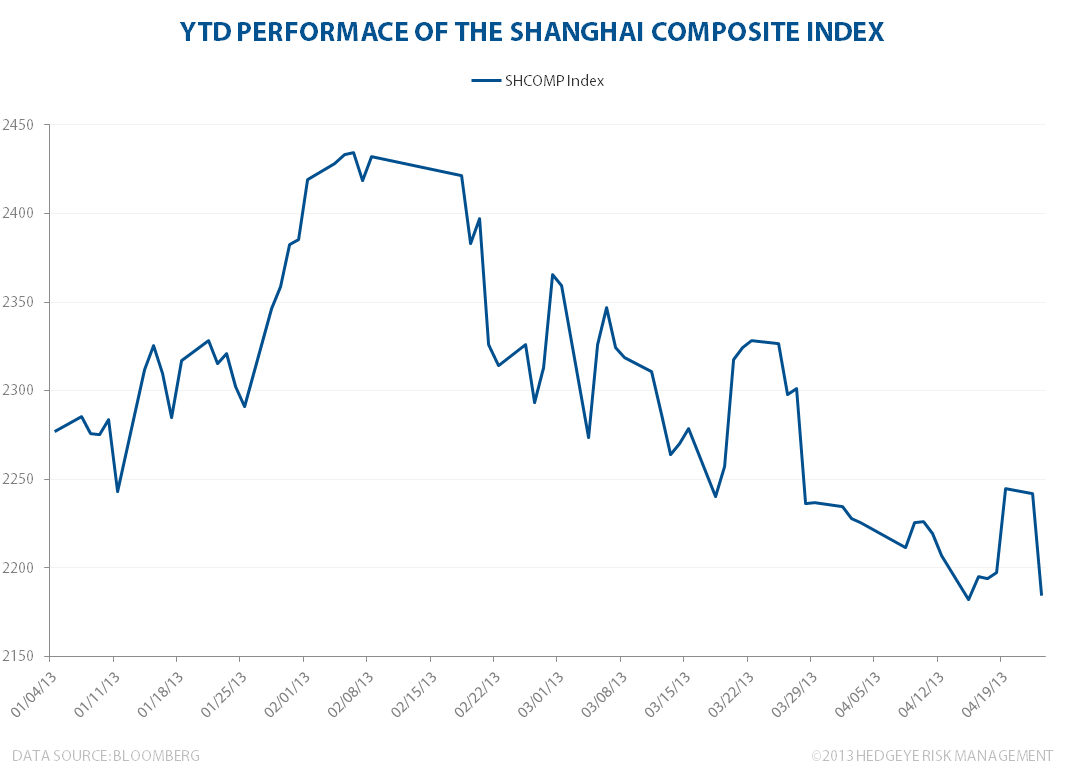

China is a big economic bubble ready to pop and this morning, it's looking like it may be ready to burst. Economic activity dried up with the Chinese Purchasing Managers Index (PMI) slowing sequentially to 50.5 versus 51.6 last month. In turn, Chinese stocks, which were moving to the upside constantly back in January, are taking a turn for the worse, with the Shanghai Composite Index closing down -2.2% this morning. As you can see in the chart below, Chinese stocks have been falling since Valentine's Day. No love for China? Apparently not.