This note was originally published at 8am on April 26, 2013 for Hedgeye subscribers.

“Losing on the other hand, really does say something about who you are. Among other things it measures: do you blame others, or do you own the loss? Do you analyze your failure, or just complain about bad luck?”

-Lance Armstrong

Yesterday, I started off the Early Look with the title #Winning and today I chose its antonym as the title. It is rarely enjoyable to lose, or think about losing, especially in investing and business, but the reality is that we probably learn more from our mistakes than we do from our victories.

Lance Armstrong is now considered by many to be one of the biggest losers of our generation after being one of the biggest winners with his unprecedented string of Tour de France victories. In the most recent news, the Justice Department has filed a suit for $100MM against Armstrong and Tailwind Sports under the False Claims Act on behalf of the U.S. Postal Service (yes, it does beg the questions as to why the USPS was sponsoring cycling!). Time will tell what, if anything, Armstrong has learned from his failures and mistakes.

To be fair, it is natural to over react to mistakes (although I don’t think Armstrong is guilty of this) and I’ve certainly noticed this with myself and my colleagues at times. The immediate reaction to a loss is often a willingness to quit a strategy. In reality, the reaction to a loss should be to analyze it, learn from it, and focus on improving the results.

The more interesting point on not learning and moving on from mistakes is that we basically inhibit ourselves from creating new ideas and opportunities. As Po Bronson and Ashley Merriman write in “Top Dog: The Science of Winning and Losing”:

“By definition, new ideas can’t come from a playing-not-to-lose mindset, where the inhibition system is hyperactive. Creativity requires disinhibition: it requires turning off the internal censors in order to allow brainstorming and idea generation. Neuroscience has shown that in the very moment when a new idea sparks to life in the brain, the prevention system is turned off.”

So, in effect, if you can’t actually forget about your past mistakes and become uninhibited, you will chemically impair your ability to generate new and innovative ideas.

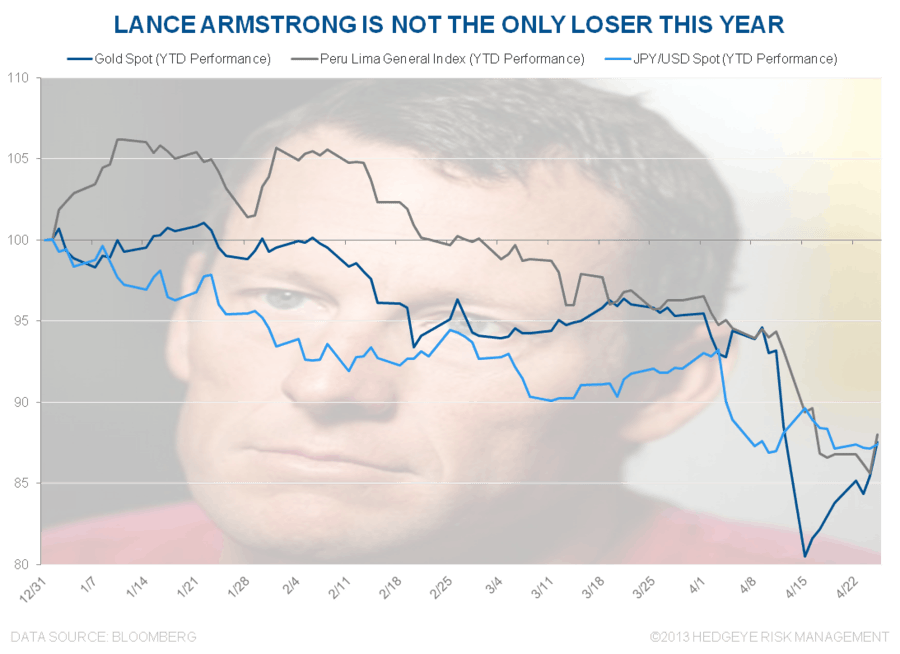

Forgetting about mistakes is certainly not easy, especially when the reminders are very present. In the Chart of the Day, we’ve highlighted the three worst performing major global asset classes in the year-to-date: Peruvian equities, the Japanese Yen, and gold. The irony of the last two is that when central bankers are aggressively printing money, like the Japanese central bank is, gold is not supposed to go down. Of course, if unilateral money printing leads to U.S. dollar strength, the case for gold obviously becomes less compelling. It should be no surprise that in U.S dollar terms the Yen is down almost the same percentage as gold this year.

The larger risk to gold is that we actually get to a place in which the U.S. Federal Reserve begins to tighten policy. Certainly some slackness remains in the U.S. economy and inflation appears largely in check, but as my colleague and our U.S. economist Christian Drake pointed out yesterday in a note, we are starting to see potential that economic growth in the U.S. may accelerate based on:

1) Housing – The housing recovery continues on the parabolic recovery that we outlined at the start of the year. Specifically, mortgage purchase applications recently registered a YTD high, median home prices of existing homes for existing home sales rose 11.8% (the highest level since November 2005), and inventory of existing home remains basically at its trough (down 17% in the last 12 months); and

2) Employment -This week’s Initial Jobless Claims data was again positive with both the SA and NSA series showing sharp sequential improvement. We consider the 4-week rolling average in NSA claims to be the more accurate representation of the underlying labor market trend and on that metric, the trend improved 250bps week-over-week as the year-over-year change in 4-wk rolling claims went to -6.3% Y/Y from -3.8% Y/Y the week prior. So, despite initial sequester related impacts beginning in April and the seasonal distortion in the seasonally adjusted data shifting to a headwind, labor market trends continue to show steady improvement.

Despite what some of the talking heads might have you believe, in an economy that is 70% consumption, a strong U.S. dollar (the currency with which we consume), an improving housing market (the consumer’s balance sheet), and stabilizing employment, are all very supportive factors of improving economic growth.

I’m going to end this morning in the winner category. If you haven’t been watching European sovereign yields, you should be focused on them as a measure of global tail risk. Since the freak-out highs in yields perpetuated by the Cyprus dysfunction, yields in the 10-year sovereign bonds of Italy, Spain, and Portugal have recovered to some of the lowest levels we’ve seen since the beginning of the European sovereign debt crisis began. In fact, it won’t be long before Italian 10-year yields starts with a three handle . . . I mean, who would’ve thunk!

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1321-1478, $97.31-103.34, $82.55-83.44, 97.45-101.36, 1.70-1.76%, 11.33-14.89, and 1564-1595, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research