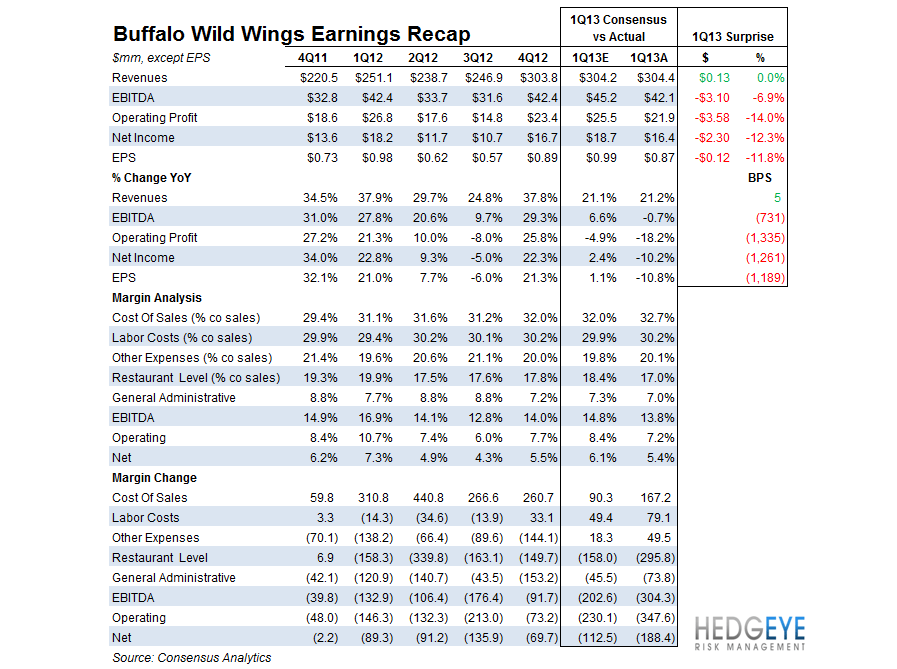

Buffalo Wild Wings reported a disappointing quarter last night with EPS coming in at $0.87 versus consensus of $0.99.

Conclusion

We believe this stock is a short here ($90.20/share) as the company is expanding its new wings-per-portion serving practice. Despite the sequential comp acceleration from 1Q to April, we believe there are several overriding factors that will drag on the stock’s performance over the next 3-6 months:

- The new service initiative (wings by weight) has been tested in only 40 stores and produced flat-to-down comps vs +1.4% co-op comps but is being rolled out to all co-op stores by end of June

- Traffic was negative in 1Q (-290 bps), April (-130 bps excl Easter)

- Flex pricing will likely materially impact guest experience (5 wings vs. 6, 10 vs. 12, etc.)

- Consensus is expecting +1.2% and +1.6% traffic in 3Q and 4Q, respectively

- Labor costs increasing due to training costs related to “guest experience model” (wings by weight)

- Margins are likely going to deteriorate further from here

- Wing prices declining will mitigate some margin pressure but labor pressure seems significant and if

- Mgmt has no credibility when it comes to guidance after 2012

- FY13 EPS growth guidance of +17% (unch’d from prior) is a Hail Mary after an 11% decline in 1Q13

Notable Earnings Call Quotes:

ON LABOR GUIDANCE OF +80 BPS FOR 2Q

“Well, I think we're just being cautionary. We did see 80 basis points in the first quarter. We definitely have full attention to how we're rolling out this guest experience business model. And so we do believe that there is improvement to have on that as we go through the year. We're just not confident at this point in the second quarter on whether or not we'll see all of that. So we do think that for at least the near term an increase similar to Q1 is the most appropriate guidance.”

HEDGEYE: In response to an earlier question on guidance provided in February, management said, “We wouldn't have had a full view of our labor at the time that we did our February earnings call.” We would echo those sentiments with regard to labor for the balance of 2013. We believe the likelihood of management underestimating the impact of different initiatives on labor is high. Examples include training staff to handle the flex pricing initiative, training an additional staff member as “guest experience captain”, etc. In 2012, management underestimated cost headwinds and we think labor is the 2013 iteration of that same mistake.

ON TEST MARKET REACTION AND EXPECTED CHANGE IN NUMBER OF WINGS PER SERVING

“Initially, same-store sales are flat to just slightly down. What the most important thing to the guest is to really understand how many wings they're getting... Well, we do plan to roll it with our July menu rollout and if wing sizes stay at the same place they are today, people would see a 5, 10, 15, 20 count as compared to the 6, 12, 18, 24. But if wing prices are different when we get to July, that could change – sizes, yes.”

HEDGEYE: What if the rollout across the system has a similar comp impact, in terms of the underlying trend? We expect that co-op comps in the back half of the year would be 2.5% and 2.9% for 3Q and 4Q, respectively. Consensus is modeling 3.3% and 3.6% for 3Q and 4Q co-op comp sales growth. Judging by the estimate of the serving portion size changes, outlined in the quote above, we expect this change to have a material impact on brand perception.

Earnings Recap

The table, below, provides an overview of the quarter’s key results versus what consensus was expecting. Revenues came in ahead of expectations thanks to better-than-expected comps and April comparable sales growth is tracking at 5.2% versus the Street at 3.8%. An important caveat is that the Easter shift helped by 150 bps and price is running at 5% so traffic is down 130 bps.

Howard Penney

Managing Director

Rory Green

Senior Analyst