TODAY’S S&P 500 SET-UP – April 30, 2013

As we look at today's setup for the S&P 500, the range is 33 points or 1.48% downside to 1570 and 0.59% upside to 1603.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

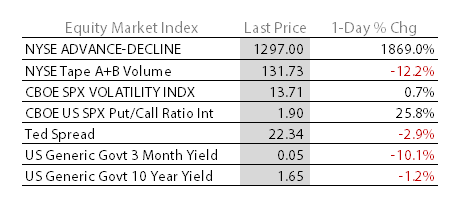

- YIELD CURVE: 1.45 from 1.46

- VIX closed at 13.71 1 day percent change of 0.73%

MACRO DATA POINTS (Bloomberg Estimates):

- FOMC opens two-day meeting

- 7:45am: ICSC weekly sales

- 8:30am: Employment Cost Index, 1Q, est. 0.5% (prior 0.5%)

- 8:55am: Johnson/Redbook weekly sales

- 9am: NAPM-Milwaukee, April (prior 50.98)

- 9am: S&P/CS 20 cities, M/m SA, Feb., est. 0.80%

- 9am:S&P/CS Composite 20 cities, Y/y, Feb., est. 8.90%

- 9am: S&P/CaseShiller Home Price Index, Feb. (prior 146.14)

- 9:45am: Chicago Purchasing Manager, April, est. 52.6

- 10am: Consumer Confidence, April, est. 60.0 (prior 59.7)

- 11am: Fed to purchase $4.25b-$5.25b notes in 2017 sector

- 11:30am: U.S. to sell 4W bills, $23b 52W bills

- 4:30pm: API energy inventories

GOVERNMENT:

- House meets in pro forma session, Senate not in session

- Federal Open Market Cmte meets on eco, interest rates, 9am

- Bloomberg LINK holds Washington Summit w/ CFTC Chairman Gary Gensler, FCC Chairman Julius Genachowski, Lazard Vice Chairman Gary Parr, White House CEA Alan Krueger, CAP Chairman John Podesta, Va. Gov. Bob McDonnell, 8am

WHAT TO WATCH

- KKR said to weigh bid for Rio Tinto Australia copper mine stake

- Best Buy exits Europe with sale of stake to Carphone Warehouse

- CBOE plans post mortem on response, procedures amid outage

- BofA urges dismissal of U.S.’s $1b faulty mortgages suit

- Time Warner Cable appoints AOL’s Minson CFO as Esteves departs

- MBIA bid for pretrial ruling in Countrywide lawsuit is rejected

- UBS 1Q profit beats ests. on investment bank

- BP 1Q profit beats analyst estimates on trading

- Deutsche Bank seeks $6.5b as co-CEO Jain reverses course

- AB InBev’s quarterly results miss estimates on Brazil, U.S.

- Heinz holders vote on acquisition by Berkshire, 3G Capital

- Heinz wins ruling tossing investor suits over Berkshire buyout

- Suncor Energy 1Q operating EPS beats est.

- US Airways-AMR in talks on credit cards w/Barclays, Citigroup

- German unemployment climbs in sign economic recovery delayed

- Japan-to-Korea output misses estimates as Taiwan cools

EARNINGS:

- Enterprise Products Partners (EPD) 6am, $0.65

- Aetna (AET) 6am, $1.38

- Starwood Hotels & Resorts Worldwide (HOT) 6am, $0.53

- Huntsman (HUN) 6am, $0.16

- Norbord (NBD CN) 6am, $1.36

- NiSource (NI) 6:30am, $0.71

- CGI Group (GIB/A CN) 6:30am, C$0.49

- Rockwood Holdings (ROC) 6:30am, $0.67

- Harris (HRS) 6:30am, $1.12

- Pitney Bowes (PBI) 6:30am, $0.44

- Cummins (CMI) 6:44am, $1.86

- Legg Mason (LM) 6:59am, $0.20

- Pfizer (PFE) 7am, $0.55

- Thomson Reuters (TRI CN) 7am, $0.32

- Sirius XM Radio (SIRI) 7am, $0.02

- Fidelity National Information Services (FIS) 7am, $0.61

- Cobalt International Energy (CIE) 7am, ($0.14)

- Wisconsin Energy (WEC) 7am, $0.71

- Avon Products (AVP) 7am, $0.14

- TRW Automotive Holdings (TRW) 7am, $1.43

- Xylem (XYL) 7am, $0.27

- Oshkosh (OSK) 7am, $0.86

- MGIC Investment (MTG) 7am, ($0.14)

- Office Depot (ODP) 7am, $0.04

- Marathon Petroleum (MPC) 7:03am, $2.17

- McGraw-Hill (MHP) 7:10am, $0.73

- MeadWestvaco (MWV) 7:15am, $0.24

- NextEra Energy (NEE) 7:30am, $1.02

- Public Service Enterprise Group (PEG) 7:30am, $0.74

- Invesco (IVZ) 7:30am, $0.47

- Tenet Healthcare (THC) 7:30am, $0.30

- Domino’s Pizza (DPZ) 7:30am, $0.55

- Vishay Intertechnology (VSH) 7:30am, $0.11

- Valero Energy (VLO) 7:42am, $0.99

- U.S. Steel (X) 7:45am, ($0.22)

- Affiliated Managers Group (AMG) 7:54am, $2.03

- HCP (HCP) 8am, $0.72

- UDR (UDR) 8am, $0.33

- AGL Resources (GAS) 8am, $1.34

- BOK Financial (BOKF) 8am, $1.18

- Hudson City Bancorp (HCBK) 8am, $0.11

- 3D Systems (DDD) 8am, $0.21

- Arcos Dorados Holdings (ARCO) 8am, $0.06

- Agco (AGCO) 8:15am, $0.88

- Martin Marietta Materials (MLM) 8:15am, ($0.35)

- Ecolab (ECL) 8:20am, $0.59

- Franklin Resources (BEN) 8:30am, $2.49

- Zoetis (ZTS) Pre-mkt, $0.33

- Arthur J Gallagher (AJG) Pre-mkt, $0.24

- Athabasca Oil (ATH CN) Pre-mkt, (C$0.03)

- Edison International (EIX) 4pm, $0.66

- Vertex Pharmaceuticals (VRTX) 4pm, ($0.21)

- Western Union (WU) 4pm, $0.32

- SolarWinds (SWI) 4pm, $0.37

- Regal Entertainment Group (RGC) 4pm, $0.13

- AvalonBay Communities (AVB) 4:01pm, ($0.63)

- Fiserv (FISV) 4:01pm, $1.34

- Canadian Oil Sands (COS CN) 4:01pm, C$0.42

- Amdocs (DOX) 4:01pm, $0.72

- Flextronics International (FLEX) 4:01pm, $0.13

- IAC/InterActiveCorp (IACI) 4:01pm, $0.68

- DreamWorks Animation (DWA) 4:01pm, ($0.03)

- EXCO Resources (XCO) 4:01pm, $0.08

- NCR (NCR) 4:02pm, $0.42

- Oneok Partners (OKS) 4:05pm, $0.58

- Oneok (OKE) 4:05pm, $0.59

- Trimble Navigation (TRMB) 4:05pm, $0.38

- QEP Resources (QEP) 4:05pm, $0.30

- Questar (STR) 4:05pm, $0.43

- Questcor Pharmaceuticals (QCOR) 4:06pm, $0.96

- Verisk Analytics (VRSK) 4:10pm, $0.53

- Genworth Financial (GNW) 4:10pm, $0.28

- Access Midstream Partners (ACMP) 4:15pm, $0.34

- Fortinet (FTNT) 4:15pm, $0.10

- Yamana Gold (YRI CN) 4:20pm, $0.18

- TECO Energy (TE) 4:24pm, $0.17

- FMC (FMC) 4:30pm, $1.07

- Willis Group Holdings PLC (WSH) 4:30pm, $1.31

- Jones Lang LaSalle (JLL) 4:30pm, $0.23

- Genworth MI Canada (MIC CN) 4:31pm, $0.81

- Equity Residential (EQR) 4:55pm, $0.65

- DDR (DDR) 5pm, $0.26

- Boston Properties (BXP) 5:09pm, $1.21

- SM Energy Co (SM) 5:30pm, $0.57

- UGI (UGI) Post-mkt, $1.44

- American Capital (ACAS) Post-mkt, $0.28

- Manitowoc (MTW) Post-mkt, $0.14

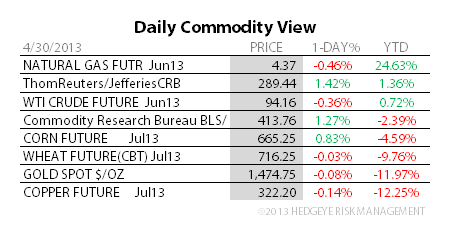

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Rush From Dubai to Turkey Saps Supply as Premiums Jump

- Lumber Mills Expand as Prices Rise Most Since 1993: Commodities

- WTI Crude Heads for Monthly Decline as Stockpiles Seen Rising

- Gold Swings Between Gains and Losses Before Policy Makers Meet

- Copper Heads for Biggest Decline Since May on Demand Concern

- Corn Extends Biggest Gain Since June as Rain Slows U.S. Planting

- Sugar Climbs With Grains Before May Futures Expiry; Cocoa Falls

- Perth Mint Works Through Weekend to Meet Most Demand Since 2008

- Noble Group Said to Hire Former Goldman Trader Evans for Metals

- India May Consider Cutting Wheat Export Price to Boost Shipments

- Greeks Bet Ship Rout Ending With Most Orders Since 2008: Freight

- Voestalpine Sees Steel Recovery Taking Until 2014 on Europe Glut

- Crude Stockpiles Gain in Survey as Output Climbs: Energy Markets

- Gold Exchange-Traded Products Poised for Record Monthly Decline

CURRENCIES

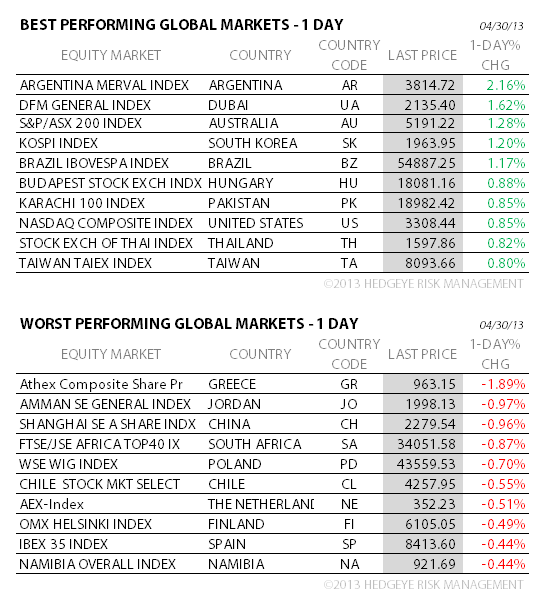

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team