Conclusion: Our bearish call on CRI is one that – especially today – has not gone our way. Let’s put on the accountability pants and see how the research call is changing – especially relative to a stock price that wants to do nothing but go up. We think that the bull/bear on this one is pretty well balanced – with a positive secular backdrop, but risky near-term positioning (and spending) to hit sales and margin targets that are already widely telegraphed. The +6% reaction showed that the market was looking for the negative momentum from last quarter to continue. We did too. Didn’t happen. When we shake the Etch-a-Sketch clean and re-evaluating our position, we still come away with more risk than reward.

(Updated to include the correct e-commerce growth figures)

Here’s our take on the bull vs. bear research call:

Bull:

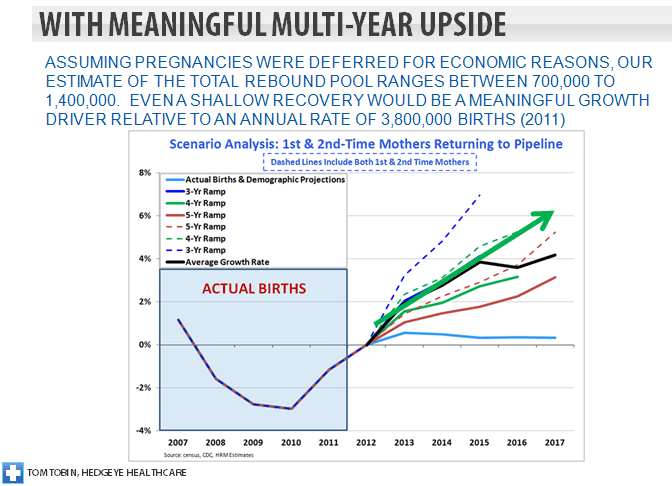

- Relatively high-return, defendable brand with dominant share (24%) in its core Baby business that will capitalize on a rebound in the birth rate after a 5-year buildup in the deferred birth pipeline (see Exhibits below).

- The company is investing today in a) e-commerce fulfillment, b) more company-operated stores (including outlets), c) centralizing headquarters, d) converting Canadian Operations to higher-margin dual-brand stores, and e) taking its sourcing operations back in-house – all of which should take margins to 14-15%. While we have a hard time internalizing the concept of a business with these characteristics sustaining this type of margin level, there’s arguably no reason why it can not get close temporarily if it wants to.

- This suggests EPS in the $4.50-$5.00 range, or a 15%+ CAGR from current levels.

- Cash flow might be bad today, but capex will ease as they start to harvest the benefit of their spending, leading to far better FCF characteristics in 2014/2015. That’s precisely when the ‘birth boom’ should be in full swing. CRI should have the sourcing and fulfillment assets in place at that point to capitalize on the favorable operating environment with a lower cost structure.

Bear:

- CRI might have dominant share in the Baby business, but that only accounts for 32% of CRI’s total. After backing out parts of its sleepwear business that we’d also consider equally as defendable, we’re looking at about 50-60%% of the portfolio has a competitive set that is no stranger to price competition and not as dependent on the birth rate.

- Like for like sales in its portfolio are simply not good. CRI added $39mm in aggregate sales in the latest quarter, but $17mm-$18mm of that was in e-commerce alone. In addition, it added 14% more stores vs last year in Carters USA, which accounts for 29% of revenue. We don’t want to ding the company for good performance in e-commerce, as it’s a critical part of growth. But with this store growth should we really be surprised that comps were up only 0.6% in Carters, down 0.5% in wholesale, and DOWN 9.5% at Osh Kosh? Not really. We’d rather the company focus on the productivity of its existing assets.

- Gymboree just reported comps of -2% for it’s latest quarter (on a 2 month lag to CRI). If this ‘baby boom’ is materializing, we’re not seeing it yet in numbers. What’s interesting is that year-to date, we’ve seen a notable rebound in containerized traffic for Baby Apparel – about $3bn in retail value vs $1.9bn last year based on our math. Some of this is due to catch-up volume from last year’s port strike, but we think at least half represents real incremental shipments. Either this sales boost has yet to be realized by the major brands, or more competition is being attracted to the space – something that tends to happen when cyclical/secular trends turn positive in virtually any industry.

- CRI’s inventories look fine – not good, not bad, just fine. The SIGMA chart shows that it’s going on its fifth quarter of improvement at a time when margin comparisons are getting more difficult. We almost never see multiples expand when this is the case. The punchline here is that the company needs to drive future stock performance by earnings upside. To its credit, that’s what it’s been doing, and our sense is that it simply set conservative expectations for the year today. But for a company that chalked up $0.08-$0.10 of a $0.10 beat to deferred SG&A and shipment timing (ie did not really beat), we’ve got to think that the Street is looking through the company’s ‘guide and beat’ strategy at least to a certain degree.

- Its' capital spending projects seem to be going according to plan, and we like the fact that more people transferred to Atlanta than the company previously thought. That suggests better continuity and more faith by the team internally in what the management team is doing. But we still can’t gloss over the fact that the sheer level of spending at this company is off the charts. Capex is going up from $83mm to $200mm this year – and we definitely are cautious towards that. SG&A growing by over 2x the rate of sales hardly puts us in our happy place. either. Not because the company should't be spending, but simply because its risky having so many balls in the air at once, and its causing free cash flow to evaporate. We’re modeling cash flow to erode from $195mm in 2012 to $30mm this year, and we don’t this we’ll see a rebound to ’12 levels until 2015.

THE BULL CASE ON AN INFLECTION IN BIRTHS

Here’s Hedgeye Healthcare Team’s overview on their expected increase in the birth rate. Contact or Tom Tobin () for additional color.