Suffice to say, the masses are beginning to figure out this inverse relationship. AFTER things really move, that's what revisionist historians do.

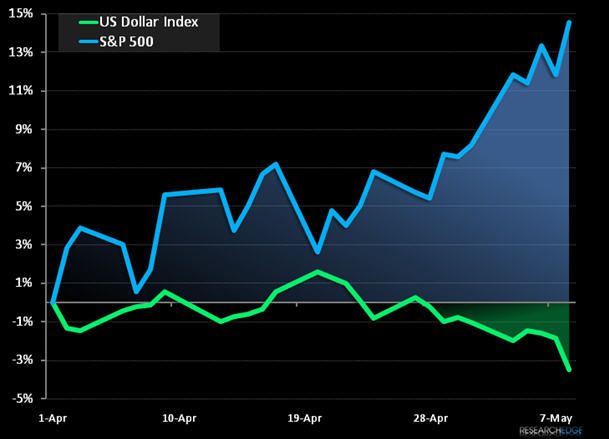

Over the course of the last 3 weeks, this REFLATION trade has really been amplified (see chart). While last week's down -2.5% week-over-week move in the Dollar probably created capitulation short covering in everything high short interest, that certainly doesn't mean that this inverse USD/SPX correlation will cease to exist.

If you're looking for lines in the USD Index that matter, here's what I'm using:

•1. USD immediate term oversold = $82.69 (bounces from that line will create short term selling pressure in stocks)

•2. USD immediate term TRADE resistance = $84.15 (all market selloffs should be bought/covered, provided that USD can't close above that line)

•3. USD intermediate TREND resistance = $85.71 (that's the big line that matters; trading below it with the SPX holding above 861 will remain bullish)

Immediate term TRADEs and intermediate term TRENDs are what I am addressing here. No matter where you go in this market, these durations will dominate daily price action in everything on your screens.

In the long run, if the USD breaks down and closes below $81.11, this REFLATION party won't be so much fun anymore. Instead of smiling when I see a consensus short seller getting squeezed, I will be getting very weary of the US Financial System's long term viability. For now, whatever credibility this conflicted American system has left needs to be respected, above all else.

Rather than buying the SP500 (SPY) this morning, I re-purchased the Technology (XLK) and Healthcare (XLV) ETFs. On a relative basis, these 2 sectors need less financial engineering than others to survive any legitimate economic stress test. No, Timmy Geithner didn't have a US Dollar crash in one of his multiple choice test boxes.

KM

Keith R. McCullough

Chief Executive Officer