Hello darkness, my old friend - it's good to talk to you again... We are re-shorting the Yen at an immediate-term TRADE Overbought high. “Team Krugman” in Japan meets its maker. #gravity

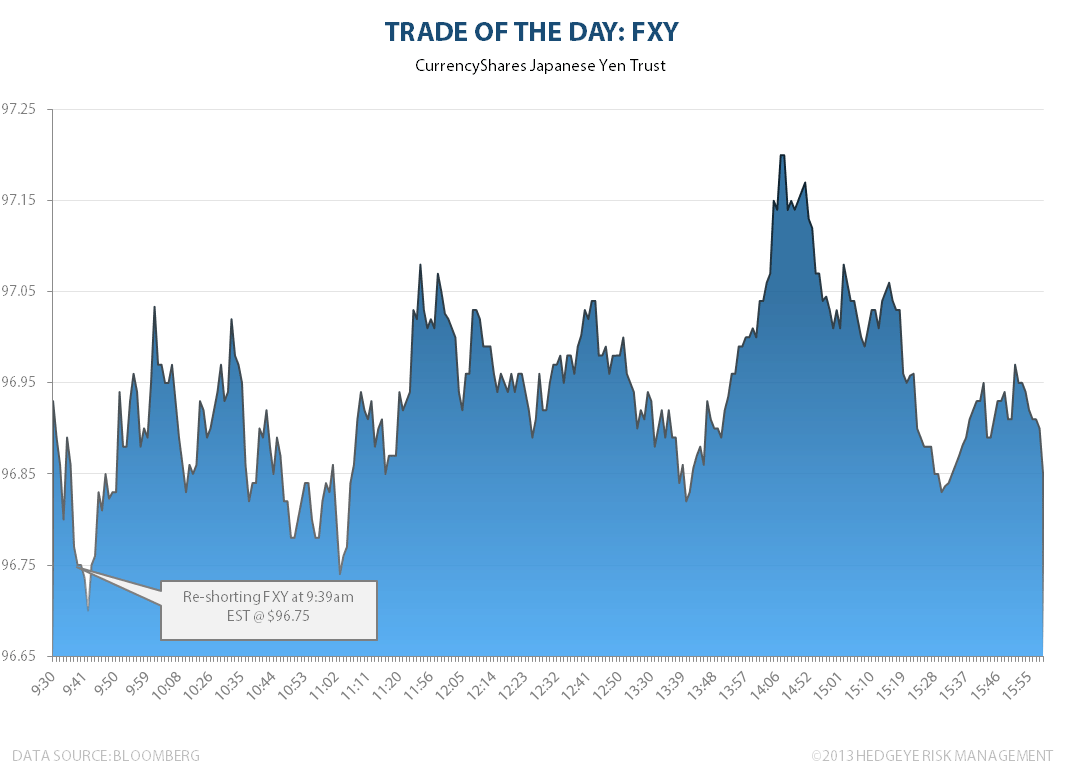

Takeaway: Keith re-shorted the Yen (FXY) at 9:39am this morning at $96.75.

Hello darkness, my old friend - it's good to talk to you again... We are re-shorting the Yen at an immediate-term TRADE Overbought high. “Team Krugman” in Japan meets its maker. #gravity

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.