JNY is closing 225 of its 1000+ store base over the next 18 months. Did anyone even realize that JNY is one of the largest specialty retailers by door count? Even if you were aware that JNY is a retailer is disguise, it's very positive to see that they are no longer growing for the sake of growth. It's also positive to see management cutting its losses and moving on. We applaud the move to close over 20% of the store base for a few reasons:

1) Closing unproductive, loss producing stores has an immediate and positive impact on the P&L. In aggregate, JNY will save $37mm in losses and costs from closing these stores from '09-'11. This equates to $0.29 per share. Off of our new estimate of $0.65, this is substantial opportunity to help rebuild the earnings base

2) The cash cost to execute the store closing plan is only $5mm! That seems incredibly low and should make any rational person wonder why they didn't close store more aggressively in the recent past. Think about it, JNY gets to over half of the 20% number almost entirely by letting existing leases run off without renewing. Seems simple - but prior management has never made anything simple. Regardless of prior decisions or lack thereof, the net benefit of this effort is a no brainer.

3) Approximately 60% of the stores are mall-based, which leaves the base with a higher concentration of outlet stores. The outlet stores have recently been comping down only a few points while the mall based stores have been tracking down 20%. Outlets are a good compliment to a better distribution and inventory clearance strategy. Leave the mall-based selling to the department stores.

4) Inventories will come down further as the chain shrinks, freeing up additional working capital. This should be about a $30-$35mm reduction in working capital annually.

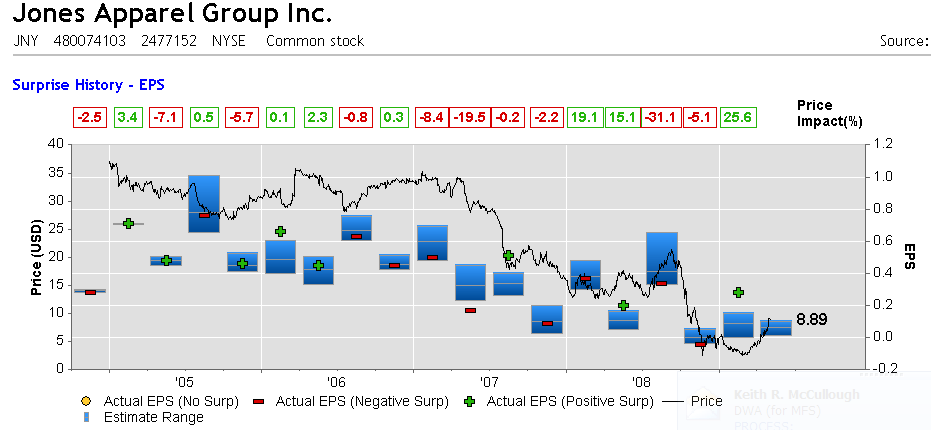

In JNY's case, addition by subtraction is not a cure-all for general market share loss and declining brand relevancy. However, we believe there is still upside in the nearer term as the business shrinks and expenses are once again leveraged. Of course, must of this is already in the shares which have now tripled from the March lows. Gains from here will have to come from measurable EPS improvement. But check out the estimate revision chart below. This company has faced 5-years of downward revisions (for good reason). The downside has stabilized, and my strong sense is that any recovery will last more than just a quarter or two. Don't get me wrong, I would not touch this name here. I'd much rather play LIZ for so many reasons. But if you're looking at jumping on the shorty bandwagon now on this perennially hated name - beware.

Eric Levine

Research Edge