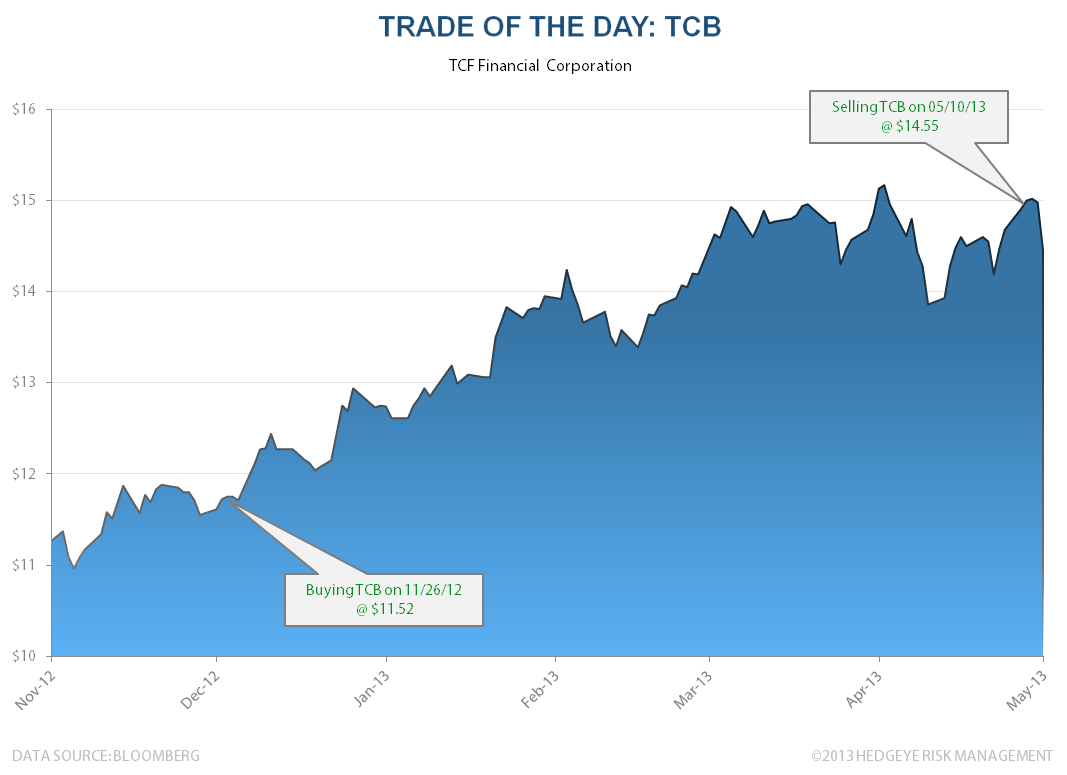

Keith sold TCF Financial (TCB) at 12:53pm today at $14.55 a share, booking a whopping 26.3% gain after holding the stock for six months.

Keith writes, “After a great run in the stock, I'll say goodbye to TCB today - primarily because their CEO (partly) did. (CEO William) Cooper selling 12.5% of his stake up here implies he probably isn't selling the company anytime soon. That takeout premium is why we held it. Fundamentals are good here, but the stock's valuation and six month return reflects most of that.”