It’s been a tough Q1 (and then some) for many staples investors that have to make a living generating alpha on the short side, or at least have to try and have their shorts go up less than their longs. As with most market moves, there are multiple factors to which we can point as contributing causes to the run up in consumer staples:

- Investors chasing yield

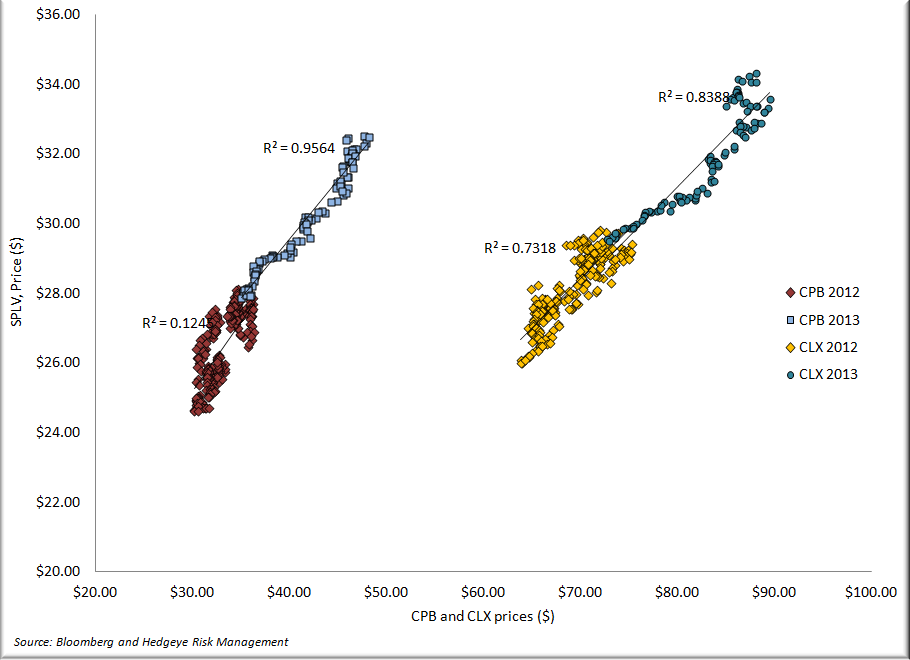

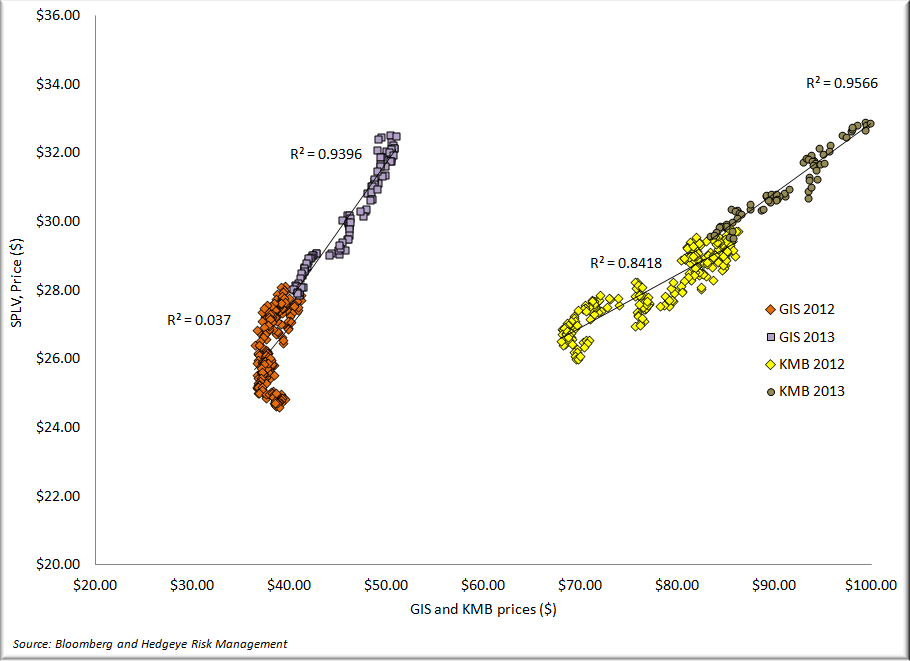

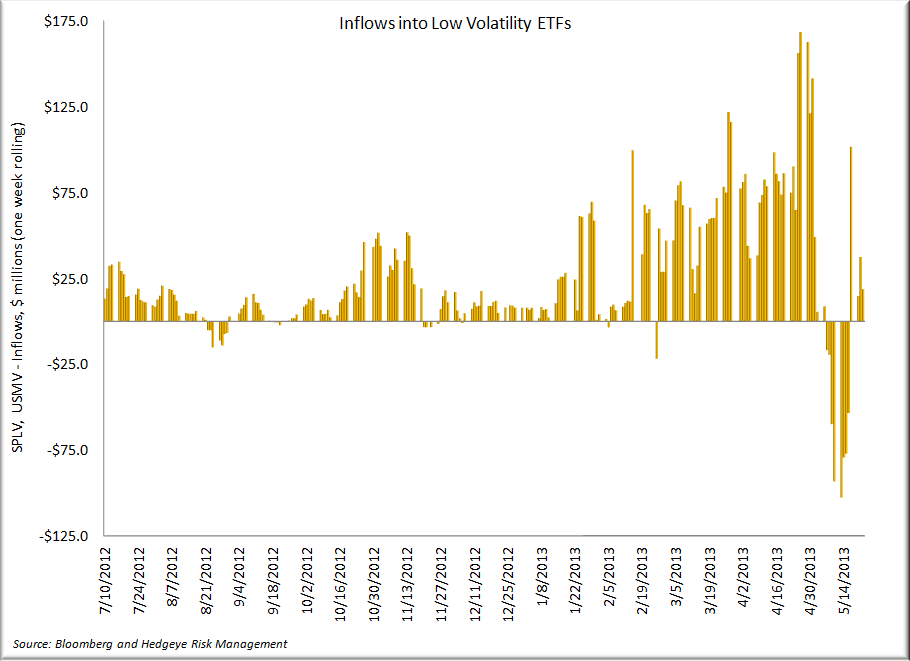

- Inflows into low volatility ETFs

- M&A speculation in the wake of the HNZ acquisition

- Declining commodity prices and the associated expectation for improvement in gross margins

- Investors skeptical of the broader market rally and playing staples as a “safe” way to be long

Conspicuous by its absence is any case for the valuation of the consumer staples sector, broadly. Valuation is always a tough one – it doesn’t matter until it matters, then when a stock heads lower (or higher, as the case may be), people point to valuation.

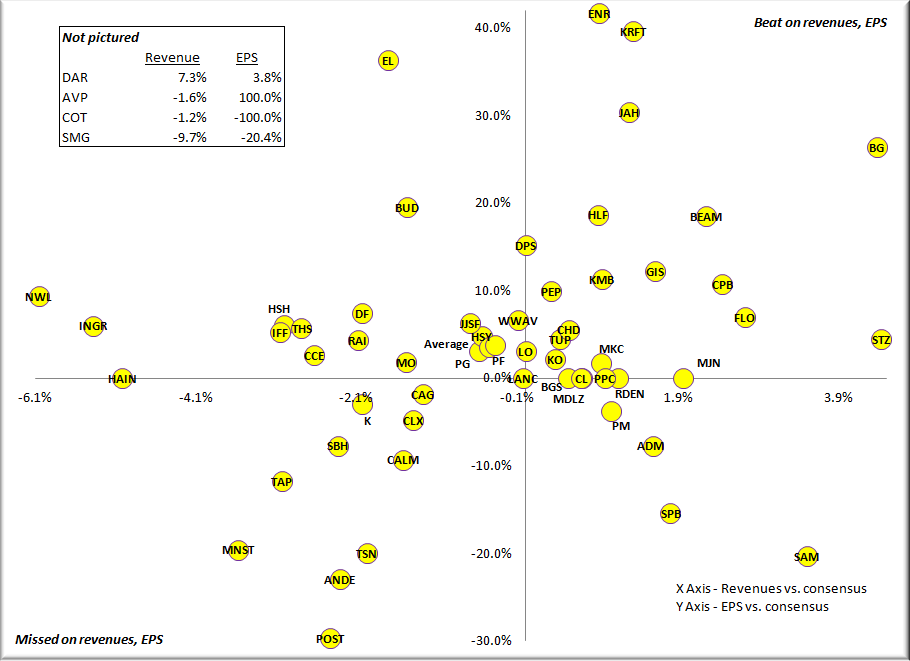

Generally speaking, we like to see stocks heading higher as estimates head higher - that has not been the case. Through Q1 earnings season, the "average" staples company missed revenue expectations by 0.4% and beat EPS by a meager 3.3%.

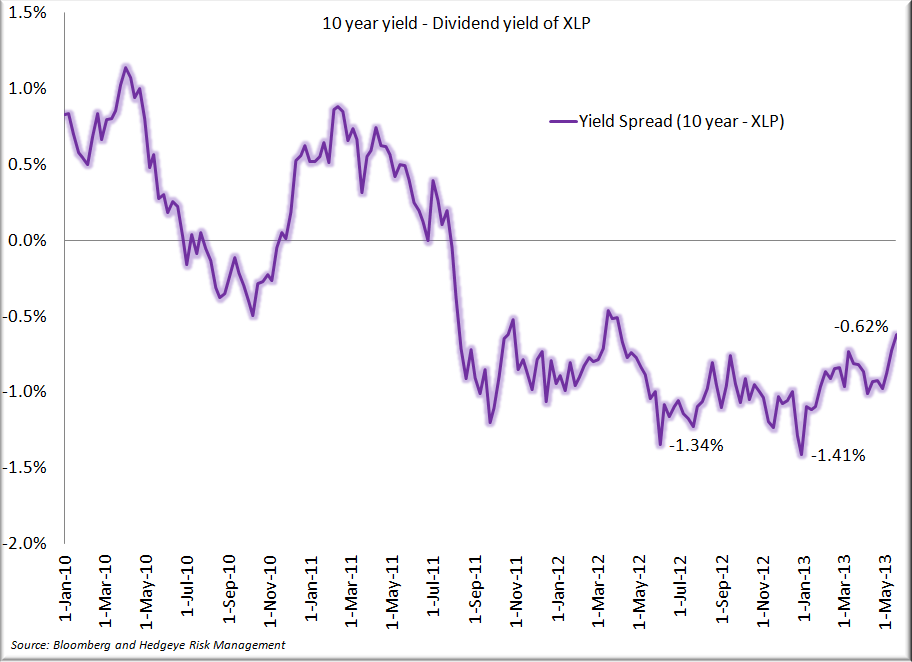

We have long made the case that investors have been using the staples sector (and utilities) as bond proxies.

With interest rates starting to creep higher, we may start to see money flow out of the consumer staples sector that was chasing yield and not invested for (or with, quite frankly) any fundamental view of the sector or the companies.

We also believe that certain stocks have benefitted from the inclusion in low volatility ETFs and associated money flows into those ETFs.

In recent weeks, inflows into these ETFs have become decidedly less one directional.

M&A speculation is more difficult to argue against. We think some names continue to make sense over longer durations as potential targets of either activists (MDLZ - known) or strategic investors (BEAM, HSH, POST, DF). We have always viewed the possibility of some sort of transaction as another reason to own a stock, but not the primary reason (unless you happen to work on a special situations desk, then have at it). Therefore, names such as CPB or even TAP, that have benefitted in part from low-quality speculation remain squarely on our least preferred list.

As to commodity prices, we believe that the companies in our universe will see a benefit, but on a lag (3-12 months, depending on the hedging programs). However, current multiples appear to be baking in a whole lot of good margin news, that may be fleeting in terms of duration given the competitive environment. Most staples companies can't stand prosperity, and are likely, in our view, to deal back margin in an effort to support top line momentum, which is still faltering.

Where does this leave us?

Quite frankly, it leaves us with a long list of names where we have a hard time seeing how the marginal investing dollar makes money at current levels. Our least preferred list is long and not so distinguished:

- KMB

- TAP

- CPB

- PM (more of an issue with the strength of the dollar)

- CLX

- CL

- GIS

- MKC

What we like remains largely unchanged:

- ADM

- CAG

- NWL

- BUD

- DF

- SPB

Call with questions,

Rob

Robert Campagnino

Managing Director

HEDGEYE RISK MANAGEMENT, LLC

Matt Hedrick

Senior Analyst