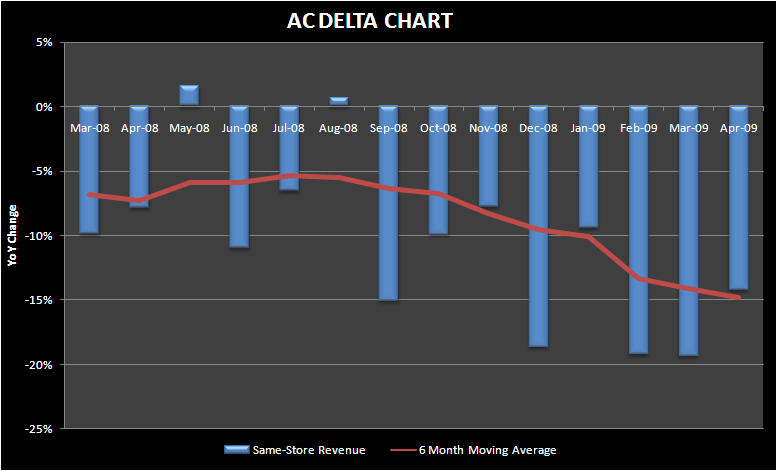

April in Atlantic City was cold. Gaming revenues declined 14% YoY, better than the 19% decline in each of the last two months. Who cares though? Business is bad and the 6 month moving average continues to trend downward. Let's move on.

I wouldn't exactly call Borgata's performance hot, but on a relative basis it was blistering. Revenues were flat YoY in April, following an 8% decline in March. The property almost posted its first revenue gain since August 2008. Both slots and tables were roughly flat, slots up a titch, tables down slightly. The six month moving average turned up in April marking the first positive discussion point coming out of AC in a long time. We'll see if that's sustainable, but what is sustainable is the advantage of having the best asset in the market.