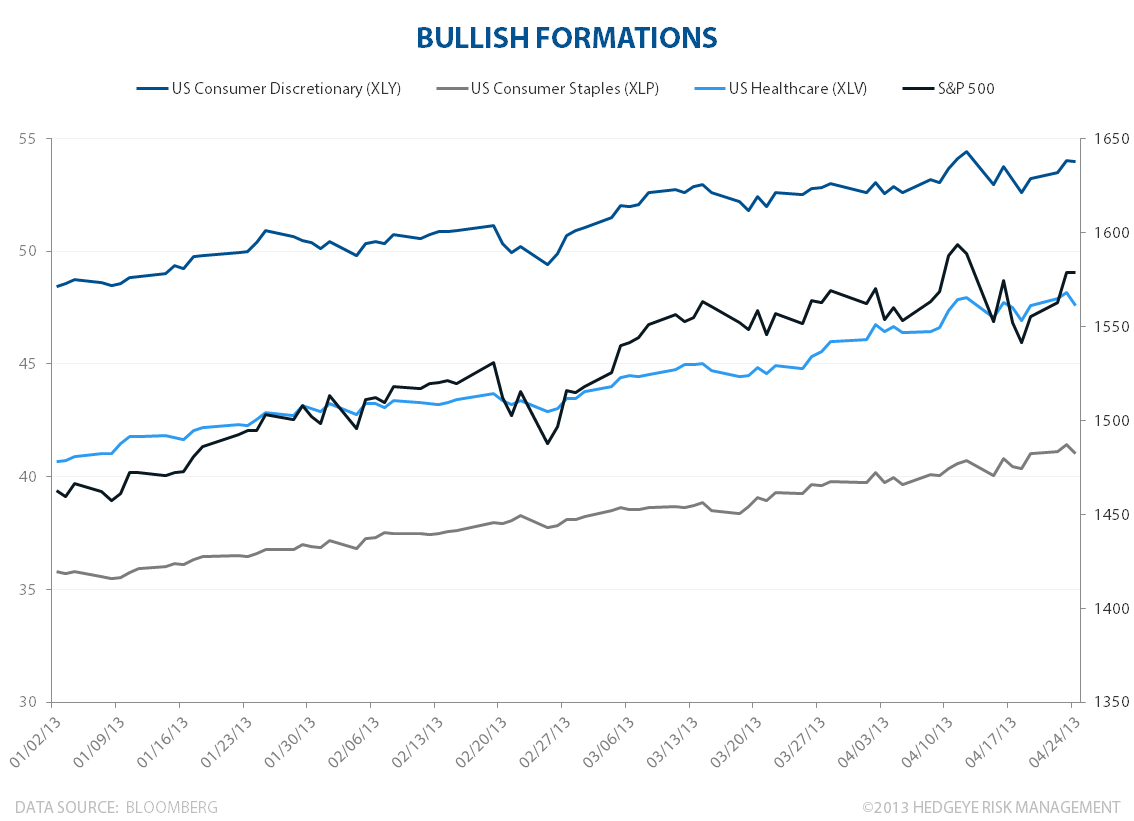

Right now, several sectors are in bullish formation across all three of our durations: TRADE, TREND, and TAIL. They include US Consumer Discretionary (XLY), US Consumer Staples (XLP), US Healthcare (XLV) and the S&P 500. As you can see in the chart below, year-to-date performance has been outstanding thus far for 2013. Here's the scorecard as far as the aforementioned sectors go:

- S&P 500 (SPY): +10.8% YTD

- Consumer Discretionary (XLY): +13.7%

- Consumer Staples (XLP): +17.3%

- Healthcare (XLV): +19.4%