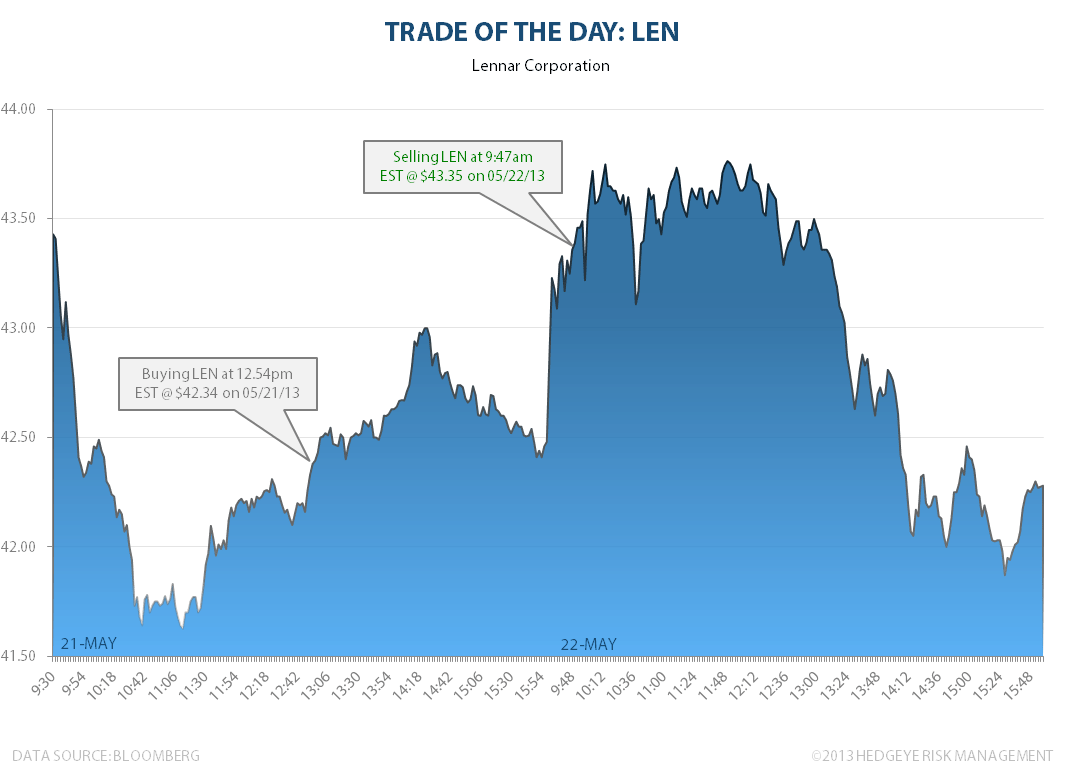

Keith sold shares in Lennar (LEN) at 9:47am today at $43.35. Miami-based Lennar is one of America’s largest new home builders.

Keith writes of his sale of LEN stock, “Backcheck. Forecheck. Paycheck. Continue to fade the bears on housing, trading the builders with a bullish bias. #HousingsHammer”

Keith now has three winning trades on the long side of LEN since March.