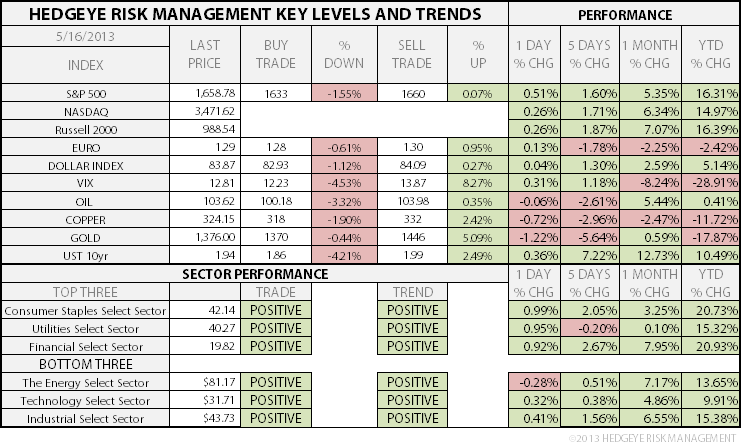

TODAY’S S&P 500 SET-UP – May 16, 2013

As we look at today's setup for the S&P 500, the range is 27 points or 1.55% downside to 1633 and 0.07% upside to 1660.

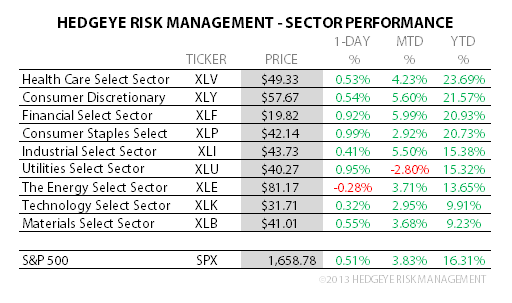

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.70 from 1.70

- VIX closed at 12.81 1 day percent change of 0.31%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: Fed’s Rosengren speaks in Milan

- 8:30am: CPI M/m, April, est. -0.3% (prior -0.2%)

- 8:30am: CPI Ex Food & Energy M/m, April, est. 0.2%

- 8:30am: Init Jobless Claims, May 11, est. 330k (prior 323k)

- 8:30am: Continuing Claims, May 4, est. 3m (prior 3.005m)

- 8:30am: Housing Starts, April, est. 970k (prior 1.036m)

- 8:30am: Housing Starts M/m, April, est. -6.4% (prior 7.0%)

- 8:30am: Building Permits, April, est. 941k

- 8:30am: Building Permits M/m, April, est. 3.8%

- 8:30am: Annual revisions to earlier data

- 9am: Fed’s Fisher speaks at NABE conference in Houston

- 9:45am: Bloomberg Economic Expectations, May (prior -4)

- 9:45am: Bloomberg Consumer Comfort, May 12 (prior -29.5)

- 10am: Philadelphia Fed, May, est. 2 (prior 1.3)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: Fed to purchase $1.25b-$1.75b notes in 2036-2043 sector

- 12:30pm: Fed’s Raskin speaks on economy in Washington

- 3:05pm: Fed’s Williams speaks in Portland, Ore.

- 6pm: Riksbank’s Stefan Ingves speaks in Chicago

GOVERNMENT:

- President Obama meets with Prime Minister Recep Tayyip Erdogan of Turkey to discuss Syria, trade, countering terrorism

- 9:30am: Senate Armed Svcs Cmte holds hearing on 2001 Authorization for Use of Military Force

- 9:30am: House Transportation and Infrastructure Cmte marks up H.R. 3, which would give Congress power to issue approval for Keystone XL pipeline

- 10am: House Oversight and Government Reform Cmte, Data Transparency Coalition hold a “DATA Demonstration Day,” to show how digital technologies would improve efficiency, management, accountability of government

- 10am: House Financial Svcs Cmte hears from SEC’s Mary Jo White on commission’s budget request

- 10:30am: House Oversight and Government Reform panel holds hearing on oil, gas production on federal lands

- 10:30am: Senate Small Business Cmte holds hearing on effect of E-Verify systems

- 11am: House Judiciary panel holds hearing on electronic employment eligibility verification systems

- 1pm: House Judiciary panel holds hearing on Agricultural Guest Worker Act

- Obama seeks to revive reporter-shield bill post-AP subpoenas

WHAT TO WATCH

- Cisco 4Q adj. EPS view in line, rev. view midpoint misses

- Time Warner Cable said to weigh stake in Hulu web-video service

- Roche’s GA101 gets FDA breakthrough-therapy designation

- Apple said to be subject of U.S. Senate offshore tax hearing

- Obama forces out acting IRS chief in bid to restore trust

- Novartis considers bid for Actavis: WSJ

- Plosser says Fed should exit mortgage-backed securities market

- Hartford Financial hires Deutsche Bank to seek buyer for Japanese unit

- Japan 1Q GDP rose most in yr on consumer spending, exports

- Tesla to raise as much as $830m to repay U.S. green-car program

- Bristol-Myers drug cocktail quells melanoma tumors: Study

- Cancer treatment’s brutal side effects may be cut: Studies

- Platts retains energy trader confidence amid price-fix probe

- U.S. wants $5b from Swiss banks to end tax row: Handelszeitung

- William Lyon Homes raises $217.5m pricing shares above range

- MSCI announces changes from semiannual global index review

- Investors see U.S. markets with best return in global poll

EARNINGS:

- Prestige Brands (PBH) 5:30am, $0.35

- Flowers Foods (FLO) 6:30am, $0.43

- Kohl’s (KSS) 7am, $0.57 - Preview

- Wal-Mart Stores (WMT) 7am, $1.15 - Preview

- CAE (CAE CN) 8:18am, C$0.18

- Applied Materials (AMAT) 4pm, $0.13

- Dell (DELL) 4:01pm, $0.35

- Autodesk (ADSK) 4:01pm, $0.45

- Aruba Networks (ARUN) 4:03pm, $0.12

- Brocade Communications (BRCD) 4:04pm, $0.15

- Brady (BRC) 4:04pm, $0.60

- Nordstrom (JWN) 4:05pm, $0.76 - Preview

- ViaSat (VSAT) 4:05pm, $0.01

- J.C. Penney (JCP) 4:30pm, $(1.05) - Preview

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Near One-Month Low as Soros, Blackrock Reduce ETP Holdings

- Soros Joins Gold-Stake Cuts Before Bear Market Drop: Commodities

- Strict Checks on China Scrap Copper Imports Boost Ore Demand

- Copper Falls for Third Day on Mounting Signs of China Slowdown

- Gold Demand Slid 13% to Three-Year Low on Investor ETP Sales

- China’s Copper Output in April Rises 14 Percent to 558,000 Tons

- Gold Demand in China Surges 20% to Record in First Quarter

- WTI Crude Declines as Fuel Demand Drops Amid Economic Weakness

- Sugar Falls to 2010-Low on Brazil, Thailand Output; Cocoa Drops

- Soybeans Advance on Indications of Sustained Demand From China

- China’s June Soybean Imports May Reach Record, Govt Center Says

- Gold Price Slump Increased India Appetite for Bullion, WGC Says

- Paulson Sold Gold Miners, Bought Family Dollar Last Quarter

- Platts Retains Energy Trader Confidence Amid Price-Fix Probe

- Freeport Stops Papua Mining After Tunnel Collapse Kills Five

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

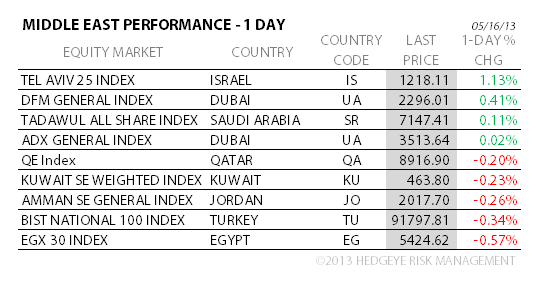

MIDDLE EAST

The Hedgeye Macro Team