This note was originally published May 10, 2013 at 07:47 in Restaurants

Initial indications are that April may have been another sluggish month for casual dining. For some people this might come as disappointing news. What happened to the Easter “shift” from March to April? Knowing some chains weakness at the end of March, this had shifted to strength in early April. This suggests that balance of April was weak.

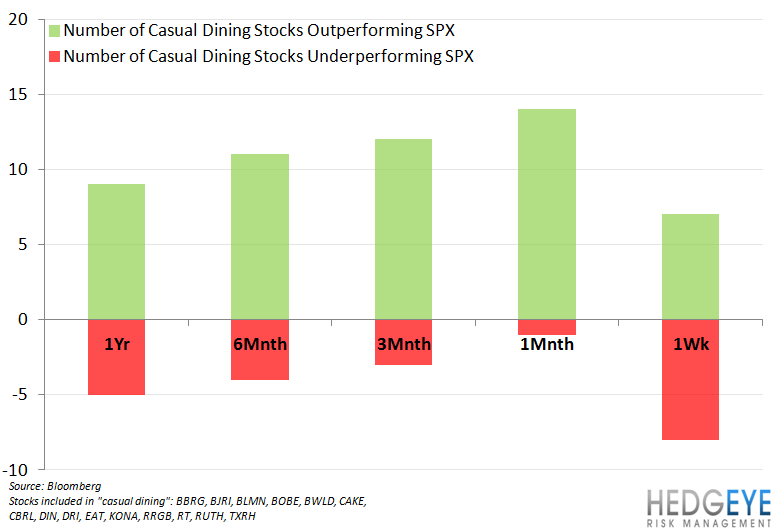

Sluggish sales trends are not being borne out in the casual dining stock, which have outperformed the S&P 500 by 340bps over the past month and 1080 basis points year-to-date. Over the same time period, the average earnings estimate has increased 1.1% and 3.3%, respectively, implying a significant multiple expansion for the group.

Black Box Intelligence released its casual dining numbers for April this week. Same-restaurant sales gained 0.4% in April, versus 0.5% in March, which implied a sequential acceleration in two-year average trends of 70 bps. Sale-restaurant traffic declined -1.7% in April, versus -2% in March, which implied a sequential acceleration in two-year average trends of 80 bps. The “Willingness to Spend” Index, reported by Black Box, also registered a sequential acceleration in April.

Our favorite names in the group remain CAKE, EAT, and DRI.