This note was originally published at 8am on May 06, 2013 for Hedgeye subscribers.

“Everything in war is simple, but the simplest thing is difficult.”

-Carl von Clausewitz

In hindsight, the perma Bull/Bear War in markets gets scored that way too. After the big moves, reasons for victory and defeat become simpler to understand.

Being a market strategist isn’t simple. You need to get to simple conclusions before the market does. And the deep simplicity of it all is born out of the complex. That’s why process matters. I’ve been highlighting the thought process of American Foreign Policy strategist George F. Kennan for the past few weeks. On #process, Chapter 11 (“A Grand Strategic Education”) of Gaddis’ Kennan biography, is a beauty.

“Kennan was struck by Clausewitz’s emphasis on psychologically disarming and adversary; finding the point at which the enemy realizes that victory is either too unlikely or too costly… the assailant weakens himself as he advances.” (George F. Kennan, pg 235)

Back to the Global Macro Grind…

Relative to our current strategy on the US stock market, the enemy is the bear. Having been bearish plenty of times myself, I respect the physiological disarming process, big time. There is nothing worse than being squeezed.

With the SP500 tacking on another +2% last week to a fresh all-time daily (and weekly) closing high of 1614, the enemy is starting to give up on some core positions. You can see that by analyzing the Top 3 performing Style Factors on a 1-month duration:

- High Short Interest Stocks – 1-month price performance = +6.2%

- Consumer Discretionary Stocks (XLY) – the top performing Sector Style on a 1-month basis = +5.6%

- Technology Stocks (XLK) – 2nd best to Consumer on a 1-month duration = +5.0%

In other words, with employment, housing, and consumption #GrowthAccelerating in April (versus the 1-month head-fake of data slowing in March), what’s leading this market’s bullish charge are the simplest things associated with a growth. Gold doesn’t like growth.

Looking back at late March and early April, what was fascinating to us was how quickly consensus bulls got bearish. Since we consider ourselves Non-Consensus Bulls, this is a self-serving (and convenient) way to look at the market, in hindsight!

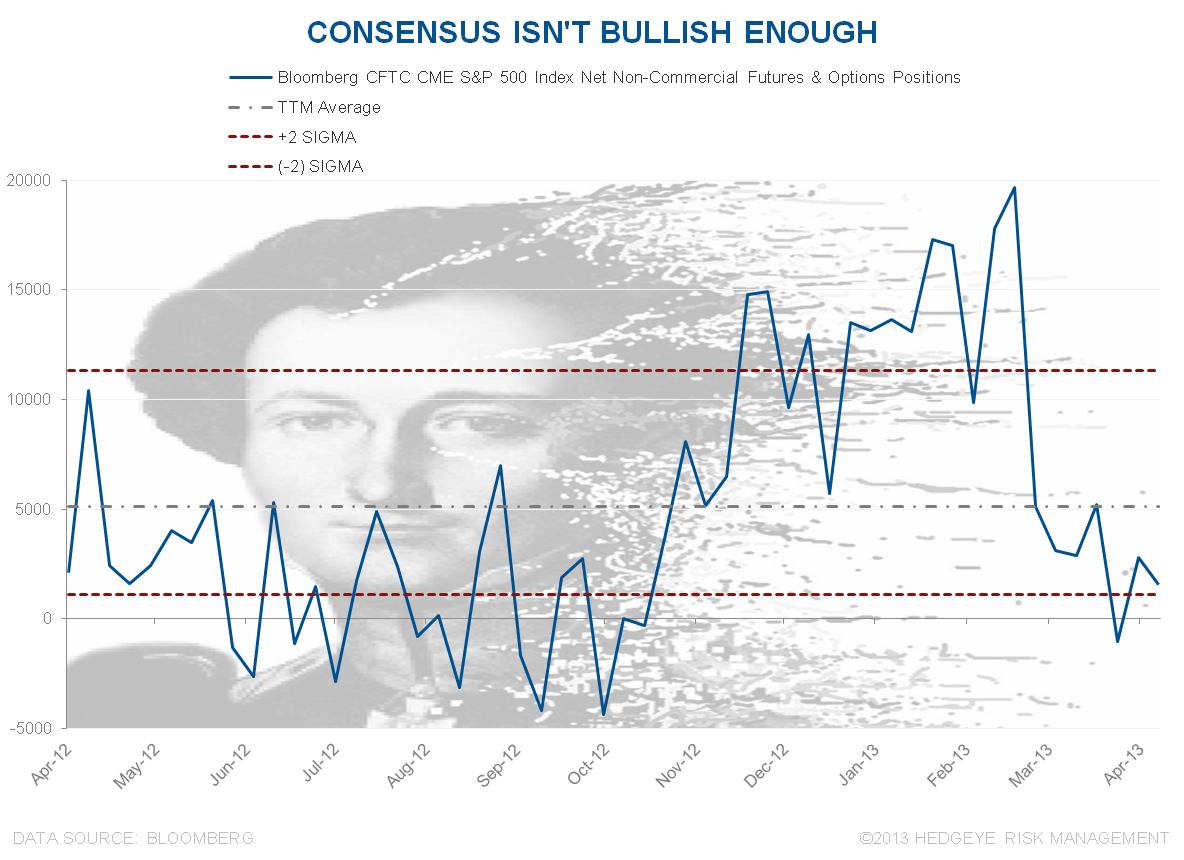

One way to look at consensus is via the net long positioning in non-commercial futures and options contracts. Going into last week’s melt-up in US Stocks, here’s how consensus was positioned:

- Uber long Treasuries at greater than +196,000 net long contracts (one of the highest positions of 2013)

- Way low in SP500 net exposure at less than +2,000 net long contracts (lowest position of 2013)

Consensus positioning wasn’t new – it was trending that way as Treasuries trended (higher) and SP500 (lower) throughout the middle of April. Many got sucked into the “March data is weak” narrative. Makes sense. Consensus sprints toward the last data point, whereas macro context wins the race.

Now what? The April economic data is undeniably better vs March – and that’s more in line with the intermediate-term TREND of the data that we have been signaling since late November, early December:

- NSA Jobless Claims hit a 5yr low last week at 324,000

- Commodities (CRB Index) and Oil (Brent) prices are -4% and -6% year-over-year, respectively

- Bloomberg’s Weekly Consumer Confidence Reading hit a 5yr high at 28.9

Confidence? Who in God’s good name in this country is actually confident? Aren’t we all supposed to be calling for the next crisis that most missed calling in early 2008? If people were as confident as I am right now, they wouldn’t be buying Treasuries as they make another lower-high versus their all-time bubble peak (November 2012).

What drives confidence? Does employment, housing, and consumption growth matter? How about the price of your home and stock market portfolio going up double digit year-over-year for the 1st time since 2006? If you want to broaden market trends beyond 3-6 months to year-over-year (y/y):

- SP500 = +16.1% y/y

- US Home Prices (Core Logic) = +10.3% y/y

- Gold = -10.9% y/y

How are end of the world ads for Cyprus, BitCoin, etc. doing this morning? That’s a confidence factor too. Some market it as “social mood.” Others sell fear in more ways than one. As George Kennan wrote in the late 1940s (when people in America were right petrified of anything they couldn’t see):

“We are in a peculiar position of having to defend ourselves against mortal attack, but yet not wishing to inflict mortal defeat on our attacker… We must be like the porcupine who only gradually convinces the carnivorous beast of prey that he is not a fit object of attack.” (George F. Kennan, pg 235)

So be the porcupine. Eventually these beastly bears will stop trying to scare the hell out of you; the perma bid for Treasuries will recede; and fear (VIX) might be priced at 10, 11, or 12 by then too. Then, the simplest of things will be to sell high, smile, and go away.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX and the SP500 are now $1406-1489, $98.81-105.24, $81.74-83.12, 97.59-100.13, 1.71-1.82%, 12.36-14.39, and 1590-1624, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer