Below is the breakdown of this morning's claims data from our head of Financials, Josh Steiner. If you would like to setup a call with Josh or trial his research, please contact

Labor Market: Back to the Races

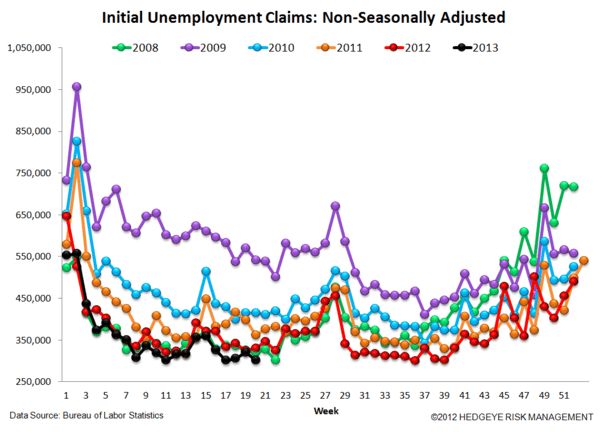

After taking a breather last week, the labor market came roaring back this week. Taking a look at the YoY trend in NSA initial claims over the last five weeks, they look like this (newest to oldest): -8.9%, -1.3%, -10.5%, -9.7%, -12.1%. That is an extraordinarily strong run. The real takeaway, however, remains that the YoY rate of improvement in rolling NSA claims continues to accelerate in 2013. This is different than what we've seen in the prior three years. The chart below shows this. The black dotted line shows that the slope in the rate of claims improvement is negative for 2013, whereas 2010, 2011 and 2012 all had positive slopes (a negative slope in this instance is better as it means the rate of improvement is accelerating).

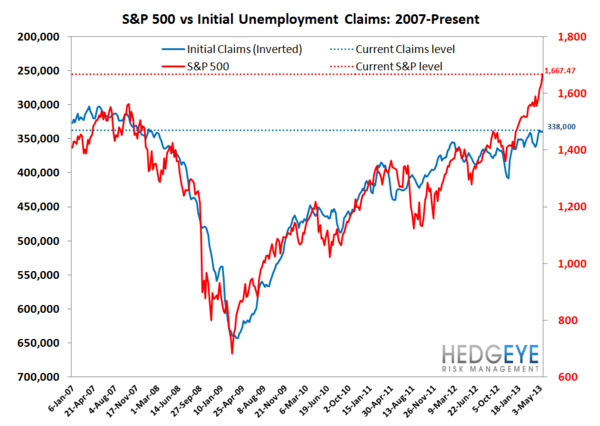

To reiterate our comments from last week, we have subscribed to a simple philosophy since Lehman Brothers. We consider three macro factors paramount in gauging the overall direction for the sector: labor, housing and the Fed. On that score, YTD all three factors had been moving in the right direction.We continue to view labor and housing as moving in the right direction from an intermediate and longer-term standpoint. The Fed, however, now seems the odd man out, and in the short-term we continue to expect weakness.

Contrary to the prior three years, however, where it was unclear whether the weakness constituted a falling knife or buying opportunity, this time around, we would view any weakness as a buying opportunity for those with a horizon beyond a few weeks. Our basis is primarily the ongoing recovery in both housing and labor. Moreover, a steepening curve is obviously a good thing for lenders, even if it retards some of the progress we've seen in housing.

The Data

Prior to revision, initial jobless claims fell 20k to 340k from 360k WoW, as the prior week's number was revised up by 3k to 363k.

The headline (unrevised) number shows claims were lower by 23k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -0.5k WoW to 339.5k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -7.6% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -8.5%.

Joshua Steiner, CFA