“The problem with the future is that it isn’t as clear as the past.”

-John Lewis Gaddis

On a flight to Denver yesterday I had the opportunity to dig into John Lewis Gaddis’ most recent history book, George F. Kennan. Gaddis, professor of Military and Naval History at Yale, won the Pulitzer Prize for Biography with this book last year.

Kennan’s life is obviously a fascinating one, and I’ll draw on some of his Russian thoughts in upcoming Early Looks, but what I found most interesting was the deep simplicity of Gaddis’ process in writing about history. Empathy is a primary focus.

“The writing of biography particularly requires empathy, which is not the same as sympathy. It asks a very simple question: What exactly would I, knowing what they knew then, have done differently?” (pg 146).

Back to the Global Macro Grind…

Last week I geeked out with some Chaos Theory in order to attempt to explain what it is that I do. In many ways, my Early Look “Context Matters” draws, partly, on the process that Gaddis explains. Research and Risk Factors are my content and time is my context.

If my contextualization of time doesn’t have empathy, can it be considered objective? Of course not. That’s why Predicting The Past in markets and economies isn’t as trivial as it sounds. There are often two competing sides to the story.

One side of market history that doesn’t require qualification is the score. What a market price did and when is a fact. You may not like the facts, but that certainly doesn’t mean they cease to exist. For the last 5 months, the US Dollar and US Stocks are up; Commodities down.

Moreover, from a historical GDP reporting perspective:

- Q1 2013 US GDP #GrowthAccelerated to +2.50% (versus +0.38% in Q412)

- Q1 2013 US Consumer Services #GrowthAccelerated to +1.46% (versus +0.27% in Q412)

- Q1 2013 Export #GrowthAccelerated to +0.4% (versus -0.4% in Q412)

Dollar Up = Exports Up? Qu’est ce que c’est mes amis? Oui oui, c’est l’economie, eh!

I can write that in the French tongue of Charles de Gaulle (who thought devaluing the French Franc was the best path to economic prosperity). I can translate it into Krugman/Bernanke if you’d like too. But facts don’t lie; economists and politicians do – and a strong currency has always been good for consumers in the United States of America.

I know. KM, that is so Q1 – this is Q2, and what have you done for me lately?

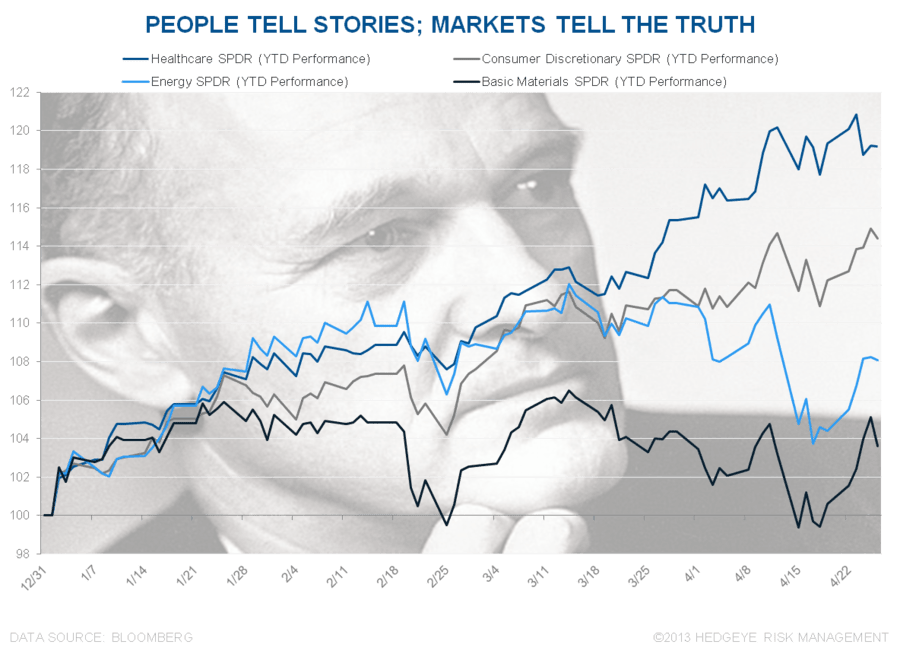

Well, so far, the US stock market has scored the 1st month of Q213 (April) as follows:

- SP500 +0.83%

- US Healthcare Stocks (XLV) +3.3%

- US Consumer Discretionary Stocks (XLY) +2.8%

- US Basic Materials Stocks (XLB) -0.70%

- US Energy Stocks (XLE) -2.7%

Looks like the performance divergence between Consumption (XLV, XLY) and Commodities (XLB, XLE) is widening. And with Brent Oil failing at $104.09 resistance again this morning, that is a very good thing (for Consumers).

Inclusive of last week’s dead cat bounce from oversold lows, YTD Commodities performance has not been pretty:

- CRB Commodities Index -3.3% (versus SP500 +10.9%)

- Oil (Brent) -4.6%

- Corn -11.1%

- Gold -13.3%

- Copper -13.3%

While some continue to plead that Commodities crashing is a bearish “internal indicator” for economic demand, I can’t for the life of me find that chapter in either 1983-89 or 1 US economic or stock market history.

That said, I am empathetic to their plight.

Plight (defined): “a situation, especially a bad or unfortunate one.” (thefreedictionary.com)

To be crystal clear on this, this week I fully expect both Ben Bernanke (Fed) and Mario Draghi (ECB) to continue with their storytelling plight that the world needs to devalue. The FOMC will descend from the high mountain of central planning on Wednesday. Then it’s the ECB’s turn on Thursday. As we’ve been saying for the last few weeks, the probability of the ECB cutting rates is going up, not down.

So what if that happens? What if the ECB either cuts rates or alludes to cutting rates? Since it’s all about expectations, market history has already answered part of that for you. The EuroStoxx600 outperformed all major regional indices last week, closing +3.7% - and it’s seeing some follow through buying/covering again this morning.

If the Europeans cut rates, that’s bad for the Euro – good for the US Dollar – bad for Commodities - and good for US Consumers. Bernanke disagrees with me on that. Unfortunately, history doesn’t side with his version of the story. Neither does the US stock market or her economy. Ben, empathize with economic gravity – and please, get out of the way. Devaluing the Dollar again would be a disaster.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, EUR/USD, USD/YEN, UST 10yr Yield, VIX, Russell2000, and the SP500 are now $1, $97.18-104.09, $82.04-83.32, $1.29-1.31, 97.21-100.92, 1.66-1.76%, 11.77-14.63, 928-955, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer