This note was originally published at 8am on April 23, 2013 for Hedgeye subscribers.

“Content is often best judged in context.”

-Eric Chaisson

That’s one of my favorite thoughts from a book I have been citing as of late, Cosmic Evolution, by Eric Chaisson. In terms of how I apply it to my market model, research and risk factors are my content - time is my context.

Time and space - so valuable to contextualize, yet so susceptible to error. In this regard, risk managing markets isn’t unlike playing professional sports. As Vince Lombardi said, inches make champions. Timing matters, indeed.

This, of course, is not a unique thought process. It’s effectively the difference between Newton and Darwin. “Unlike events in classical Newtonian physics, which are time-independent, reversible, and ahistorical, in Darwinism the past history of a system contributes to its subsequent properties” (Chaison, pg31). In other words, context matters too.

Back to the Global Macro Grind…

When I say that our Global Macro Risk Management process is multi-factor and multi-duration, this is what I mean. We are a content company that contextualizes risk.

That doesn’t mean we are always right – it just means we tend to be less wrong on big stuff than most others. That’s probably because we start with the timing signal, and reverse commute on the research from there.

One of our core focuses in risk management is what Warren Buffett and Charlie Munger used to champion as Rule #1 – “Don’t Lose Money” – and maybe that’s why they love the insurance business so much. Essentially, we sell insurance too.

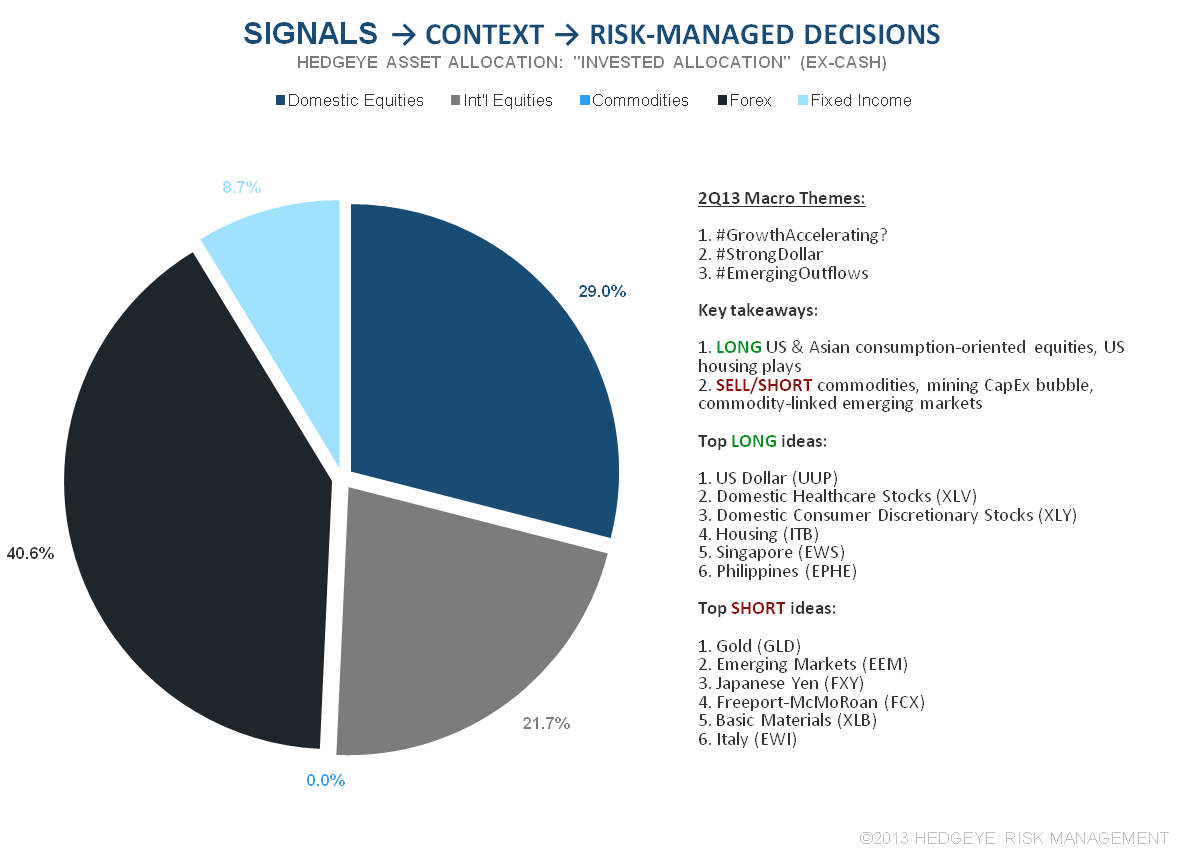

Insurance questions: what assets are bullish or bearish on our (TRADE/TREND/TAIL) model?

1. Bullish Formations (bullish on all 3 of our core durations - TRADE, TREND, and TAIL)

A) US Dollar (UUP)

B) SP500 (SPY)

C) US Consumer Discretionary (XLY)

D) US Consumer Staples (XLP)

E) US Healthcare (XLV)

F) Starbucks (SBUX) and Nike (NKE)

2. Bearish Formations (bearish on all 3 core risk management durations)

A) Commodities (CRB Index)

B) Gold and Gold Miners (GLD and GDX)

C) Silver and Copper (SLV and JJC)

D) Japanese Yen (FXY)

E) Basic Materials and Energy (XLB and XLE)

F) Russia (RSX) and Brazil (EWZ)

As a result, I think our version of Global Macro Storytelling has been succinct for the last 5-6 months. On both the long and short side, there’s a little bit of everything for everyone here. That helps make it less confusing.

The big thing about big things in macro is that they can last. That’s why the questions I wrestle with throughout my day largely surround what could change what I think is currently both causal and correlated:

1. What stops the US Dollar from going up?

2. What stops the Euro and Yen (vs USD) from going down?

3. What stops Bernanke’s Bubbles (Commodities) from popping?

Again, since I start with the signal and not the research noise, what I really need to do here is be patient. Just wait and watch for any and/or all of these three things from stopping on both my TRADE and TREND durations.

This morning’s signals marry up quite nicely to more of the same on the research content front:

- Chinese and German PMI growth data for April slowed sequentially versus March

- European #GrowthSlowing (Spain GDP -2% y/y and Swedish unemployment up to 8.4%)

- Oil, Copper, and Corn prices fall further on said “demand” slowing, as the USD rises

So, if you can’t put money in Emerging Markets like China (we’ll be hosting our #EmergingOutflows Macro Theme Conference Call at 11AM EST, ping Sales@Hedgeye.com for access), and you aren’t buying European Equities and/or Commodities because they are bearish on both our TRADE and TREND durations, what do you buy?

Markets chase price. Gravity (fund flows), like content and context, matters. The global macro flows continue into US Dollars, US Treasuries, and yes, US Consumption Equities. I’ve tried to fight gravity in markets – it rarely works.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, EUR/USD, UST 10yr Yield, VIX, and SP500 are now $1284-1435, $96.04-101.08, $3.06-3.26, $82.42-83.19, $1.29-1.31, 1.65-1.76%, 14.07-18.76, and 1531-1603, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer