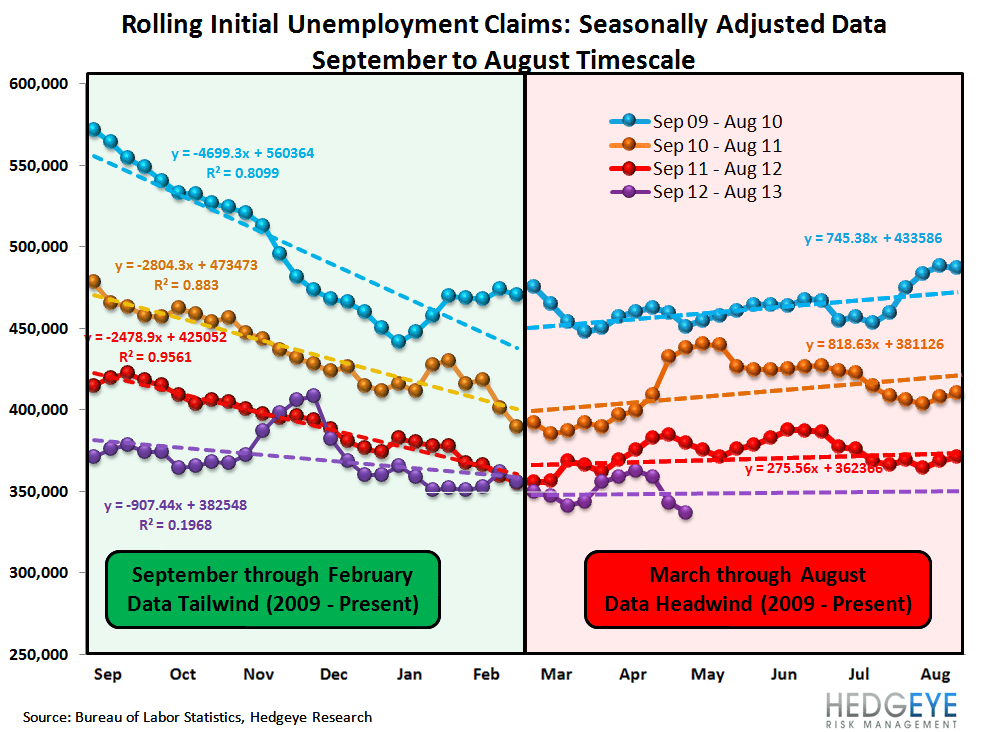

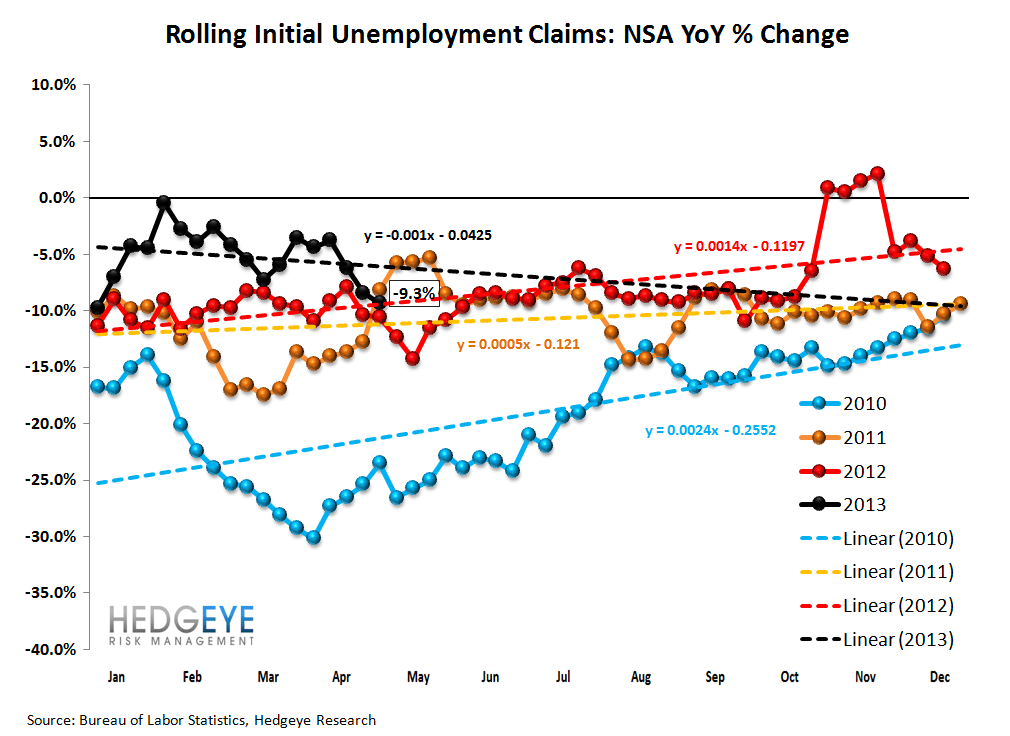

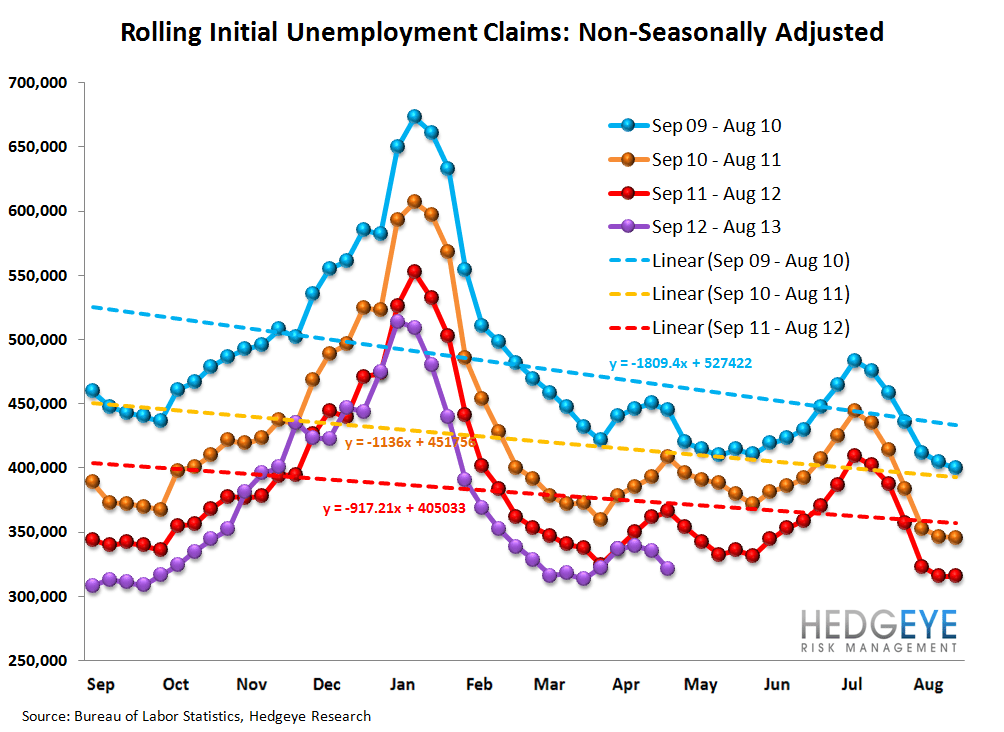

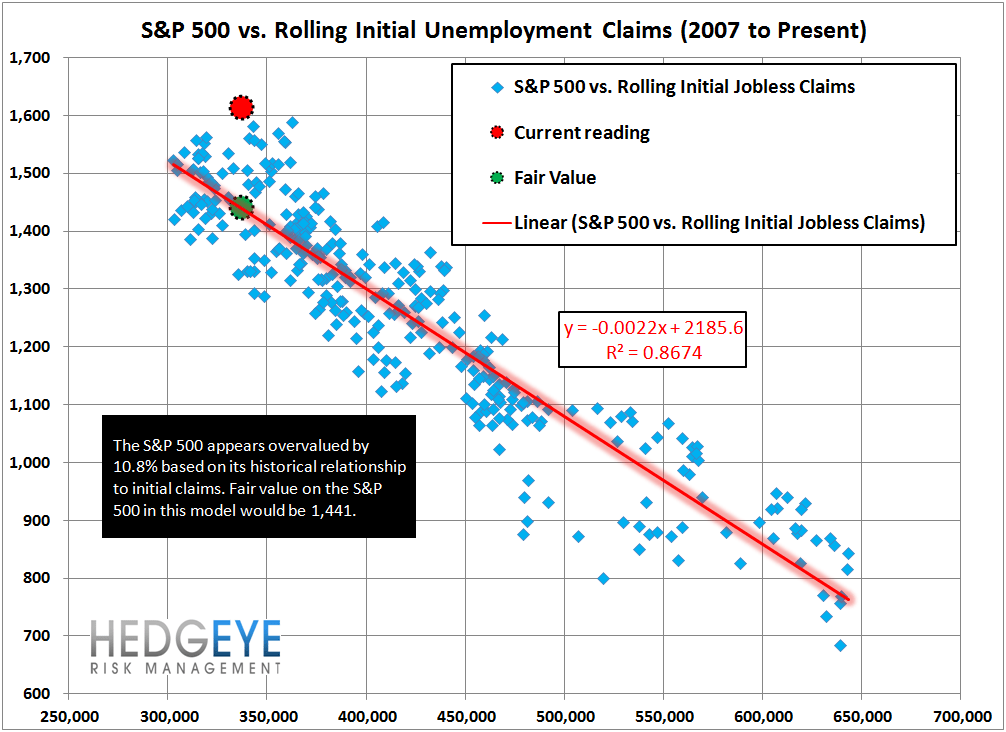

Last week we pointed out that claims had been diverging from historical trends for four weeks. This week's print brings that divergence to five weeks. NSA claims last week were 12.5% lower than the same week last year. 4-week rolling NSA claims last week were lower by 9.3% vs last year, an improvement vs. 8.4% the prior week. The seasonally-adjusted data is obviously very strong as well.

To reiterate, the strength in the underlying labor market over the last few weeks is strong enough to more than offset the seasonality distortions we regularly highlight. This continues to turn the duck & cover in May dynamic on its head. It doesn't hurt that the housing metrics are also strengthening, though this shouldn't be surprising as the two (labor & housing) are closely co-integrated.

Is ACA Driving Hiring?

An interesting question worth asking is Why? Why is the labor market showing accelerating improvement? One hypothesis we've been considering is the ACA impact on low-wage, high employment industries like restaurants, hotels, etc. Under ACA (i.e. Obamacare), employers with 50+ employees must provide healthcare to employees who work 30 hours or more per week. Part-time (those under 30 hours) and temp workers are exempted from the requirement. Industries like restaurants and hotels, that employ huge numbers of relatively low-wage earners, would see their costs rise materially under ACA. Not surprisingly, many employers are quietly seeking to sidestep ACA by cutting workers to sub-30 hours and offsetting the lost hours by hiring additional part-time and temp workers.

Anecdotally, we've been reading a lot of articles about temp agencies seeing significantly higher demand of late. We ran across one that quoted an analyst at another firm saying that when Massachusetts implemented its universal healthcare plan, growth in hiring of temp workers in the state ran at six times the national average.

One thing to consider is that companies are treading very cautiously here from a PR standpoint. No employer wants to be seen as intentionally seeking to sidestep ACA requirements. So much of this is going on under the radar. As counterintuitive as it may seem, we think ACA is actually creating jobs in significant numbers, while simultaneously reducing many workers from full-time (40 hrs+) to part-time (sub 30).

The Numbers

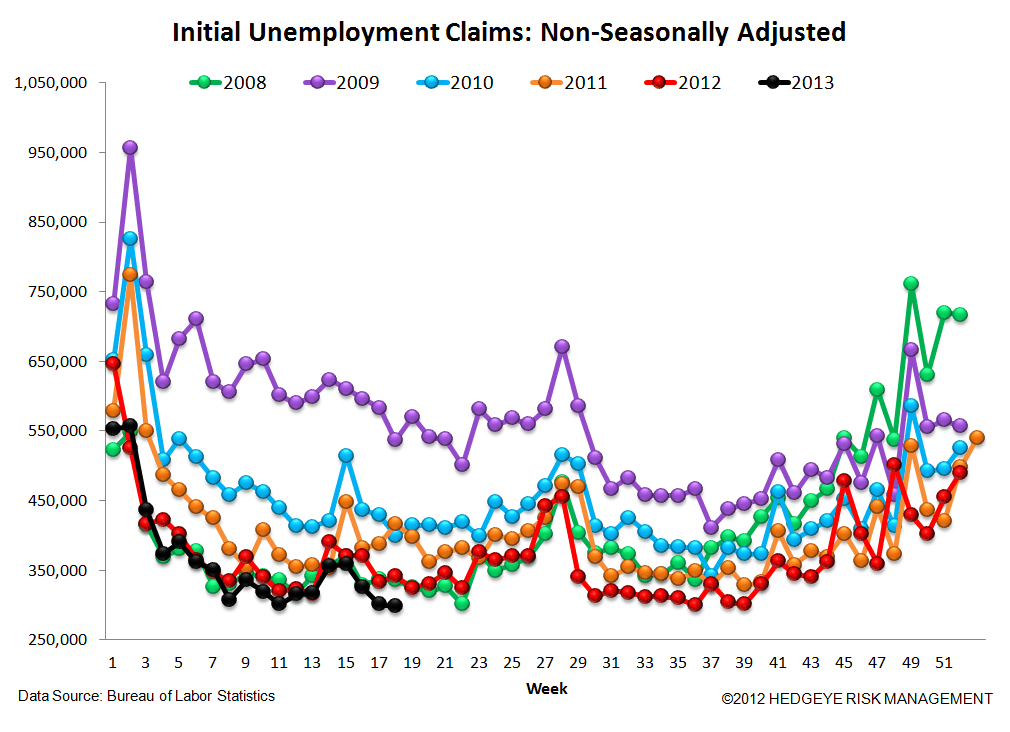

Prior to revision, initial jobless claims fell 1k to 323k from 324k WoW, as the prior week's number was revised up by 3k to 327k.

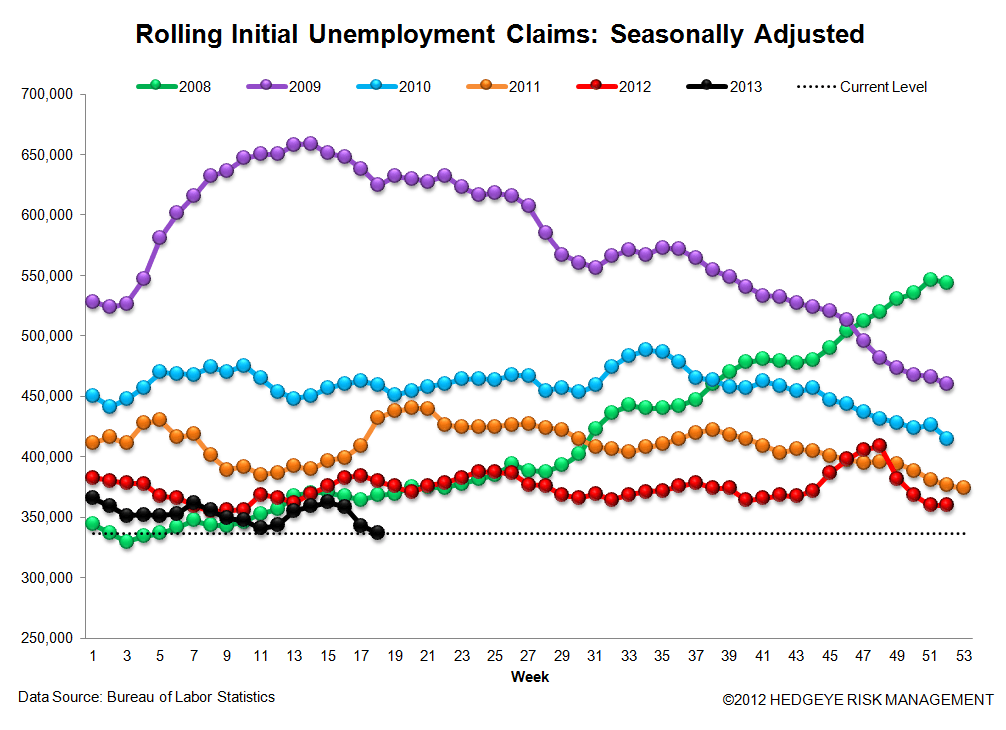

The headline (unrevised) number shows claims were lower by 4k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -6.25k WoW to 336.75k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -9.3% lower YoY, which is a sequential improvement versus the previous week's YoY change of -8.4%.

Yield Spreads

The 2-10 spread rose 12.6 basis points WoW to 155 bps. 2Q13TD, the 2-10 spread is averaging 151 bps, which is lower by -17 bps relative to 1Q13.

Joshua Steiner, CFA