This note was originally published May 10, 2013 at 13:09 in Energy

EV Energy Partners (EVEP) remains a high conviction short idea for us. Today’s result changes little, except for that it seems as if we gave the Company too much value for its Utica package, and EVEP’s funding situation is now even more precarious given that it will JV the oil window acreage instead of sell it outright. We would be adding to short positions today on the back of the poor 1Q13 result and outlook.

On the Quarter

Open EBITDA (before hedges) was $31.4MM, down from $36.7MM in 4Q12 due to a 1% decline in production and higher operating costs. Excluding a 1Q-only G&A expense of $3.2MM, open EBITDA was $34.6MM (this is not a one-time item, but a recurring 1Q-only item).

On EVEP’s management metrics – which are pretty meaningless to us even though everyone else uses them – “adjusted EBITDA” was $48.5MM vs. $56.7MM expected and $69.6MM in 4Q12. “Distributable cash flow (DCF)” was $21.8MM ($0.51/unit) vs. $37.9MM ($0.89/unit) in 4Q12, for a distribution coverage ratio of 0.67.

The main reason for the miss was the hedge book rolling off, especially on the NGL side. Realized cash gains from commodity derivatives were $12.3MM vs. $28.4MM in 4Q12.

Discounted cash flow (DCF) would have been lower had it not been for the generous (and inexplicable) approximately $5MM haircut to “maintenance CapEx” in the quarter. Production fell 1% q/q and EVEP invested $21.1MM into its E&P operations in the quarter, though deducted only $13.6MM ($0.91/Mcfe) of maintenance CapEx from DCF vs. a consistent run-rate of $18 - $19MM ($1.25/Mcfe) over the prior four quarters.

EVEP defines maintenance CapEx as “expenditures necessary to maintain the production of our oil and gas properties over the long term.” But, EVEP could not manage to keep production flat on $21.1MM of total E&P spending. In our view, EVEP slashed maintenance CapEx this quarter to make the already poor coverage ratio look a little better, and that a realistic maintenance CapEx number is approximately $20MM per quarter. If maintenance capex were $20MM in 1Q13, the coverage ratio would have been 0.47.

On the Utica Shale Sale Process

EVEP is no longer looking to sell its acreage in the oil window of the play, which it once boasted would fetch more than $15,000/acre. It will now attempt to find a joint venture partner for the majority (~82%) of its marketed acreage, which is in the oil window. If any deal gets done, it will likely be for a drilling carry (and maybe a small cash bonus); we won’t be holding our breath – CEO John Walker said on the call,

“There are not enough wells drilled there yet and through one or more joint ventures we intend to find the completion technique that will solve this problem. It could take one to two years for us to find these solutions and maximize the value of our position in the supply.”

That leaves EVEP with 18,200 net acres (18% of marketed acreage) to sell in the wet gas window (majority in NW Carroll county). Timing and price remains uncertain.

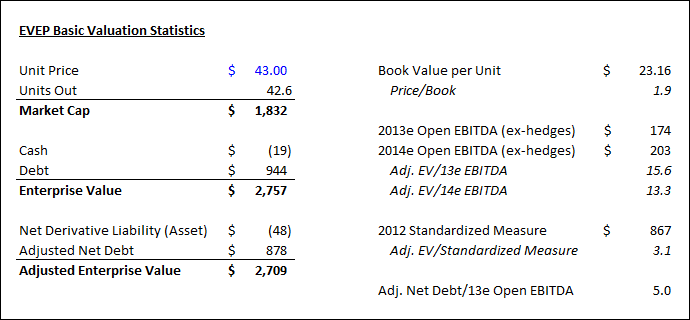

On Valuation

EVEP is still trading above a price that would reflect anything close to the intrinsic value of the assets. We’ve updated our NAV analysis taking into account the change in plans for the Utica acreage, the decrease in FV of the hedge book, and the increase in net debt. Our NAV is $22/unit.

On conventional E&P valuation metrics, the story is the same: EVEP trades at 40x 2013e earnings, 16x Adjusted EV/2013e Open EBITDA, 1.9x book value (despite having acquired the majority of its assets), and 3.1x standardized measure. The Company is over-levered with net debt of $925MM exceeding the value of its proven reserves (YE12 PV-10 $867MM), and adjusted net debt/2013 open EBITDA at 5.0x. Leverage ratios will tick higher this year without meaningful asset sales or equity-funded acquisitions as the Company invests heavily in its nascent midstream businesses.