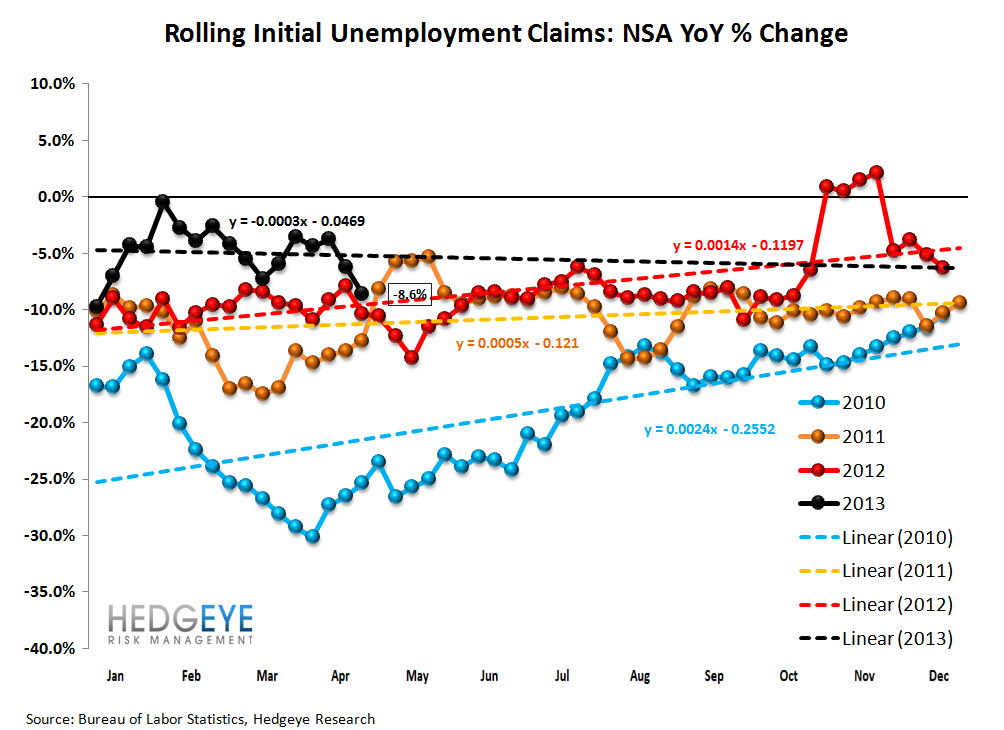

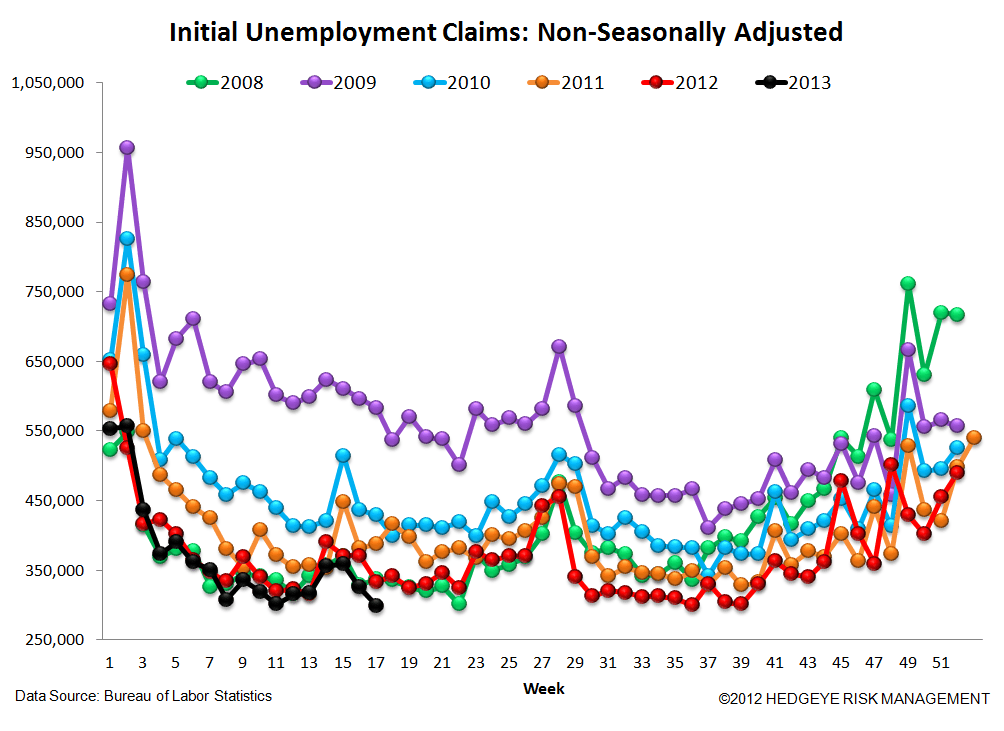

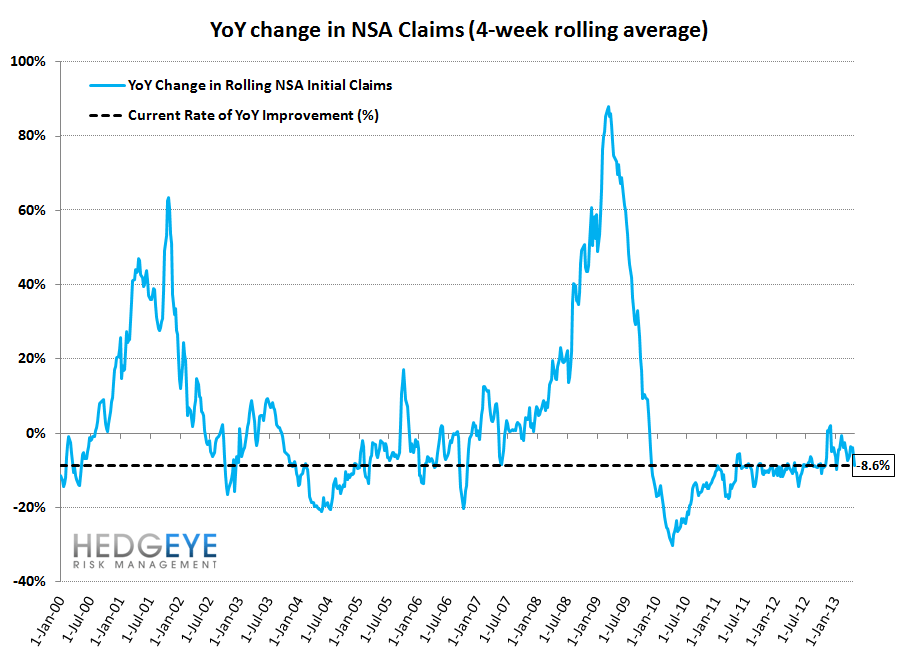

The last four weeks have seen a notably positive divergence from both trend and historical perspectives. The last two weeks have shown the sharpest improvements. Our preferred method for evaluating labor conditions is the year-over-year rate of change in the non-seasonally adjusted initial jobless claims. In the last three weeks, that figure has been -3.8%, -6.2% and today -8.6%. In other words, rolling NSA claims are 8.6% lower than last year.

One of our central tenets in thinking about the big picture for Financials has been this recurring dynamic in seasonal distortions, as it has correlated tightly with sector performance for the last three years. Interestingly, the strength in the underlying labor market over the last few weeks is strong enough to more than offset the seasonality distortions. This is, for now, turning the sell-in-May dynamic on its head. It doesn't hurt that the housing metrics are also strengthening, though this shouldn't be surprising as the two (labor & housing) are closely co-integrated.

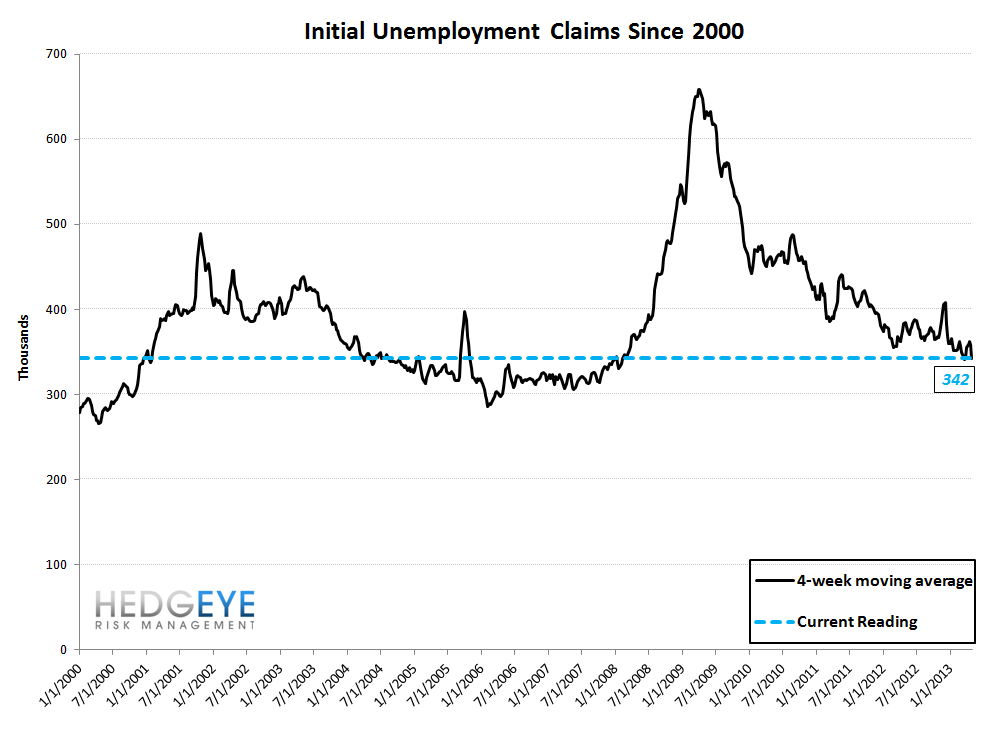

How Low Can Claims Go?

Thinking longer term about the setup, rolling claims (SA) are currently at 342k with the most recent week at 324k. The first chart below shows the claims history (rolling SA) back to 1967. Every economic cycle since the late 1970s has seen claims trough at around 300k. To be precise, in prior cycles, claims bottomed at:

* 312k November, 1978

* 287k January, 1989

* 266k April, 2000

* 286k February, 2006

This works out to an average of 288k with a standard deviation of 19k (on a very small sample). In other words, we're still 54k above historical cycle troughs or roughly 2.8 standard deviations, a pretty healthy margin of error for the bull case.

The Numbers

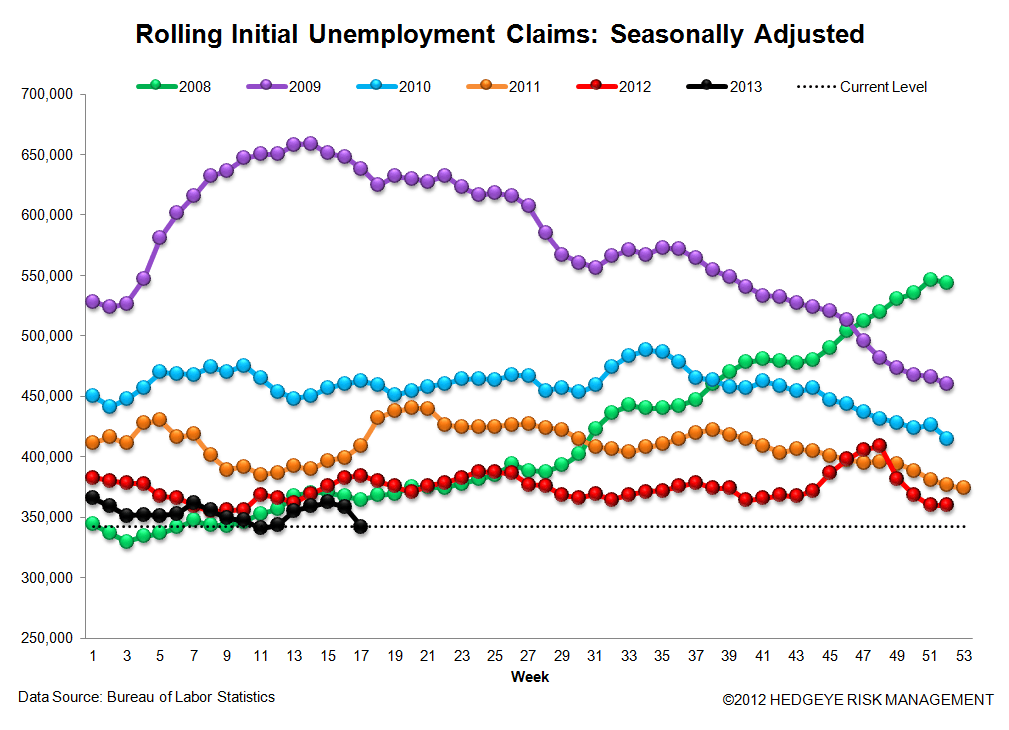

Prior to revision, initial jobless claims fell 15k to 324k from 339k WoW, as the prior week's number was revised up by 3k to 342k.

The headline (unrevised) number shows claims were lower by 18k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -16.5k WoW to 342.25k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -8.6% lower YoY, which is a sequential improvement versus the previous week's YoY change of -6.2%

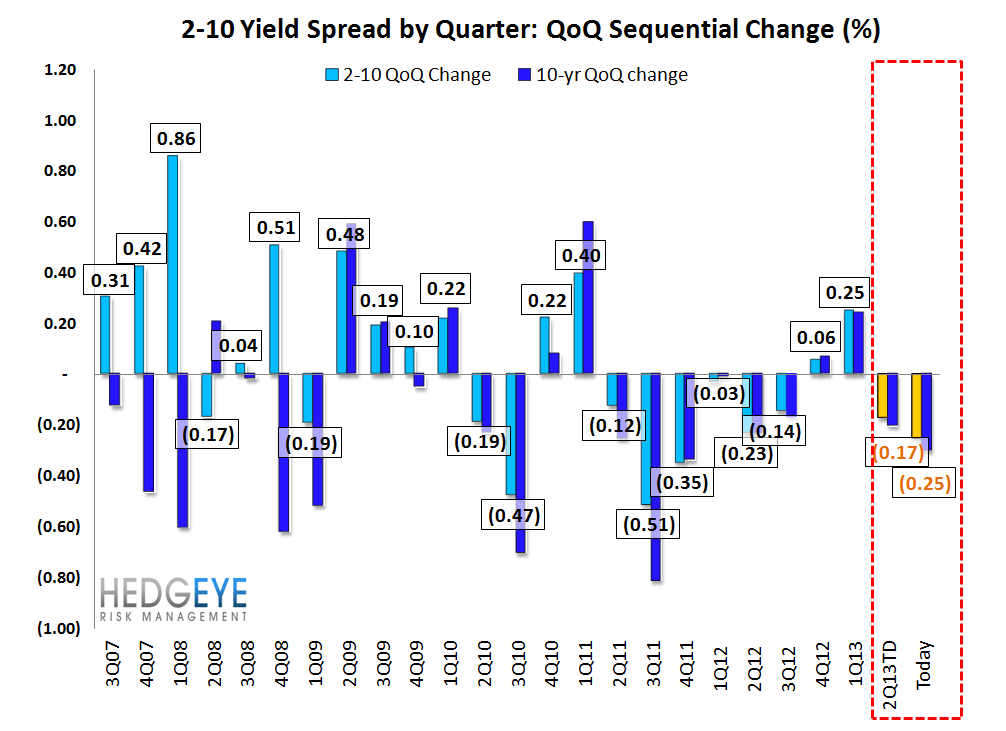

Yield Spreads

The 2-10 spread fell -4.7 basis points WoW to 143 bps. 2Q13TD, the 2-10 spread is averaging 150 bps, which is lower by -17 bps relative to 1Q13.

Joshua Steiner, CFA