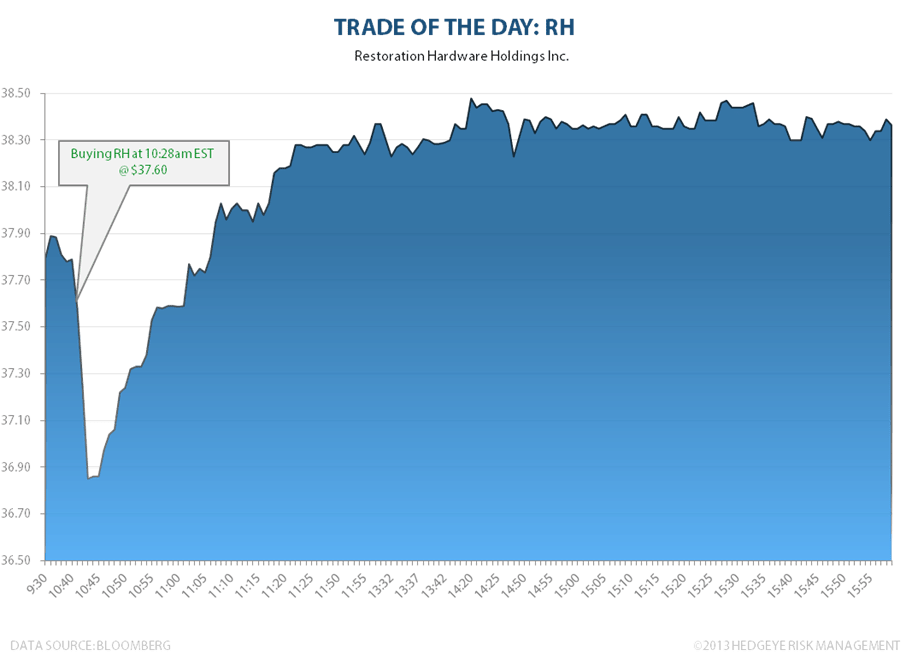

Today we bought Restoration Hardware (RH) at $37.60 a share at 10:28 AM EDT in our Real-Time Alerts. Nice pullback (on no volume) to immediate-term TRADE support here for Hedgeye Retail Sector Head Brian McGough to hit the buy button on. Shorts are going to keep getting squeezed here is our call. Fundamentals are solid.