This note was originally published April 26, 2013 at 10:39 in Restaurants

Starbucks (SBUX) is the best-run company that we follow and the long-term TAIL seems unlimited. The company’s geographical reach and size is highly impressive. Even more impressive is the performance of the Americas business, given its size and maturity.

We maintain a positive view of Starbucks as an effective way to play improving US consumption. While sell-side analysts this morning are correct that the global macro outlook is challenging, it is important to know where SBUX has its exposure. The U.S. is what will drive beats and misses in the near term, despite much unit growth being focused in China/Asia-Pacific. ~88% of company stores and ~85% of licensed stores within the "Americas" division are located in the United States.

The Good

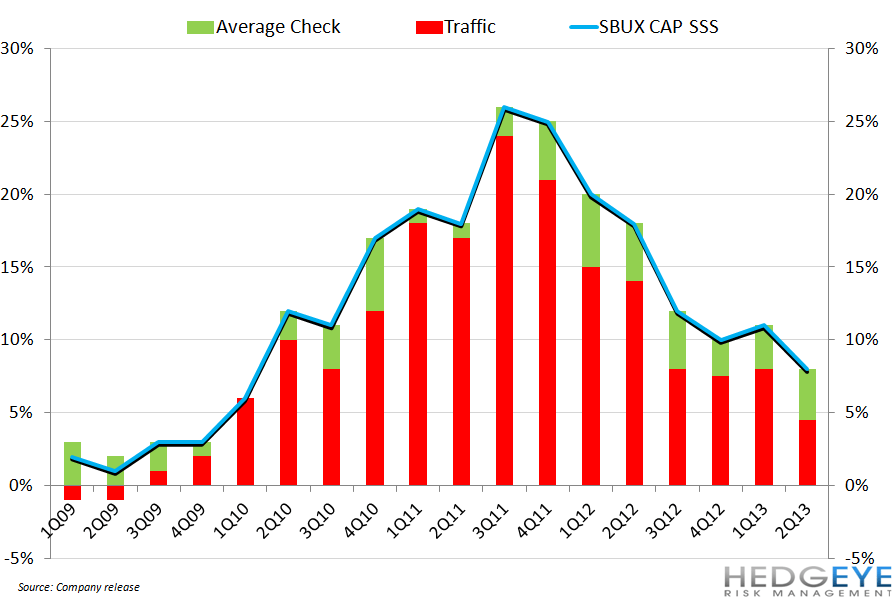

Last night, Starbucks reported global same-store sales growth of 6% (13th consecutive quarter above 5%). Same-stores sales in the Americas division grew 6% (including 5% traffic). Total revenue growth of 11% produced a 1.8% increase in operating margin and a 20% increase in earnings per share (EPS).

Americas:

- Revenues + 10% year-over-year

- SRS two-year comp sequentially declined 1%

- Operating Income +22%

- Operating Margin +2.2% to 21.1% (highest 2Q ever)

EMEA:

- Revenues unchanged, operating margin unchanged

- -2% second quarter of fiscal year 2013 comps implies 2-year comps negative

- Emphasis is on improving profitability by refranchising (“sold to you!”)

- Applying Americas “learnings” not trumping macro

CAP:

- Revenues grew 22%

- Comps at +8% came in light vs consensus

- Operating margin down -7.1% on investment spending on China growth

The Less-Good: Expectations, Food

The only slight negative stemming from what was, overall, a bullish conference call was management reigning in expectations for 2H13, but upping the official guidance. During the call management guided for third quarter fiscal year 2013 EPS of $0.50-0.53 and fourth quarter fiscal year 2013 EPS of $0.54-0.57, versus consensus of $0.54 and $0.57, respectively. The coffee cost tailwinds should continue well into fiscal year 2015 now, offsetting continued investments in growth-related initiatives.

Food remains Starbucks’ Achilles’ heel. The acquisition of La Boulange is a long way from being branded a “success”. As of yesterday, there were 439 stores carrying La Boulange products, including all stores in the San Francisco Bay Area. The company is planning a rollout of La Boulange pastries in the Pacific Northwest including Seattle in June, then will expand to cities including Los Angeles and Chicago, followed later in the year by New York and Boston. The company is on track to have La Boulange products in all of our U.S. company operated stores by the end of 2014.