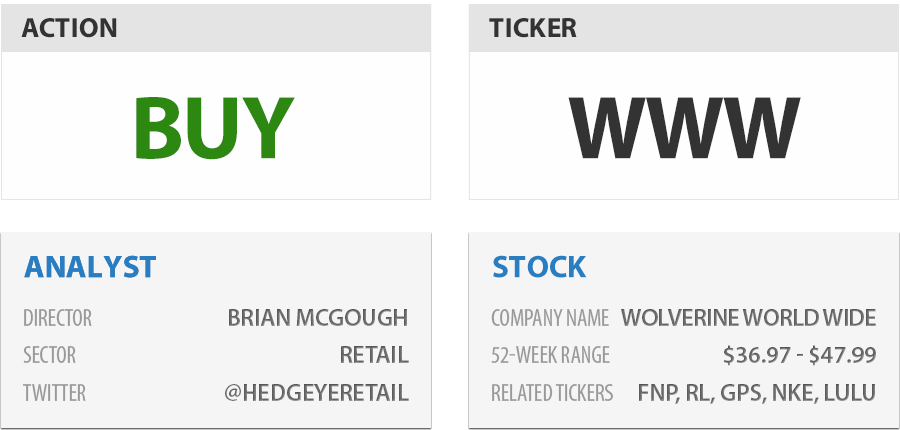

THE HEDGEYE EDGE

WWW is one of the best managed and most consistent companies in retail. We’re rarely fans of acquisitions, but the recent addition of Sperry, Saucony, Keds and Stride Rite (known as PLG) gives WWW a multi-year platform from which to grow.

We think that the preailing bearish view is very backward looking and leaves out a big piece of the WWW story, which is that integration of these brands into the WWW portfolio will allow the former PLG group to achieve what it could not under its former owner (most notably – international growth, and leverage a more diverse selling infrastructure in the US). Furthermore it will grow without needing to add the capital we’d otherwise expect as a stand-alone company – especially given WWW’s consolidation from four divisions into three -- which improves asset turns and financial returns.

The stock is hardly washed out – we get that. But the reality is that this for a high quality globally diversified portfolio that has consistent 20-30% EPS growth and improving returns we don’t think that arguing a high teens multiple is a stretch. 18x our 2014 estimate of $3.55 gets us to a $64 stock, or 36% above current levels. Take that out to 2015 and 2016 and we’re looking at $75 and $95, respectively. When we juxtapose that alongside 15x what we think is a worst case $2.50 in EPS power, we’re looking 3 to 1 upside/downside over the course of a 12-18 months.

TIMESPAN

INTERMEDIATE TERM (the next 3 months or more)

There is currently a bifurcation between the Legacy business and the new PLG brands. Due to heavy exposure to a) Europe, which is in a perennial recession, b) the US industrial economy with its CAT, Harley and HyTest brands, and c) the cold-weather outdoor boot business through its Merrell brand – which has been shellacked two years in a row due to unfavorable weather – the Legacy brands are under pressure. But accretion in the PLG brands is well ahead of plan. The company is playing down the combination synergies – and in fact is dodging the topic at all costs. Our sense is that it wants 2013 to be the year of ‘accretion’ while ’14 and ’15 will be the year of synergies.

LONG-TERM (the next 3 years or less)

PLG was only 5% outside of the US under its former owner, but WWW’s legacy business was 40% outside of the US due to its strong International distribution network of 10,000+ points of distribution in over 200 countries. As WWW layers these new brands over its infrastructure, we think it can drive double-digit growth in this billion dollar business while lowering unit costs. That gets us to 7-8% consolidated top line growth, 15-2-% EBIT growth, and 20%+ EPS growth. Add on accelerated cash flow generation and subsequent debt paydown, and we think that this story has legs.

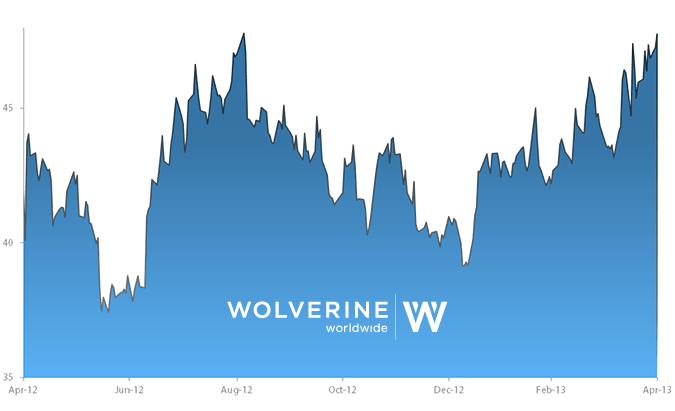

ONE-YEAR TRAILING CHART