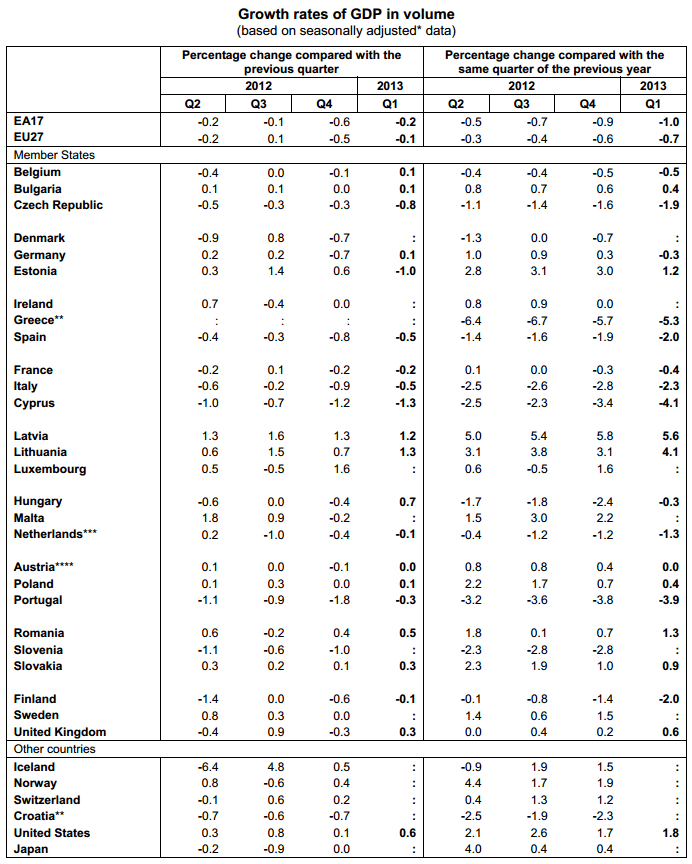

European Q1 2013 Final GDP figures were released today and confirm our call for protracted sluggishness across the region. Eurozone GDP has now contracted for sixth straight quarters and actual results for the region and major countries were lower than estimates on a Q/Q basis: Eurozone -0.2% (est -0.1%), Germany +0.1% (est +0.3%), France -0.2% (est -0.1%), Italy -0.5% (est -0.4%).

Call: we expect the EUR/USD to be range bound over the intermediate term, anchored on the ECB’s backstop for the region (with long-term TAIL support at $1.22) and a TREND/TAIL line of resistance at $1.32. We think that as the market increasingly looks for another interest rate cut (which we’re not calling for over the next months as Draghi assesses the last cut), the EUR/USD may weaken as equities rise. (This is also in line with our #StrongDollar call).

Negative France/ Positive Germany and the Periphery

We continue to wrestle with the miss-match on weak fundamental results and strong capital market performance across much of the region.

On the fundamental side, we highlight France as one nation that has not proven it has a credible plan of structural reforms to improve its competitiveness. We continue to think that Hollande’s budget policy of increased taxes without sufficient spending cuts and its outsized debt to GDP (now over 90%) will hamper the economy (and the region) more than it helps. That said, the European Commission is squarely on board to allow France two more years to reach its deficit reduction target level and has largely signaled a dovishness vis-à-vis further austerity. This could prove to be a tailwind.

On the flip side, we like Germany on a relative basis. We see GDP gains coming in 2H and the EUR/USD price benefiting the export-heavy country. Chancellor Merkel should continue to talk-up her handling of the economy throughout the “crisis” in Europe as she prepares for re-elections in September. We see Germany playing ball in the European project (writing bailout checks if needed) versus the very adverse option of a return to a strong D-Mark.

Despite ongoing fundamental weakness across the periphery, we continue to believe that market participants will buy the periphery (equities and bonds) as the yield chase extends itself alongside the expectation that the ECB will backstop the Union at all costs.

Sovereign bond issuance YTD continues to show paper being priced at lower levels, a positive sign, and in the coming months we may see steps towards setting up loan pools to small-and-medium-sized enterprises (SMEs), which would be another tailwind to a channel that is currently clogged.

For more on our outlook on the Eurozone please see last Friday’s note titled “Where’s Europe At”.

Matthew Hedrick

Senior Analyst