative effect of changes in our holdings on financial conditions,” and warned that “uncertainty about the quantitative effect of securities purchases increases the difficulty of calibrating and communicating policy responses.”

This is why there is a Fed chairman. Pace our own CEO, Keith McCullough and the many others who are critical of unelected officials making policy decisions that affect the whole world, members of Congress really like their jobs, and having someone to blame is key. Our high school football coach, Coach Boyers, used to shout at us during practice, “When the going gets tough, the tough get going!” For members of Congress the motto is, “When the going gets tough, the Hill points fingers.” They would not have lasted an hour on the practice field with Coach Boyers, one of whose favorite terms of endearment was “he’s a pathetic excuse for an idiot.”

Bernanke’s job, which he has embraced with as much relish as his deadpan manner will allow, is to make sure that Rich Folks stay Rich. There’s a popular misconception that the job of the Fed is to stabilize the US economy, which would result in such knock-on effects as keeping people employed and making sure that homeowners remain in their homes. The actual job of the Fed is to stabilize the banking system.

What constitutes “banking system stability” is largely a function of where you sit. It means one thing to a family that has been defrauded by unscrupulous mortgage originators and is about to lose the house they live in, together with their life savings. It means something very different to the CEOs of the Too Big To Fail banks that received the TARP trillions in largesse.

In order to keep the banking system stable, the Fed performs an ongoing sequence of market manipulations known as Open Market Operations. The Fed heads meet regularly in Fed Open Market Committee sessions (FOMC) where they review the output of millions of data calculations all designed to get a fix on where inflation is, and to figure out where it should be. The purpose of open market operations by any central bank is generally to influence short-term interest rates, and thereby to control the Money Supply in the short term. Generally, the more money floods into an economy, the higher the rate of inflation.

Another way of looking at this: the more of a commodity becomes available, the cheaper its price gets. Now, if you look at money as the commodity, you’ll see that its “price” is the amount of stuff you can exchange for it. The more money floating around in a system, the less stuff your dollar will buy. When there’s only $100 in a theoretical economy, a piece of cheese might cost $1. When there’s $1,000 in that same economy, the piece of cheese will cost $10. Voila! your money just went down in price.

What this has to do with Ben Bernanke is that the successive rounds of Quantitative Easing (QE) he has overseen since 2010 have caused asset prices to go up. This has made it harder for normal folks to buy things like gas and groceries. But rich people have lots of their wealth tied up not in cash, but in assets. So while the flood of dollars into the economy caused people’s paychecks to be worth less – they could buy less cheese every week – it enabled the people who owned the cheese to collect lots more dollars.

The constant pumping of financial assets is consistent with the old notion of “trickle-down” economics: when rich folks get richer, they ultimately get so very rich that they have trouble holding onto all their money and some of it starts to trickle down to lower economic classes.

This week Fed Chairman Bernanke demonstrated the other side of the Fed’s monetary policy arsenal: he opened his mouth. No less than Samson, who slew 1,000 Philistines with the jawbone of an ass, the chairman of the Federal Reserve has the power to move markets by doing nothing more than opening his mouth.

In his Congressional testimony this week, Bernanke said the Fed may begin to taper off its pace of bond purchases in the next few months, if the FOMC notes indications of sustained economic growth. And Bernanke is not alone in jawbone brandishing. Last week another Fed Head, John Williams, president of the San Francisco Fed, told the press “We could reduce somewhat the pace of our securities purchases, perhaps as early as this summer.”

We defy you to parse all the qualifiers in that sentence.

As Bernanke was speaking, the markets shuddered, moaned and swooned. While many saw this as a sign that the markets have lost faith in Helicopter Ben, the tonic of free money keeps them coming back. Each successive round of QE has elicited less of a response than the one before. We’re not sure where Ben & Co can go this time, but we note yet another Little Samson who leapt unexpectedly from the thicket yesterday and brandished his jawbone.

St. Louis Fed president James Bullard said he thinks it is too soon to slow the pace of bond buying. Bullard is rather more hawkish than Bernanke (see Investing Term of the week below) so his statements caught observers off guard. We think this is as it’s intended: Bernanke and a few other Fed Heads get to take turns playing Good Cop / Bad Cop. It keeps the markets just unstable enough to lower prices temporarily. Lower prices gives the Fed the ability to buy even more bonds for their monthly $85 billion. This see-sawing in the markets is great for traders, especially for smart folks who run what are called Long-Short hedge funds. In a Long-Short fund, as you probably figured, the manager is simultaneously long and short different assets. If the manager is good, the portfolio makes money on both sides – and the offset helps to hedge when the market swings too far in one direction.

The way we see it, Bernanke is running the biggest hedge fund in history. Long the US bond market – all of it – and short the dollar. With these volatile days in the markets, he should be making money like crazy.

So where is it?

Sector Spotlight: As High as an Elephant’s What?

Everybody needs a break now and then. To hear him tell it, it seems our Consumer Staples sector head Rob Campagnino may be taking a sabbatical for the next one or two quarters.

This week Rob did a post-Q1 assessment of his sector with the upbeat title “The Case Against Consumer Staples Stocks.” His basic takeaway is that stocks in the group in general have moved up in price for what appear to be a variety of tangential reasons. The one reason missing from the mix, says Campagnino, is Valuation.

“Valuation” writes Campagnino “doesn’t matter until it matters.” He attributes the rise in the group to a list of likely factors, including expectations of improved profitability in light of declining commodity prices, speculation about “who’s the next takeover” after the Heinz deal, and investors looking for yield in a relatively safe instrument and buying big Staples names for the dividend.

This looks like a spindly set of supports to build an investment case. It’s reminiscent of the BRICS investment theme that drove billions of investment dollars into emerging markets. Investors got caught up in the euphoria of seeing their holdings go up – because the price of oil was rising, or of iron ore – and forgot that the investment theme required single-commodity economies to develop into complex markets complete with business innovation, corporate governance and credible financial markets. When commodity prices started to roll back, investors saw that many of their BRICS investments were nothing but one-legged stools.

At its most dire, something like this may be poised to wash over the Consumer Staples sector. Maybe there won’t be a rash of acquisitions to drive prices to astronomical new levels. Maybe the yield investors who planned to buy into the Staples sector have already bought. Maybe the earnings pop from the decline in commodity prices is largely priced into the sector.

Another factor Campagnino points to is inflows into low-volatility ETFs, many of which have large Consumer Staples holdings. One of the oddities of the ETF world is that, unlike a hedge fund, a mutual fund, or a corporation, ETF managers can simply roll up the mat and walk away. Some ETF creators have come in for criticism lately for liquidating ETFs that haven’t performed up to expectation. This makes it difficult to assess the overall investment performance of an ETF manager. It makes comparisons darned near impossible if they can liquidate their losers at any time, while letting their profitable funds continue to trade. If this happens in the Staples sector it will create not an overhang, but a downdraft in the market. Unlike large shareholders who work carefully to get out of a block of stock without forcing down the price, ETFs buy and sell large quantities of shares all at once, with the potential to create significant short-term market disruptions.

In short, there are lots of little things that could add up to price declines across much of the sector. And as prices start to erode, investors may look at their motivation for buying the stocks and decide that, without solid valuation to back them up, it may be time to cut their losses. Campagnino points out that the sector has not seen the lockstep rise in analyst earnings estimates and an accompanying rise in stock prices that often signals a robust group. In fact, in the quarter the average Staples company came in at slightly below revenue expectations, and only slightly above EPS estimates. In other words, no major upside surprises to encourage hope to spring eternal in investors’ hearts.

Campagnino continues to like a few companies – notably CAG remains on his list – but thinks that much of the good news is already priced into the sector, and much of the really, really good news may not materialize.

Meanwhile, perhaps the single most exciting point in the space is the confirmation of Campagnino’s outlook for continued lower corn prices. Last week saw record planting – the acreage was equivalent to the entire state of Wisconsin. (Go, Green Bay!) Economics 101: oversupply = decline in price.

Investing Term: Hawkish / Dovish

A political “Hawk” is someone who advocates military action to solve problems. A “Dove,” then, is one who seeks to avoid military confrontation.

The terms are also thrown around liberally when discussing the Federal Reserve, whose policy makers are ranked as Hawkish or Dovish on monetary policy.

Media company ThomsonReuters has a proprietary “Fed Dove-Hawk Scale” that ranks Dallas Fed chief Richard Fisher, Richmond president Jeffrey Lacker, and Charles Plosser, head of the Philadelphia Fed, as the top Hawks. The Hawks are staunchly opposed to continuing QE, reasoning that it is better to suffer a sharp, short depression than the lingering malaise brought on by long-drawn policies with no certain outcome and no end date.

Among the five most Dovish are Vice Chair Janet Yellin and New York Fed president William Dudley. One reason Dudley may be in favor of continued QE is his catbird seat in the galactic financial hub: QE means buying lots of bonds. Buying lots of bonds means making lots of transactions, which keeps New York’s financial sector trading desks busy. It also means funneling lots of money directly into those banks’ coffers, while getting unwanted stuff out of their inventories. This was presented as the Keynesian recipe to start the economy chugging away again, but money has disappeared into bank vaults rather than flowing out in the form of new business loans. Contrary to what many critics claim, the reason banks are not lending is not because they are greedy (they are greedy, but that doesn’t appear to be the main motivation), but because they are scared. Not knowing what the next policy moves will be, or how long the Fed’s monthly check for $85 billion will keep coming in, banks are building up cash reserves out of self-preservation and steeling themselves for the deluge that’s sure to hit when QE ends.

So it would appear that Hawkishness would lead to a sharp, but relatively brief, recession. To borrow from another context, the outcome of Hawkish policy would most likely be “nasty, brutish and short.” Dovishness, on the other hand, keeps the wheels of commerce turning, but seems to feed a long-drawn deterioration of confidence that is impossible to contain to the financial markets alone. The despair felt by many as a result of this uncertainty is a concrete case of a policy decision that targets the financial markets, but then spills over into the Real Economy.

Chairman Bernanke is a Dove – though not so much as his Vice Chair. Yellen is ranked 1 on that 1-5 scale, while Bernanke comes in a 2. The Doves outnumber the Hawks 11-5, while only St. Louis Fed president James Bullard ranks as a Centrist. The more than 2-1 imbalance is further skewed by the fact that the Chair and Vice-Chair call most of the shots that matter at the FOMC.

As we said above, the Fed moves the markets by two types of manipulation. The first way is by actually buying and selling securities, putting short term cash into the market or taking it out. The second part is by threatening to do something – even when the FOMC does nothing at all. Indeed, the Fed doesn’t even have to threaten. Often it is enough if the right official simply muses out loud.

Sampson would be impressed. We have come so far since the days of the jawbone of an ass.

Or have we?