This note was originally published at 8am on April 16, 2013 for Hedgeye subscribers.

“We cannot predict where it might be headed in the future, but we can describe how it came to be in the past.”

-Eric Chaisson

First, my entire team’s thoughts and prayers go out to all of the people affected by the horrible act at the Boston Marathon yesterday.

Without having inside information, predicting an external event like that is impossible. So is consistently predicting tops and bottoms in markets. They are processes, not points. It’s my job to A) contextualize the past so that B) I put us in the best position I can for the future.

Yesterday’s market collapse started with more of what has been happening for months – commodities collapsing. Combine intermediate-term TREND collapse with an immediate-term external event and you run out of time and space into the market’s close. That’s why describing where we came from to reach an intraday capitulation like that is critical this morning.

Back to the Global Macro Grind…

Historical Context:

- SP500 was immediate-term TRADE overbought into last week’s all-time closing high of 1593 (so we made sales there)

- CRB Commodities Index was already in a Bearish Formation going into yesterday’s open (bearish TRADE/TREND/TAIL)

- Gold was not only in a Bearish Formation into Friday’s close, it started crashing pre-open yesterday too

Crashes (20% peak-to-trough declines) are very bad. We don’t buy those. Predicting The Past on that score is actually quite easy. Old Wall calls it “catching a falling knife” for a reason. Unless you have a catalyst, “cheap” gets a lot cheaper during a crash in price expectations.

But the thing about the past, on both things that matter to our process (Research and Risk Signals) is that you can see it today. That’s why our Research and Risk Management Models often get lucky in not being long something like Gold, Energy, or Brazil on days like yesterday. A multi-duration, multi-factor, Research and Risk Management #Process makes its own luck.

Describing how Bernanke’s Bubble (Commodities) is deflating is actually quite easy. You simply have to accept causality in terms of what made Bubble#3 (Greenspan/Bernanke Bubbles #1 and #2 were Tech and Housing) to begin with. If you reverse that causal factor’s intermediate-term TREND (Dollar Up instead of Debauched), you start describing why the Commodity/Gold Bubble is popping.

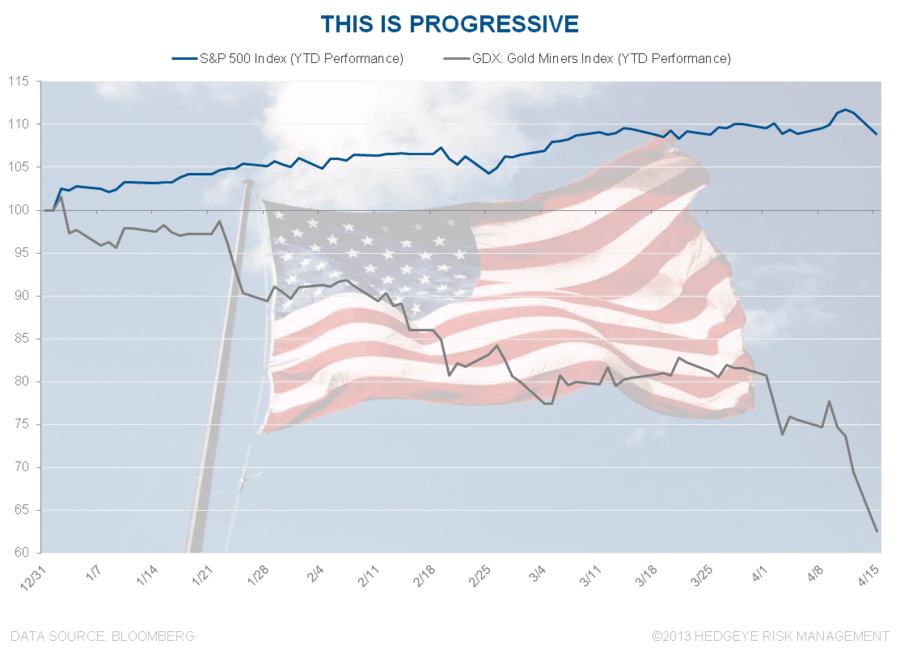

Reviewing 2013 YTD:

- Gold Miners (GDX) are down -37% YTD

- Gold is down -18% YTD

- Copper is down -11% YTD

Freeport McMoran (FCX) is a Gold and Copper expectations proxy (that’s why we’re short it); it’s down -14% YTD. And Brazil’s stock market (the best liquid proxy for a country commodity index) is down -13.1% YTD. For the month-to-date (APR) alone, Basic Materials (XLB) and Energy (XLE) stocks are down -4.8% and -5.7%, respectively.

This is why describing where we are matters. It’s the #CommodityDeflation that’s been driving US Consumption expectations higher all year long too. Q: So on the biggest down day for both US stocks and commodities of the year, why didn’t I buy US stocks yesterday? A: it’s the signal – and, above all else, I respect the market’s Risk Management Signal.

For US stocks, let’s go through why I’m at 10 LONGS, 9 SHORTS @Hedgeye instead of sending you another “Buyem” email into the close:

- SP500 broke my immediate-term TRADE line of 1557 support yesterday (that was new)

- US Equity Volatility (VIX) broke out above my immediate-term TRADE line of 14.07 resistance yesterday

- S&P Sector Studies flagged 5 of 9 core Sectors broken on our immediate-term TRADE duration

Those 3 things, combined with a nasty volume signal (+32% vs my TREND avg), predicts plenty enough for me to do 1 thing in a situation like that (a situation I have seen many times before) – to simply wait and watch.

I’m not happy to miss a big US stock market open, but if I do, I know why I made that decision. Having sold into an immediate-term TRADE overbought signal of 1593, I’m more than happy to wait and see if the bulls recapture 1557. If they can, with intermediate-term TREND support for the SP500 (1515) and TREND resistance for the VIX (18.69) intact, predicting the past gets easier again.

My Macro Team and I will be hosting our Q213 Global Macro Themes Call at 1PM EST today. Please ping Sales@Hedgeye.com for the details. Our intermediate-term TREND to long-term TAIL Research Views will be the focus of that call. That always helps us contextualize what was confusing about yesterday’s immediate-term duration risk too.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, EUR/USD, UST10yr Yield, VIX and the SP500 are now $1291-1464, $100.21-104.79, $82.04-83.14, 95.87-102.11, $1.28-1.31, 1.69-1.76%, 14.07-18.69, and 1537-1568, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer