Am I the only one who is floored that Adi only traded down 11% on the earnings release? This quarter was U-G-L-Y. Sales -2% and Inventories +28% with an 80% decline in operating profit? Closing stores in what was its fastest growing market (China)? Restructuring Reebok - again? It's been a long time since I've seen such a large company lose control of its business so quickly. So many of the issues here are Adidas-specific, but although Adi is a speck in the US market, its global market share is meaningful (US$15bn in sales vs. Nike at $18.6). Adi is on the ropes, and future moves of desperation will put some unwanted pressure on NKE. Keep an eye on this one.

Here are a few notable margin drivers...

Gross Margins:

- ~200bps due to higher input costs - raw material and wages.

- o Expected to ease in 2H, but not positive until 2010.

- o NKE noted a similar expectation for visible improvement on its March earnings call.

- ~150bps due to the impact of foreign currency - particularly the devaluation of the Russian Ruble.

- o Over 90% of ADI's Russian business is through owned retail stores

- o Price increases will be used to offset this impact though only minor

- o We estimate that Russia represents ~10% of the NKE's EMEA sales equating to <3% of total sales.

- ~50bps due to the promotional environment

- o 50% of this is a company specific issue related to bloated inventories in China

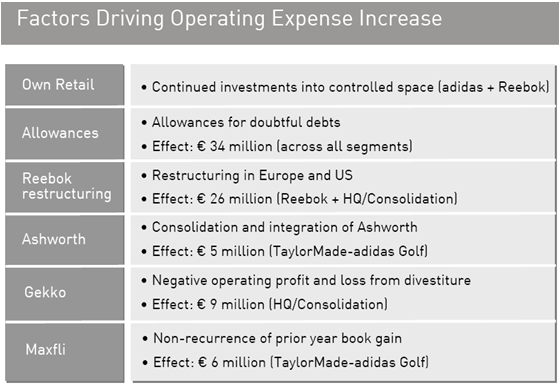

Higher operating expenses were entirely company specific as detailed in the slide below. As it relates to sales, ADI announced on their Q2 F2008 call in March that they are no longer providing backlog numbers limiting read through on a regional basis (convenient when business is tanking); However, management remarked that emerging markets (up 16%) are expected to outperform all other markets in 2009. Not tough for emerging markets to outperform when major markets like the US are down double digits.