In line with the Hedgeye Macro Team’s call, this morning’s April jobs data was indicative of a continuing bullish trend in the U.S. economy. The narrower data sets released along with the headline numbers were, on balance, positive for the restaurant space as accelerated employment growth in younger age cohorts suggests that sales at QSR and fast casual are likely to remain strong into 2Q.

Employment by Age

Employment growth by age data continue to imply that quick service restaurants are benefiting from improving job growth in the younger age cohorts while casual dining also benefitted (albeit to a lesser degree) from a sequential improvement in the employment growth rates in older age cohorts. The sequential acceleration/deceleration in employment growth among the respective age cohorts illustrated below ranged from -60 bps (25-34 YOA) to +162 bps (20-24 YOA). We would highlight that employment growth among the youngest age cohort in the chart below is frequently referenced by companies and industry operators as being crucial for restaurants chains’ top line growth.

We remain bullish on SBUX, CAKE, DRI, and JACK, and are bearish on BWLD, MCD and PNRA.

Industry Hiring

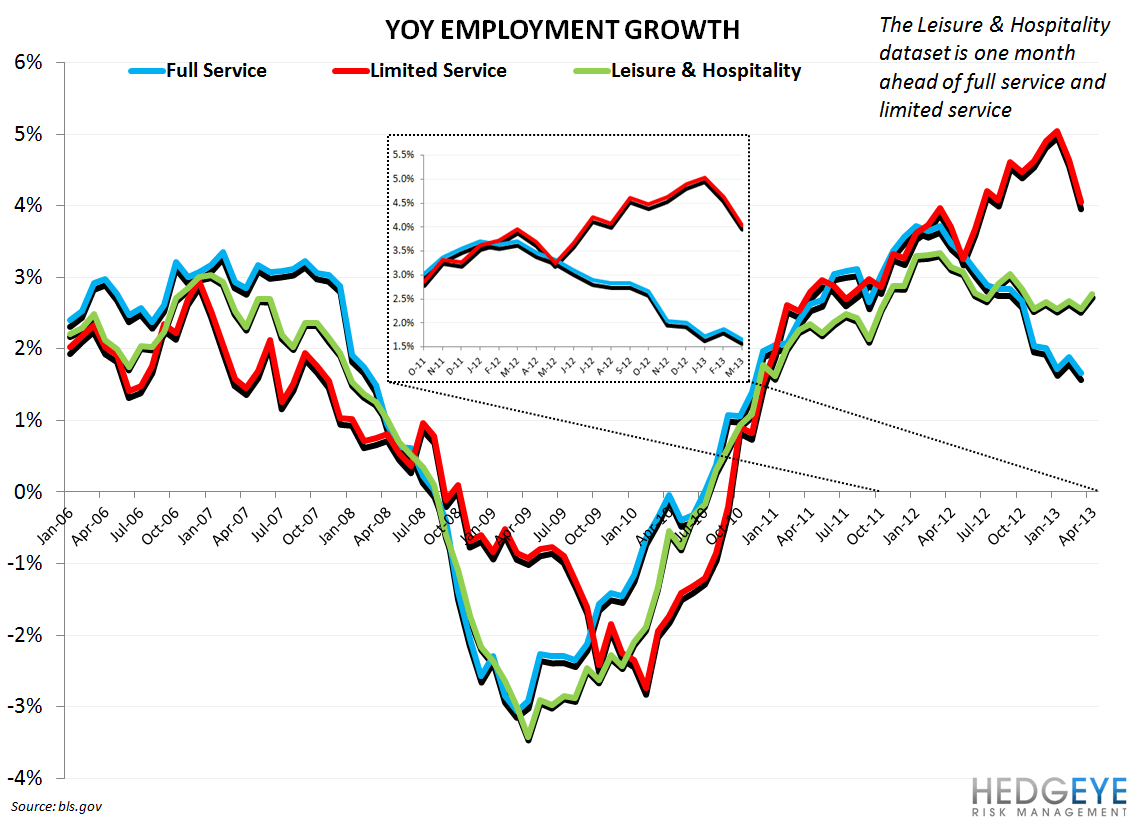

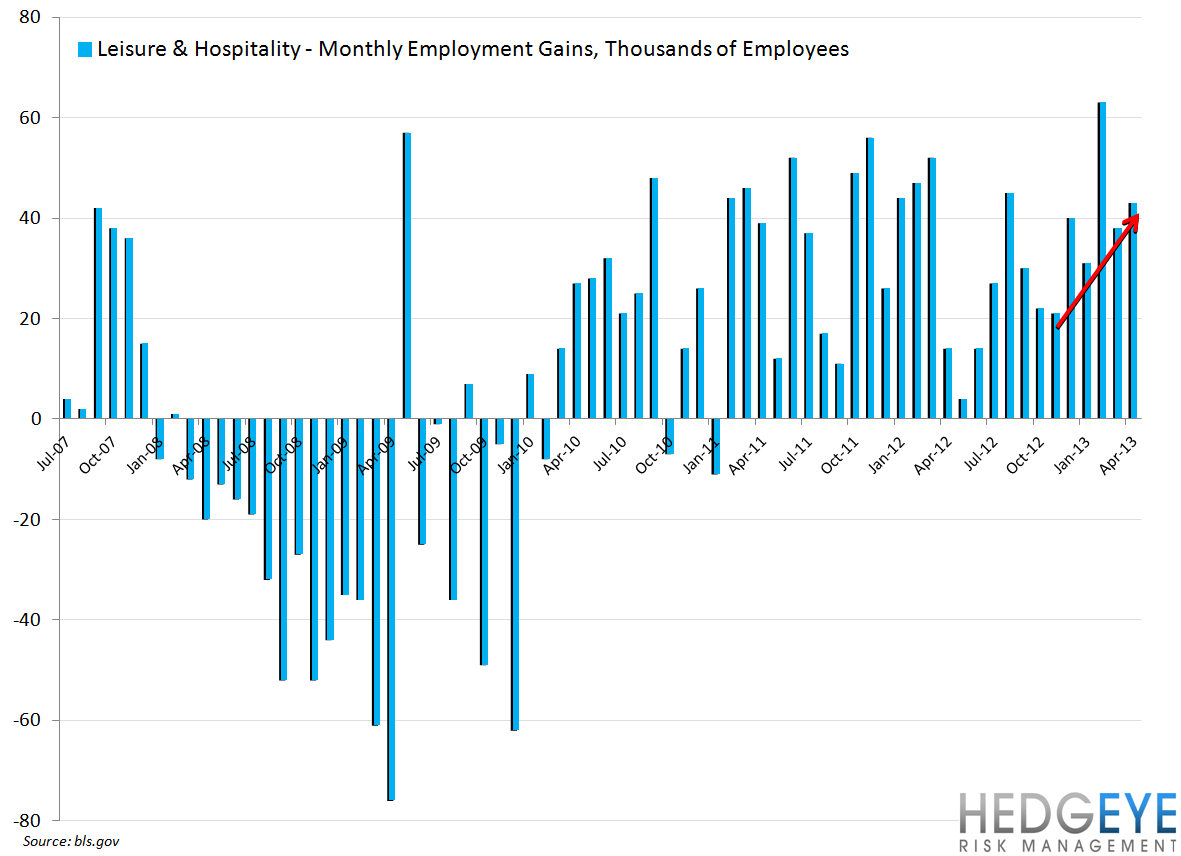

The Leisure & Hospitality employment data, which leads the narrower food service data by one month, suggests that employment growth in the food service industry may have ticked up in April, consistent with the commentary of several management teams during the recent earnings period. On a sequential basis, Leisure & Hospitality employment data registered a month-over-month gain of 43k (second chart below), an acceleration from the prior month’s 38k month-over-month gain.

Sequential Moves:

- Leisure & Hospitality: Employment growth at +2.8% in April, up 21 bps versus March

- Limited Service: Employment growth at +4.1% in March, down 60 bps versus February

- Full Service: Employment growth at +1.6% in March, down 22 bps versus February

Howard Penney

Managing Director

Rory Green

Senior Analyst