This note was originally published at 8am on April 10, 2013 for Hedgeye subscribers.

“We are made of the same stuff of which events are made.”

-Ralph Waldo Emerson

That’s the opening volley from astrophysicist Eric Chaisson in one of my favorite risk management books, Cosmic Evolution. What’s up with that? What’s up with a chaos theorist prefacing his ideas with the penmanship of a mid-19th century American essayist? It’s all about the storytelling folks. As Taleb recently wrote in Antifragile, “evolution does not depend on narratives, humans do.”

While finding the deep simplicity of the Global Macro point that matters can often feel like finding Waldo himself, Chaisson channeling Emerson is consistent with our discipline of Embracing Uncertainty. Emerson was labeled as a “transcendalist” – he preached individualism and self reliance; he did not support dogmatic and/or traditional organizations.

We’re human, so we want things about markets to make simple sense within our organizational boxes. But markets change, fast and slow. Sometimes they make sense. Sometimes they don’t. In the heat of a thermodynamic moment, does every phase change make sense to everyone? Does that change care if you understand it? Of course not. Best we can do is try to keep up.

Back to the Global Macro Grind…

Keeping up with the US stock market hasn’t been easy for the #PTCs (professional top callers). Every time the SP500 sells off to a higher-low (1540 on Friday), they claim victory. Every time we rally off those higher-lows to higher all-time highs, I hear crickets.

Crickets? What are crickets? Do you hear them on the floor of the NYSE? Crickets – you can hear the hum when something was supposed to happen, and didn’t. #crickets

While I am not entirely sure what kind of a risk management process top-calling is, it fits within the confirmation biases of consensus. My tally is up to 28 high profile PMs, strategists, pundits, etc. who are currently still trying to call the top in US stocks. Maybe this time is different – maybe they’ll all nail it, at the same time. Maybe not.

Quantifying sentiment in markets is probably the hardest thing to do – I’ve tested and trialed almost every voodoo signal I have been issued on this front, and I am left with very few that I’d actually act on. Let’s consider those few:

1. Sentiment Spread – the II Bullish/Bearish survey data doesn’t tell me much on most metrics other than its historical spread (ie Bulls minus Bears). This morning, that spread is +2990 basis points wide. Over a decade of my tabulating/monitoring this spread, a relatively safe sell zone is +3500-3700 basis points wide. A relatively safe buy zone is 900-1500 basis points wide.

2. Exhaustion (VIX vs SPX) – while plenty will quibble with this for theoretical reasons (“front month doesn’t reflect sentiment” … “term structure matters more”, etc. etc.), for me it’s just a signal that I’ve built for myself that works most of the time. The problem with it is that it’s not signaling all of the time. So I have to wait on it.

If you’ve studied thermodynamics, you’ll agree that waiting for a certain amount of entropy matters before you register a certain amount of consequential change (energy). That’s one way to conceptualize my VIX/SPX signal. What I am waiting on is:

A) SPX immediate-term TRADE oversold

B) VIX immediate-term TRADE overbought

Sounds simple, because it is – after you’ve incorporated multiple-factors across multiple-durations in order to contextualize that immediate-term moment. In other words, it’s a lot easier to roll with the conclusion after the process signals it.

I’m not submitting that I haven’t been run over by my signals once in a while. Nor am I suggesting that either the Sentiment Spread or the VIX/SPX signal are stand alone silver bullet signals. They are just two of the many tells I use instead of gnomes.

Just to roll through putting the aforementioned into action:

- On Friday morning, the SP500 was immediate-term TRADE oversold at 1540

- On Friday morning, the VIX was immediate-term TRADE overbought at 15.23

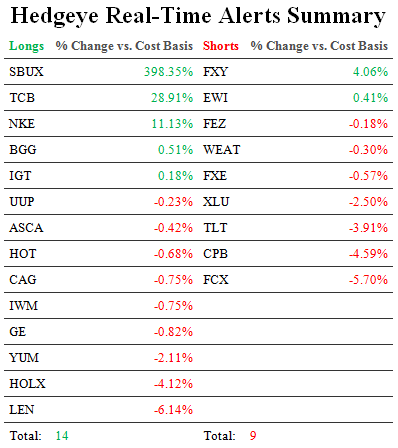

So, our #RealTimeAlerts (immediate-term signaling product) acted, aggressively on that, covering shorts and buying stocks (including the SPY itself). This is not about taking victory laps – this is about being accountable to what I do and why. I feel like putting my process out there like this makes it better. Sharp clients question it; so do my analysts internally. In the end, for me at least, that’s a win.

The other side of the buy/cover signal is to have the discipline to sell/short on the bounce. We’ve seen that for a few days since the Friday lows, and now, as the SP500 makes another all-time high, we’ll get another SPX overbought/VIX oversold signal too.

Will that happen at VIX 12.21 and SPX 1576? I don’t know. And that’s the point. Embracing Uncertainty in a non-linear and dynamic ecosystem like this is what I do. Stuff Changes. So I need to change alongside it.

Our immediate-term Risk Ranges for Gold, Oil (Brent), Copper, US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1544-1585, $103.86-107.78, $3.29-3.47, $82.23-83.34, 96.12-100.05, 1.71-1.82%, 12.21-14.51, and 1561-1576, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer