Strong quarter, unchanged guidance and some reassuring comments are boosting the stock today. Should we be optimistic about the market of just market share gains from CCL?

"It was a gratifying first quarter...Ticket revenues were better than expected, costs were well controlled and it was encouraging to see record guest satisfaction and noticeable improvements in onboard spending as a result of our revitalization efforts"

- Richard D. Fain, chairman and chief executive officer

CONF CALL NOTES

- Expect that Quantum of the Seas will generate compelling returns for the company

- Expect to invest their savings on marketing throughout the rest of the year

- Think that some of the slowdown in Caribbean booking in March was due to the negative publicity about the industry but see some of that easing and still expect strong yields this year

- They are seeing positive developments with the booking window widening about 2 weeks from 2011 and 2012. Prices, on average, are running 3% ahead of next year.

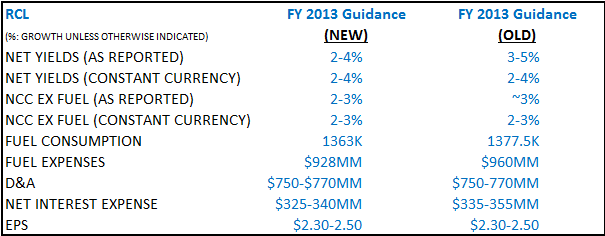

- As-reported yield guidance lowered by 100bps due to stronger $

- Favorable fuel prices and lower consumption are offsetting the negative effects of the stronger U.S. dollar.

- They have put on some more fuel hedges recently

- Sense that their current distribution of inventory across regions is a good one

- Australia rapid capacity growth has depressed yields but the market remains healthy

Q&A

- How much of the strength that they are seeing are coming from share gains from CCL?

- No comment

- Looks like the main markets in Europe are booking at a pace that has somehow derisked their outlook for the balance of the season.

- Before the bad press, they were doing better (in the Caribbean). They are back in "equilibrium" now but not running as strong.

- They have not seen a mix shift between first time cruisers and repeat cruisers from the recent publicity. However, bad publicity does usually impact first time cruisers more than repeat cruisers.

- Had about 8 cents of favorability of costs in the quarter mostly due to marketing timing. They do expect to reinvest that money throughout the year- some of which will be spent in 2Q. They did save 2 cents from FX which should drop to the bottom line.

- When they gave their guidance in Feb, they factored in easier comps in Europe. That's why they expect to have positive comps in Europe this summer. They are around 70% booked for Europe for the year. Back in Feb they were only 50% booked.

- They have reviewed their systems in light of the recent events and feel like their current capex plan properly covers the maintenance of their ships

- Europe as a whole is doing better than they expected. Spain followed by the UK are the 2 weakest markets. Germany has held up better than expected, especially with the TUI brand

- Booking window: Across their portfolio, they have seen an across the board expansion of the booking curve by 2 weeks or so. Most of the ships that have had renovations have done the best.

- Australia market has been an exceptionally strong market during the past few years. As a result, they have had a lot of capacity additions to that market. They have lowered their yield expectations for that market.

- Why are they lowering deployment for Europe if things are picking up? It's not that the market is "strong"; it's that their initial expectations were too low.

- Within Europe, there is more business coming from Northern Europe than Southern Europe

- Carnival is saying that Europe is getting a little bit worse.. .RCL is saying its getting better? Their view on Europe is really "on the margin" it is slightly better than what they saw in Feb. They are happy that they took 10% capacity out of Europe and are still contemplating taking out 10% more capacity out of Europe in 2014 in hopes of getting better yields. (already in new press release)

HIGHLIGHTS FROM THE RELEASE

- Overall, demand trends appear consistent with the company's earlier expectations. Constant-Currency Net Yield and EPS guidance for the year remain unchanged at this time.

- Both onboard revenue and ticket pricing improved... NCC excluding fuel were also better than anticipated, primarily due to timing

- Since the beginning of the year booking volumes have averaged 5% ahead of the prior year. At this time, full year booked load factors and APDs are higher than the same time last year. The overall demand environment is in-line with the company's expectations from February, but as usual there are regional fluctuations.

- Bookings from North America have remained strong since the beginning of the year, with the exception of a modest disruption to Caribbean demand which the company attributes to adverse industry media coverage.

- Demand from European sourced guests strengthened in early February and the company expects pricing improvement from the region for the year.

- Demand from China has weakened somewhat due to itinerary changes related to the territorial dispute with Japan.

- RCL expects that the negative effects from the adverse industry media coverage in March and itinerary changes in Asia will be offset by the favorable performance in the first quarter and a slightly better outlook for Europe. As a result, full year 2013 Constant-Currency yield expectations remain unchanged from the company's February guidance of an increase of 2% to 4%.

- RCL recently opened the majority of its 2014 deployment offerings and announced a two-month European summer micro-season for the Oasis of the Seas that complements the vessel's scheduled maintenance drydock in Rotterdam. Demand for these sailings has been exceptionally strong.

- RCL expects to further reduce its European deployment year-over-year by another 10% and also expects that European itineraries will be approximately 25% of its overall 2014 capacity.

- As of March 31, 2013, liquidity was $2.2 billion.

- Scheduled debt maturities for 2013, 2014, 2015 and 2016 are $1.5 billion, $1.5 billion, $1.1 billion and $1.0 billion, respectively.

- The company will continue to opportunistically approach the prepayment and refinancing of its 2013 and 2014 scheduled maturities.

- Projected capital expenditures for 2013, 2014, 2015 and 2016 are $700 million, $1.2 billion, $1.2 billion and $1.3 billion, respectively.

- Capacity increases for 2013, 2014, 2015 and 2016 are 1.3%, 1.0%, 6.9% and 4.8%, respectively. The company's annualized capacity growth rate from 2012 to 2016 remains at a historically low rate of 3.5%