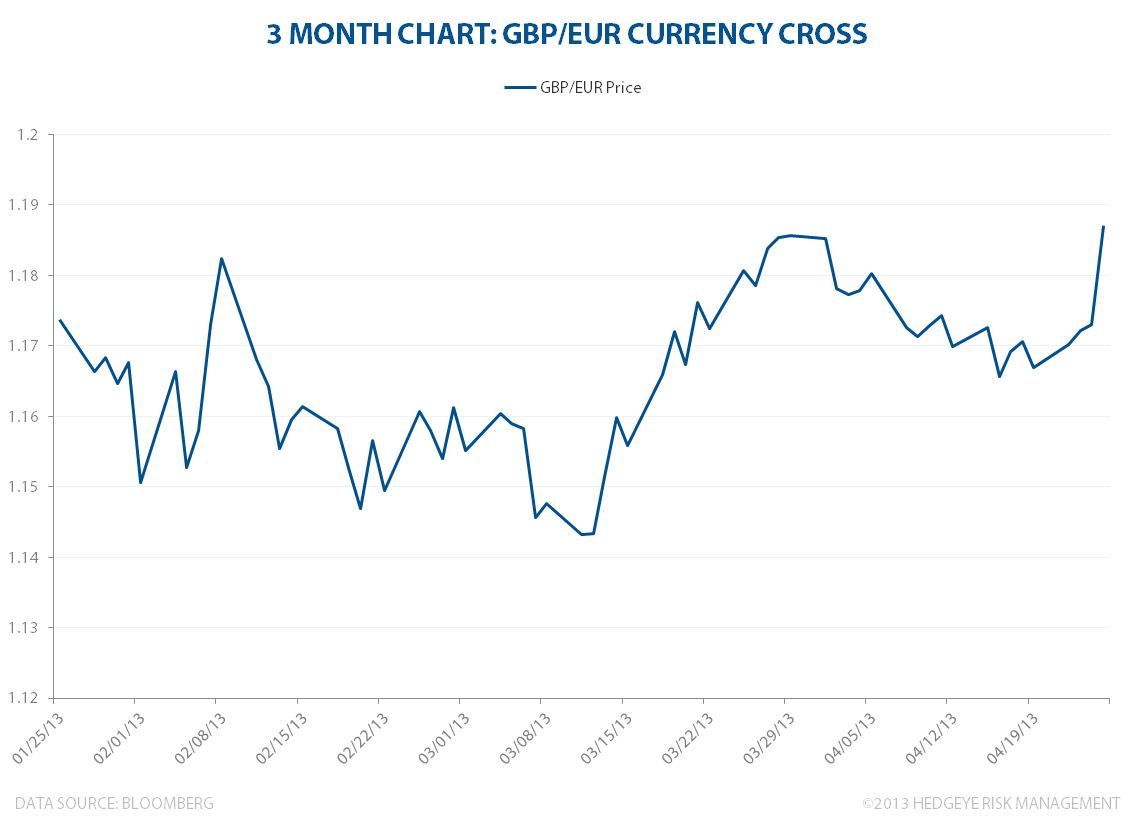

The British Pound rallied today after reports from the U.K. Office for National Statistics showed the economy expanded by 0.3% in the first quarter, exceeding expectations of a 0.1%. Against the Euro, the Pound gained considerably, which is outlined in the GBP/EUR currency cross chart below. While the growth isn't spectacular, it's a heck of a lot better than the situation in Spain and elsewhere across Europe.