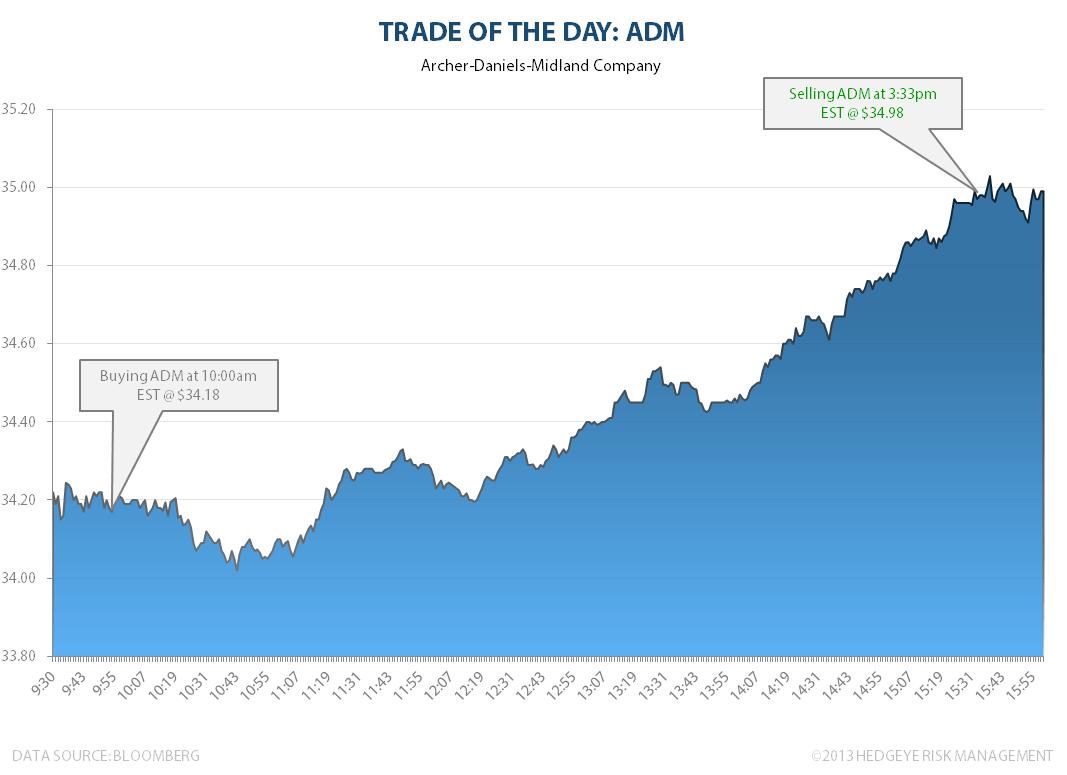

Keith bought shares of Archer Daniels Midland (ADM) at 10:00am ET at $34.18 a share, and sold them at 3:33pm at $34.98 for a tidy 2.34% profit in a little more than five-and-a-half hours.

Keith writes of his purchase this morning: “(Consumer Staples sector head) Rob Campagnino reiterating his bullish view on ADM post the Berkshire sale. Higher-lows and bullish trend (are) intact into a big corn crop utilization.”

Warren Buffett’s Berkshire Hathaway disclosed in a filing this week that it had sold its entire stake in ADM, in which Berkshire had amassed holdings of nearly six million shares.

Keith writes of his sale of ADM this afternoon, “How’s that for some weekend moneys? ADM moved to immediate-term TRADE overbought within its bullish TREND, in a day!”