This note was originally published May 06, 2013 at 15:36 in Gaming

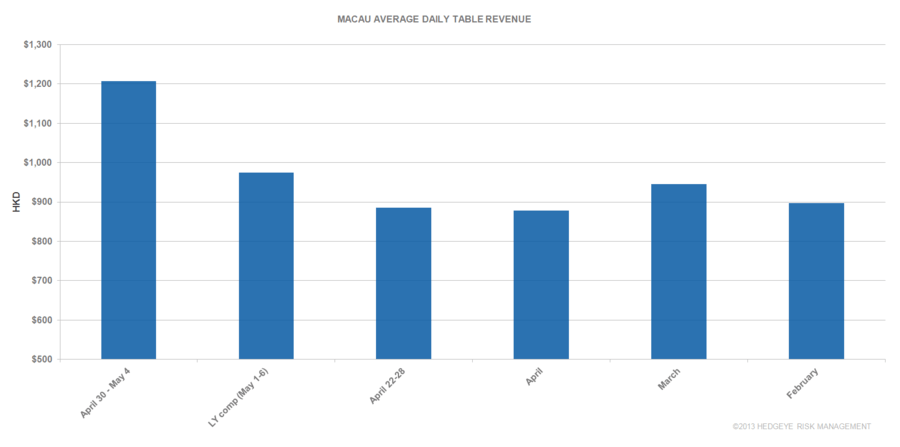

While five days of data is not enough from which to draw many conclusions, the May holiday is off to a strong start. Average table revenues for 5 days spanning April 30-May 4th were HK$1.2 billion, up 24% year-over-year (HK$975 million) and up 36% from last week’s HK$886 million. In-line with our earlier projections, we expect May gross gaming revenue growth to accelerate to 16-20% or HK$29.5-30.5 billion.

In terms of market share, Galaxy and Wynn were big gainers. Galaxy’s share shot up to 21.1% from 17.8% share in April while Wynn’s share rebounded to 12% from the April low of 9.2%. MPEL gave back its massive share gains in April and dropped back to its 6M average share of 14.0%.