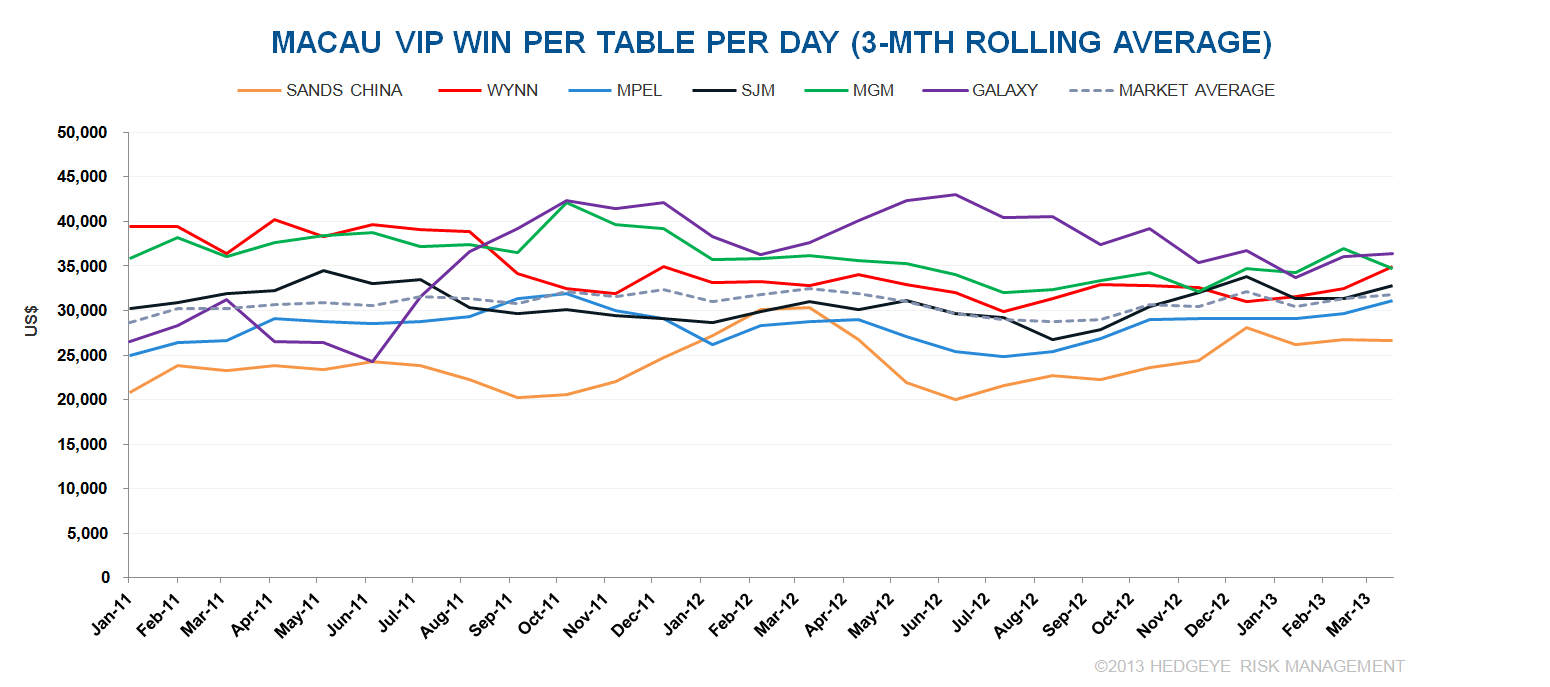

VIP per table stagnant over last few years but signs of an upturn emerging

- Unlike the Mass chart we posted yesterday, VIP table productivity has been nonexistent

- However, April showed promising YoY growth. May started strong, and we’re projecting accelerating growth for most of the rest of the year

- Not surprisingly, the two primary Cotai operators – MPEL and LVS – trail the others on the VIP side but perform well on the Mass side