This note was originally published at 8am on April 22, 2013 for Hedgeye subscribers.

“Our trepidation about Volcker’s appointment was later justified.”

-Jimmy Carter

That’s what the outgoing President of the United States had to say about Paul Volcker because, “on Thursday, September 25, 1980, the Federal Reserve Board had approved by unanimous vote a one percentage-point increase in the discount rate to 11 percent.”

“Former Fed Chairman, William McChesney Martin led the counter attack. He termed Carter’s comments “deplorable”… a “serious and unfortunate thing”, and added … partisan politics ought not to be around the Dollar.” (Volcker: The Triumph of Persistance, pg 190)

Of course, by the time Carter was losing the election markets were already front-running the US shift in monetary policy. After hitting an all-time high in January of 1980 ($850/oz), Gold didn’t see those highs again for 3 decades. For Gold Bulls, that was a long-time to average down.

Back to the Global Macro Grind…

To be balanced, according to the Gold Bulls of 2013, this time is different. Rather than acknowledging that the market has already discounted the greatest combination of deficit spending and money printing in US history, they’re digging in.

Gold isn’t trading on what they think it should trade on – it’s trading on both absolute and relative expectations vs the US Dollar:

1. ABSOLUTE: On the monetary policy side, no iQe5 upgrade of Gold is coming out of Jackson Hole this year (Bernanke isn’t even going to be there). And on the fiscal side, sequestration combined with US Consumption #GrowthAccelerating, is USD bullish.

2. RELATIVE: Japan is going to print to infinity and beyond and the probability of the Europeans cutting to 0% is rising. Both are bullish for the US Dollar relative to the Yen and the Euro. What’s bullish for the USD remains bearish for Gold.

Last week was another reminder of that:

- US DOLLAR = +0.9% on the week (up for the 7th week in the last 10 and +4% for 2013 YTD)

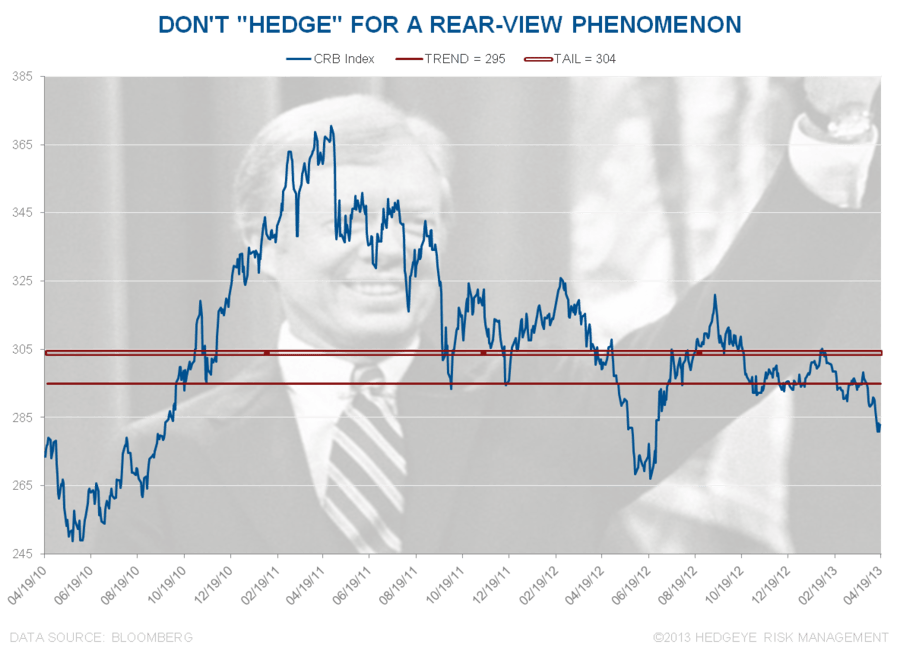

- CRB Commodities Index = -1.4% on the week (down for the 8th week in the last 10 and -4% for 2013 YTD)

- GOLD and SILVER = down -7% and -13% last week, respectively (taking Gold’s YTD decline to -16.9%)

All the while, the Gold Bulls continue to say almost the opposite of what we have been ranting about for 6 months. Paulson & Co. wrote to their investors that central bank “stimulus will eventually lead to inflation.” But that’s my point, eventually already happened.

We already had the greatest commodity inflation in world history. If the most asymmetric long-term move in all of Global Macro continues higher from here (#StrongDollar), this will continue to be an epic #CommodityDeflation, not inflation.

Don’t take my word for it – ask Mr Market, what was priced in when Bernanke said he’d go to infinity and beyond (6 months ago)?

- Silver is down -29% in the last 6 months

- Rubber is down -25% in the last 6 months

- Japanese Yen is down -25% in the last 6 months

Again, if you get the US Dollar right, you’ll get a lot of other big things right. There are plenty of other ways to make money on this other than being short Gold and Copper Miners (we remain short Freeport, FCX, btw):

- Emerging Markets (EEM)

- Russian Stocks (RSX)

- Peruvian Stocks (EPU)

Peruvian stocks? You have to be kidding me Mucker. Who the heck do you think you are making calls on Peru – what’s next, Peruvian Par Bonds? Ha! Actually Peru just dipped inside of Russia for the world’s 2nd worse performing stock market YTD (Cyprus is the worst at -15%).

The reason why you shouldn’t have your 401k choking on Peru is the same as why you shouldn’t have it stuffed with Gold, Silver, or Corn. Peru a commodity economy (85% of exports) and its stock market is 37% indexed to Basic Material and Energy stocks.

As a point of reference, only 13% of the SP500 is in Basic Materials and Energy. And we don’t want you to be long those S&P Sectors (XLB and XLE) either. Energy (XLE) led USA’s losers last week at -4.4%, only to be outpaced by Russian stocks (on the downside) at -4.9%!

How important is it for a Global Macro investor to get the world’s reserve currency right? Is it all interconnected? If you invest in Global Macro, do you have to get growth and inflation right too? We think the answers to these basic questions are self evident. That’s why we built our proprietary Growth/Inflation/Policy (GIP) Model.

That’s also why our views on growth and inflation have been different from consensus for a long time now. We get the #GrowthSlowing via US Dollar Debauchery inflation call (it’s a call we made consistently from 2007-2012). And when you see this week’s US preliminary GDP Growth print (Friday), sequentially in Q113 you’ll see #GrowthAccelerating as #CommodityDeflation takes hold too.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, EUR/USD, UST 10yr Yield, VIX, and the SP500 are now $1284-1454, $96.02-101.62, $82.41-83.14, 97.12-101.06, $1.29-1.31, 1.68-1.76%, 14.05-18.69, and 1532-1568, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer