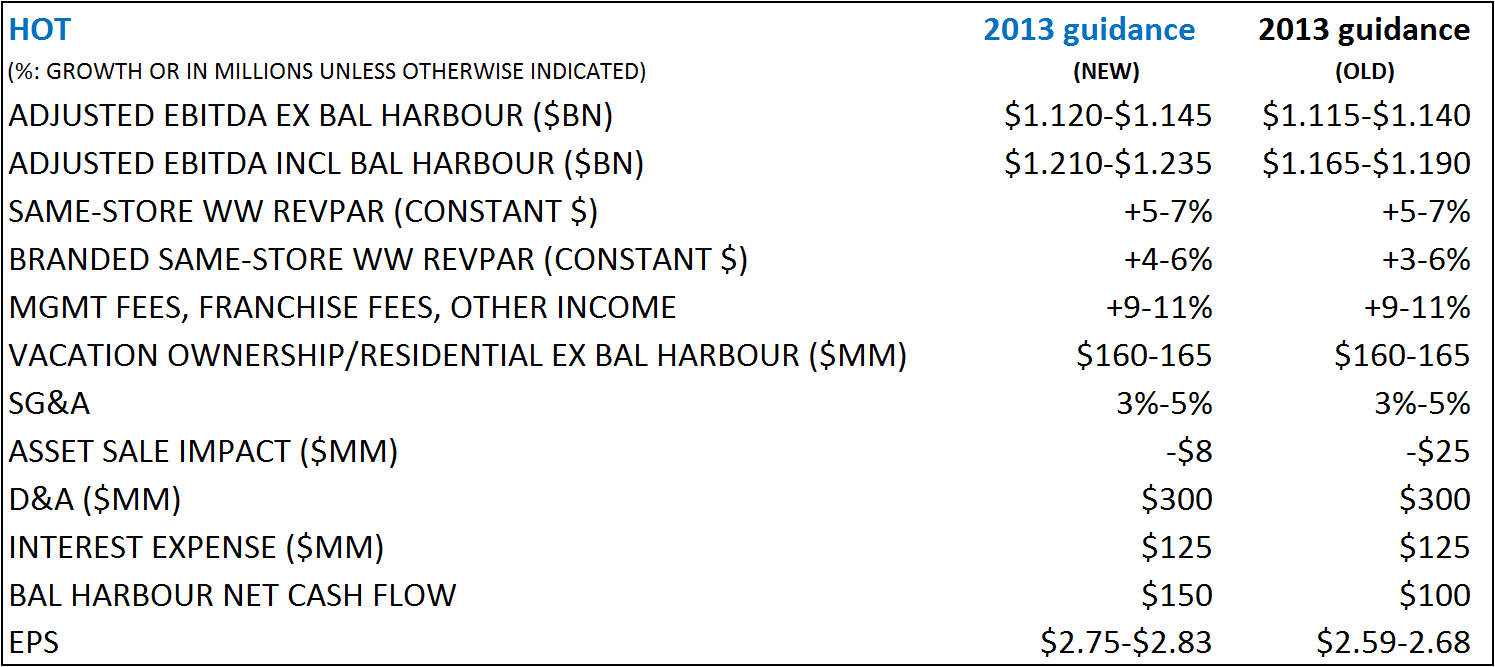

Solid quarter and higher guidance. We still think the numbers are conservative

"Overall, the global lodging recovery continues along the trend lines we’ve been seeing. Tight supply is driving higher room rates in North America, and our footprint continues to expand in the growing economies. We are seeing more interest among real estate buyers for both vacation ownership and our owned hotels"

- Frits van Paasschen, CEO

CONF CALL NOTES

- Business is doing better than they expected across the board

- They expect to complete the sell-out of BH this year. Only 40 units left.

- In China business is generally picking up, 1Q RevPAR was up over 5%. Results were soft in Beijing as it was more dependent on government business. The government transition is not complete until March. Meanwhile, across markets in the south, RevPAR was up nearly 10%. The quarter's trends were in-line with the long-term trend HOT sees in China

- Revenue grew by nearly 6% elsewhere in Asia. India was slower, Indonesia, Thailand and Malaysia were strong. Smart capital in India is moving to convert their brands.

- 1Q European RevPAR was flat, ex London. Weak start in London, suggesting oversupply post Olympics. Q1 is the off-season in Europe so its hard to draw conclusions for the full year based on these results.

- Argentina mess is spilling into Uruguay

- North America RevPAR was up 6% and ex Canada up 7%

- Government travel is about 2% of their business so the sequester is less of drag on their business

- Africa & the ME - RevPAR up over 7%. Business there is good.

-

After their time in China, they increased occupancy by 6 percentage points in 2012 alone. HOT doubled the number of SPG active members and SPG now accounts for 55% of our occupancy. They grew outbound travel from China to their hotels globally by 52%. And since the relocation, they've signed 54 deals, meaning our pace of signings is up by about 40%. And 45 hotels have opened.

- Hope to derive 80% of their profits from fees by 2016 by selling more assets

- Will not reduce debt further and will use FCF to invest in high ROI investments and the balance will be returned to shareholders in the form of buybacks and dividends.

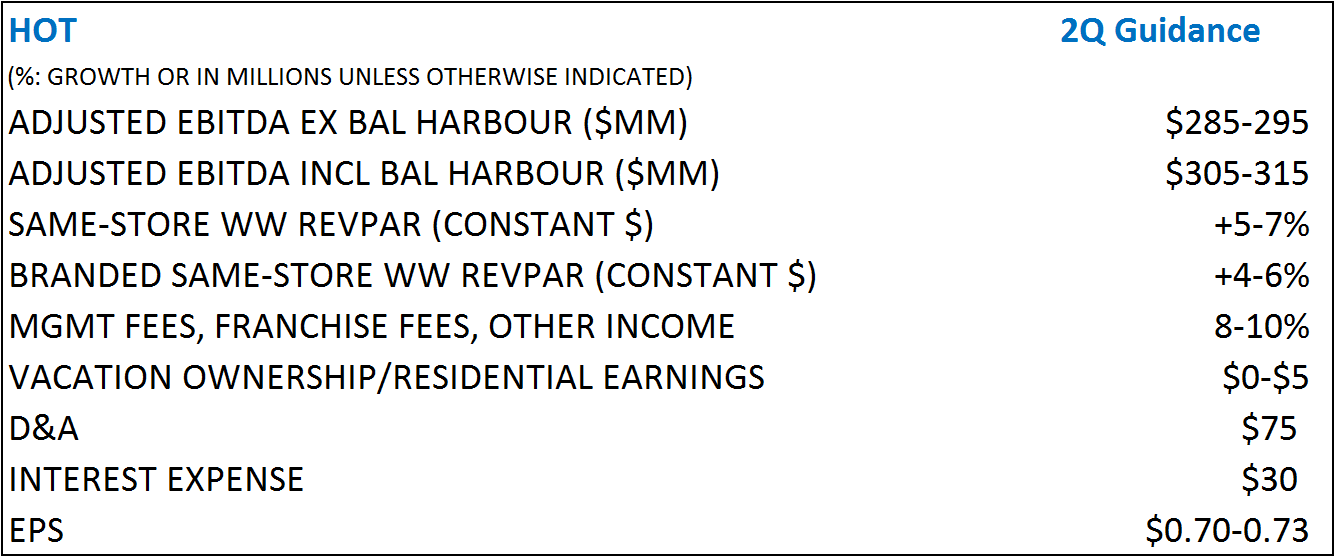

- Transient rate was up over 5% in the quarter. Hawaii was particulary strong, N.E was weaker. Expect that NA will come in at the high end of their guidance range.

- Group pace continues to pace along in the mid single digits. NA will remain their strongest region in 2013.

- Expect modest RevPAR growth in Europe in 2Q. Companies are watching their costs, groups are smaller and bookings are closer in. No signs that things are improving right now.

- China: As expected they saw business pick up in Q1. RevPAR increased 5.4% in 1Q in constant currency. New government has been asking officials to reign in their spending and lifestyles. Harder hit are the north and western regions. Some impact from bird flu in the Shanghai region. They are monitoring the situation closely. Believe that new supply will be absorbed in the next 9-12 months. Expect China to be at the midpoint of their 5-7% guidance.

- They will begin to break out greater China in their releases going forward

- Impact on travel into Japan from North and South Korea issues

- India remains sluggish but sequentially better

- A&ME was the fastest growing region in 1Q. UEA is booming with RevPAR growth of 14%. Egypt was up 30% in the Q. Expect these trends to conitnue in 2Q.

- Latin America was dragged down by Argentina which was down 27%. Argentina accounts from 15% of owned RevPAR. Mexico was up 10% as US guests return. Expect LA growth to remain challenged in 2Q.

- Owned portfolio: Impacted by Argentina. US owned hotels and in particulary Bal Harbor results were very strong. YTD they have sold an additional 4 hotels which will reduce earnings by $8MM from guidance given in 4Q.

- VOI: trends remain stable. Resort business was up sharply. Cash flow from this business remain strong.

- Adding inventory in Orlando

- Bal Harbour significantly exceeded their expectations.

- SG&A was down YoY, reduced costs due to restructuring and easy comps. Some of the severance costs and other costs were delayed this year. They incurred $4MM of severance so far vs. prior guidance of $10MM

- Japan headwinds impacted FX

Q&A

- Were buyers earlier in the Q when the stock was under $60. They are opportunistic buyers of their stock.

- Why did HOT's RevPAR in China materially outperform Smith travel numbers in China?

- Geographic mix and they generally outperform the index with their brand. Mix of new hotels also helps.

- Overall M&A environment: It's still a lumpy market on the UUP and Luxury asset side. Qualitatively, there is more interest than 12 months ago. Sense is that volume should continue to pick up. They are still not seeing an active market for large portfolio sales (> $1BN), still a ones and two's market.

- They do have the ability to sell most of their European assets and distribute that cash efficiently to shareholders. They have no cash trapped in Europe now. They should have no issues repatriating cash from asset sales.

- Can structure sales as either asset sales or stock sales

- VOI: By having scaled back their business they have very favorable IRR's that nicely exceed WACC. Happy to keep the business in their portfolio given the cash flow generation and the syngeries. For example, they are moving the Westin St John's into VOI. More efficient than an asset sale

- They have worked on their assets to make them ready for sale. In theory, they can achieve their asset sale targets before 2016 but it just depends

- Regarding their buyback activity, look to past behavior as an indicator of future activity

- US is better than they expected RevPAR wise. Trending at high end or netter in 2Q bc of holiday shift. China is a little softer. Europe is really unchanged - still projecting 2-3% growth since 1Q doesn't really matter.

- Any impact from air traffic furlough from last week. Think its was brief enough that they did not see an impact

- Incentive fees: 60% of SS mgmt properties are paying incentive and about 75% outside the US. In the US, it's in the 30% range.

- Outside of group business, their visibility is somewhat limited

- Have some modest FX headwinds from Japan and Canadian and AU impact is also negative... all in to the tune of $3-4MM. They may also have some more severance charges. SG&A is also fairly lumpy.

- In some cases they have a preferred time to sell due to tax issues or the need for renovations

- Group Pace: low to mid single digit pace - same as before

HIGHLIGHTS FROM THE RELEASE

- Adjusted EBITDA was $315 million, which included $58 million of EBITDA from the St. Regis Bal Harbour residential project

- Worldwide Systemwide REVPAR for Same-Store Hotels increased 5.0% in constant dollars (4.6%

in actual dollars).... Systemwide REVPAR for Same-Store Hotels in North America increased 6.2% in constant dollars (6.2% in actual dollars). - In 1Q13, HOT "signed 26 hotel management and franchise contracts, representing approximately 6,200 rooms, and opened 18 hotels and resorts with approximately 4,000 rooms"

- 20 are new builds and 6 are conversions from other brands.

- At March 31, 2013, the Company had approximately 400 hotels in the active pipeline (~100,000 rooms)

- Special items... totaled a charge of $5 million (after-tax), included a loss of $8 million (pre-tax), primarily related to the sale of three wholly-owned hotels.

- Excluding special items, the effective income tax rate in the first quarter of 2013 was 31.3%

- Net income... included a tax benefit of $70 million, in discontinued operations, as a result of the reversal of a reserve associated with an uncertain tax position related to a previous disposition. The applicable statute of limitation for this tax position lapsed during the first quarter of 2013.

- During the first quarter of 2013, 18 new hotels and resorts (representing approximately 4,000 rooms)

entered the system.... five properties (representing approximately 900 rooms) were removed from the system. - Excluding owned hotels in Argentina, REVPAR at Worldwide Owned Hotels increased 5.3% in constant dollars (4.9% in actual dollars). Excluding owned hotels in Argentina, internationally, REVPAR at owned hotels increased 4.2% in constant dollars (3.7% in actual dollars). REVPAR at owned hotels in Argentina decreased approximately 27% in constant dollars driven by economic instability in the country. Excluding owned hotels in Argentina, margins increased by approximately 100 basis points.

- Total vacation ownership revenues increased... primarily due to increased revenues from resort operations, the transfer of the Westin St. John from owned hotel revenues to vacation ownership revenues, and a favorable adjustment to loan loss reserves.

- Originated contract sales of vacation ownership intervals and the number of contracts signed were flat... The average price per vacation ownership unit sold increased 0.5% to approximately $16,200, driven by inventory mix.

- HOT's residential revenues were $132 million.... realized residential revenues from Bal Harbour of $129 million and generated EBITDA of $58 million. During the first quarter of 2013, the Company closed sales of 38 units at Bal Harbour and realized incremental cash proceeds of $127 million associated with these units. From project inception through March 31, 2013, the Company has closed contracts on approximately 86% of the total residential units available at Bal Harbour and realized residential revenue of $939 million and EBITDA of $219 million.

- SG&A decreased ... primarily due to organizational changes in the second half of 2012 and non-recurring professional expenses recorded in the prior year. The Company continues to target a 3-5% increase for the full year.

During the first quarter of 2013, the Company completed certain changes to its organizational structures

in the Americas division. The Company recorded an expense for severance costs of approximately $4

million associated with these changes. - Gross capital spending during the quarter included approximately $17 million of maintenance capital and

$81 million of development capital - During 1Q13, HOT completed the sales of three hotels; the Aloft and Element hotels in Lexington, Massachusetts and the W New Orleans - French Quarter for cash proceeds of approximately $61MM. These hotels were sold subject to either long-term management or franchise contracts. The Company recorded a loss of $8MM associated with these sales. In addition, following the end of the first quarter the Company completed the sale of the W New Orleans for cash proceeds of approximately $65MM.

- In 1Q13 and through April 5, 2013, HOT repurchased nearly 1MM shares at a total cost of ~$56MM and a weighted average price of $59.35 per share. As of April 5, 2013, approximately $624MM remained available under the Company’s share repurchase authorization

- At March 31, 2013, HOT had gross debt of $1.275 billion, cash and cash equivalents of $529 million (including $142 million of restricted cash)... including $472 million of debt and $20 million of restricted cash associated with securitized vacation ownership notes receivable, was $1.198 billion.