This note was originally published May 14, 2013 at 07:38 in Early Look

“Risk happens fast, and slow.”

-KM

I’m always looking for someone more intelligent than me to preface the Early Look with a quote that encompasses what I am thinking that day. It’s called validation theory. Especially in our group-thinking profession, it’s usually easier to convince people a new idea is a good one if someone else came up with it.

I also enjoy making stuff up. Today’s quote is a play on the title of one of my favorite investing books of the last 5 years, Thinking, Fast and Slow, by Daniel Kahneman. What I liked most about Kahneman’s thought process (and it’s really embedded in the title of his book) is that it’s Duration Agnostic. In a world where everyone wants certainty about timing risks, I say you embrace uncertainty instead.

One framework to apply to a duration agnostic risk signaling process is Chaos Theory. Think multi-duration, multi-factor. “The interplay between random factors (at the bifurcation point) and deterministic factors (between bifurcations) not only guides the systems from their old states into new configurations, but also specifies which new configurations are realized.” (Cosmic Evolution, pg 54)

Back to the Global Macro Grind…

So how do you know which factors are random and which ones are deterministic? Can a random factor start to become deterministic? Oh, and how the hell do we know when we are at the bifurcation point?

Welcome to my thick mind staring into at a massive correlation matrix… It can be boring as the day is long, but it sure beats trading on inside information. It’s only when something really new begins that I get really excited. Sometimes that happens fast – sometimes it’s slow.

Whether you are looking at a market system or a physical one in nature, patterns have a not so ironic way of re-appearing. “… biological systems do change in response to an unpredictable mixture of randomness…” too (Cosmic Evolution, pg 54).

We’re just trying to adapt as the market’s ecosystem is telling us to…

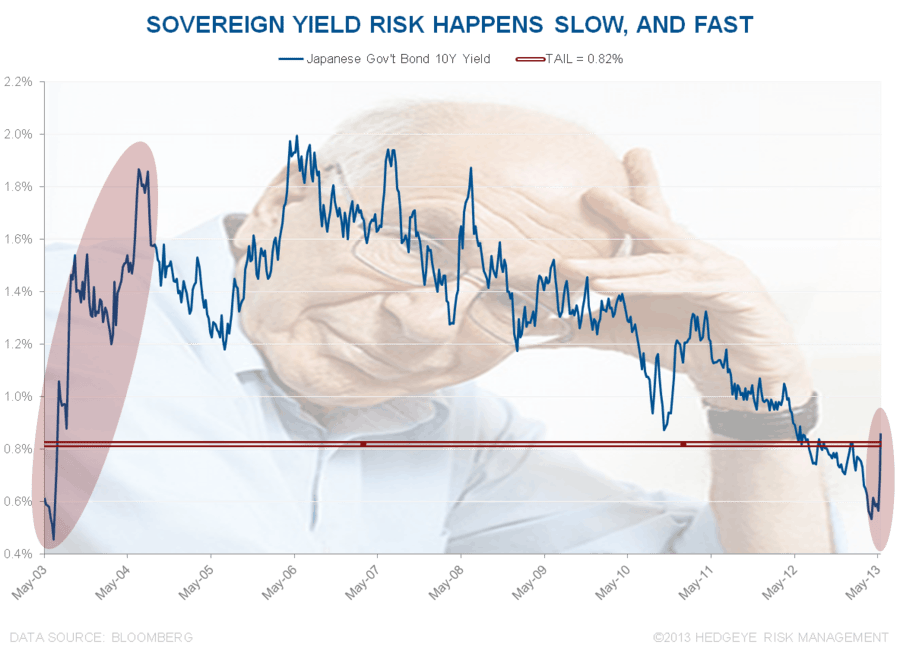

So why rant about this today instead of yesterday? Well, the answer is pretty simple – and it’s born out of everything I just wrote. Something just jumped off my page as new – JGB Yields.

JGB, yeah you know me – as in the most asymmetrically depressed live market quote in all of Global Macro – as in Japanese Government Bond Yields:

- 10yr JGB Yields +10bps day-over-day to 0.84%

- 10yr JGB Yields are now +23bps month-over-month

- 10yr JGB Yields just jumped above my long-term TAIL risk line of 0.82%

Oh yes, darkness my old friend, I have been waiting for you. But for how long will you stay? I have never shorted you before. Are you toying with my emotions this morning, or are you for real? If you are for real, what will central planners in Japan do to tone you down?

Consensus has spent most of the last 6 months looking for a crisis that never happened. If and when this one happens, it will matter. And the if part isn’t the question in my mind. It’s the when that really matters – when will Japanese and US Government Bond Yields stop baking in that they’ll never go up?

Now that the Greenspan/Bernanke Top 3 (major bubbles) have popped (Tech, Housing, and Commodities), this is really the last of the mega bubbles left – the Bubble in Super Sovereign Debt.

I don’t like shorting a bubble until that bubble starts:

- Making lower all-time highs

- Confirming those lower-highs at what I define as my bifurcation point (my TREND line)

In terms of signaling Sovereign Yield Risk, measuring and monitoring the bubble happens upside down. Which is kind of cool; especially versus the alternative (i.e. being levered long US and Japanese Sovereign Debt for May 2013 to date).

In terms of big bang risk, the 2 most important live quotes on my risk management screens next to the US Dollar Index are:

- US Treasury 10yr Yield of 1.82%

- Japanese 10yr Government Bond Yield of 0.82%

These are what I call my long-term TAIL risk lines. And they matter – big time; especially when A) they continue to confirm (becoming less random) and B) have causal research (deterministic) factors explaining their confirmations.

What’s causal in driving our call for a continued #StrongDollar and higher-lows in UST bond yields? That’s easy – employment, housing, and consumption #GrowthAcellerating as the Fed is forced to tone down bond purchases.

What’s causal in driving higher JGB Yields? That’s less easy – credit risk is as likely as a growth scare. Since one or the other can really get bond yields to move, which one will it be? The only thing we know is that there has never been a country with its debt and deficit positions (as a % of GDP) that has burned its currency and not ended up in crisis.

So we’ll see. These Japanese risks can happen fast, or slow. They may not happen at all. But, on my risk signaling scorecard, the improbable risk of rising Yield Risk in both US and Japanese Sovereign Debt just went up in the last 2 weeks, not down.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1421-1459, $100.35-103.99, $82.63-83.56, 99.61-102.53, 1.82-1.96%, 11.74-14.24, and 1618-1650, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer