Labor Market, Housing, and (now) Confidence Trends all continue to accelerate. Ongoing improvement in the Housing and Labor markets should further support consumption as the slope of recovery in household income and net worth accelerates. Moreover, ongoing improvement in the domestic macro data is supportive of our bullish view on the U.S. Dollar on both an absolute basis and on a relative basis as US fiscal and monetary policy expectations get tighter, on the margin, while ECB and BOJ fiscal/monetary policy expectations get looser, on the margin.

Positive consumer related data in combination with expectations for further $USD appreciation keeps our Strong Dollar – Strong Domestic Consumption (Down Commodities) theme the predominant strategic framework driving our equity and asset class exposure.

Below we summarize this morning’s claims data along with the consumer confidence and housing data of the last week.

Initial Claims: How Low Can We Go?

The positive acceleration in labor market trends continued this week with both the seasonally adjusted and non-seasonally adjusted Initial Jobless Claims series showing sharp sequential improvement. The headline number fell 15K to 324K w/w versus the prior week’s unrevised number while the 4-week rolling average in SA claims fell -16.5K w/w to 342K.

The 4-week rolling average in NSA claims, our preferred judge of trend with respect to underlying conditions in the labor market, improved 240bps w/w with the year-over-year change in 4-wk rolling claims improving to -8.6% Y/Y from -6.2% Y/Y the week prior, and -3.8% two weeks prior.

Given the ongoing and marked improvement in the claims series, how much additional upside could we seen from current levels? Our head of financials, Josh Steiner, answered that question in the context of the historical cycles observed over the period 1967-present:

Thinking longer term about the setup, rolling claims (SA) are currently at 342k with the most recent week at 324k. The first chart below shows the claims history (rolling SA) back to 1967. Every economic cycle since the late 1970s has seen claims trough at around 300k. To be precise, in prior cycles, claims bottomed at:

* 312k November, 1978

* 287k January, 1989

* 266k April, 2000

* 286k February, 2006

This works out to an average of 288k with a standard deviation of 19k (on a very small sample). In other words, we're still 54k above historical cycle troughs or roughly 2.8 standard deviations, a pretty healthy margin of error for the bull case.

In short, rolling NSA claims are 8.6% lower than last year and the positive improvement is accelerating. Moreover, the current, positive trend is overwhelming both the negative seasonal distortion currently present in the data and any negative sequestration related drag.

Source: Hedgeye Financials

Consumer Confidence: The Bloomberg Consumer Confidence Index made a new 5Y high two weeks ago with confidence measures across age and income demographics showing broad improvement. The index held those gains last week and made a new 5Y with this morning’s reading improving to -28.9 from -29.9 w/w. The Conference Board Consumer Confidence as well as the University of Michigan Consumer Sentiment readings were confirmatory with the lastest, April readings accelerating sequentially to 68.1 and 76.4, respectively.

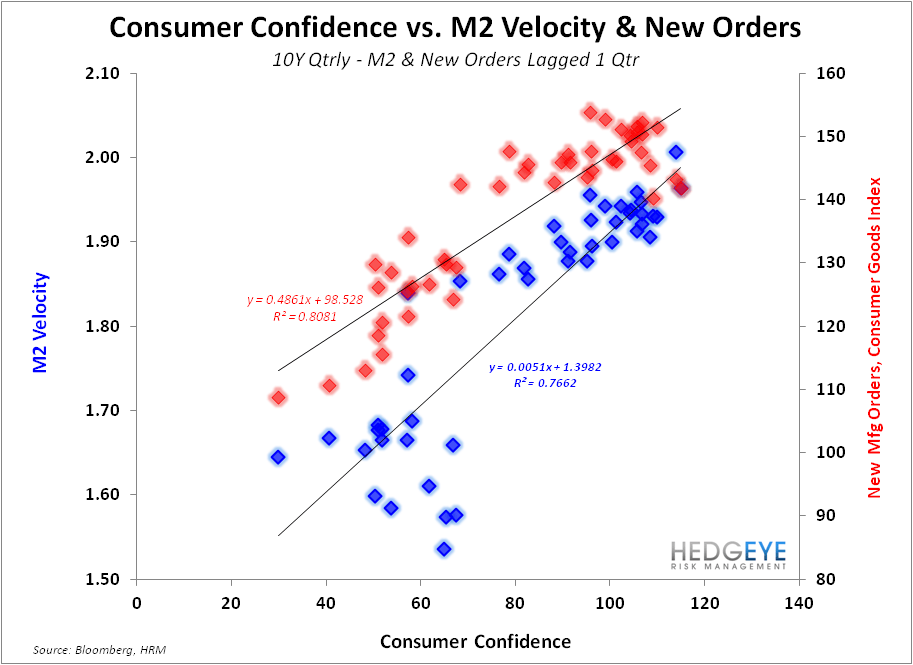

For most of the last 4 years, historical relationships with economic data have broken down with correlations moving towards zero as confidence readings have largely tracked sideways. Over the longer-term, consumer confidence has served as a decent to very good lead indicator for economic activity. For example, on a 10Y basis, lagged correlations to New Manufacturing Orders, PCE Services, and M2 velocity are all > 0.85. With consumer confidence readings beginning to break out here alongside ongoing improvement in the housing and labor markets, we’re monitoring for any re-tightening in the relevant confidence-econ activity correlations a little more closely

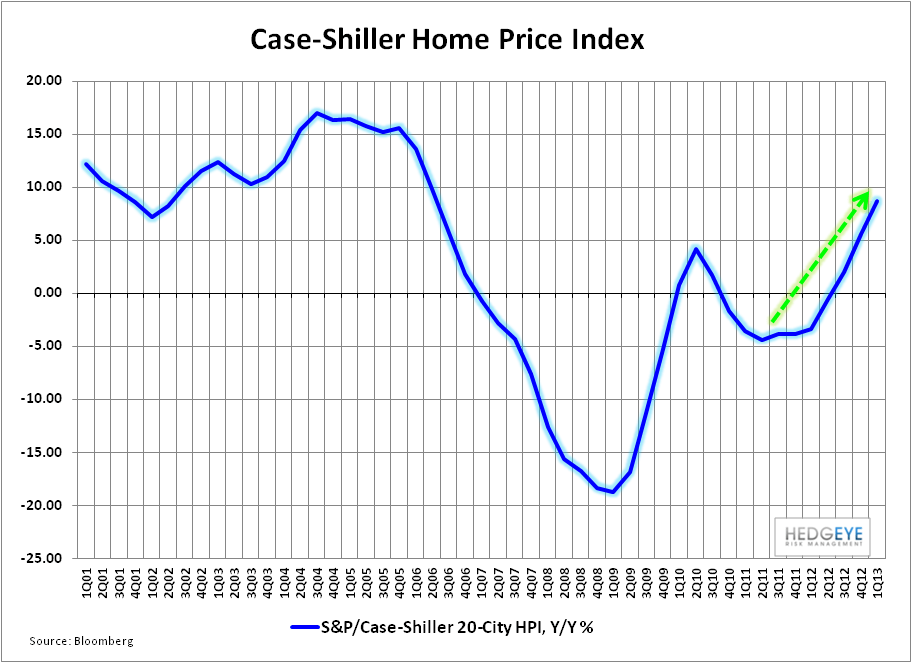

Housing: We provided a summary recap of the most recent housing data last week (HERE). Incremental data over the past week has reflected more of the same as Mortgage Purchase Applications remained at their YTD highs while the Pending Home Sales and Case-Shiller HPI data both accelerated sequentially. The Purchase application data and Pending Home sales numbers both suggest forward housing demand should remain strong.

Additionally, President Obama’s likely nomination of Congressman Mel Watt to replace Ed DeMarco as head of the FHFA should be taken as a positive catalyst for housing. DeMarco has opposed underwater principal forgiveness for GSE borrowers – a stance that may be lightened should Watt be confirmed.

Christian B. Drake

Senior Analyst