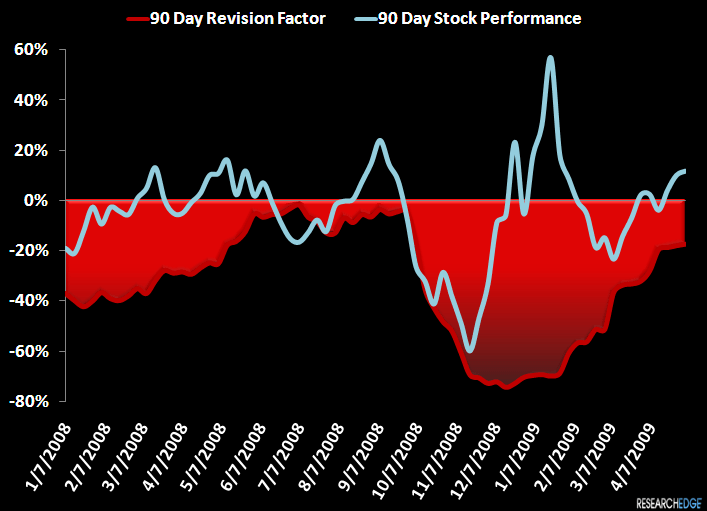

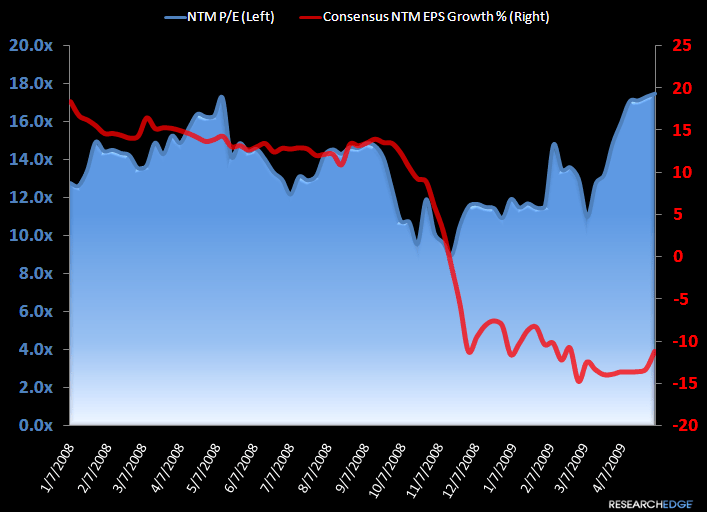

Another week passes where revisions are trending better, and the group is following suit. The major call-out, however, is that we're now sitting at peak valuations based on NTM consensus EPS estimates (17x).

The major question here for me is whether or not estimates are real. Has the sell-side finally overshot on the downside and what appears to be 17x earnings is actually something in the low teens?

In aggregate, I think that estimates are largely too low for the next 12-months, as our team has outlined since March 5th (We're Getting Fundamentally Bullish). But back then, it did not matter which names you played, as pretty much the whole group went up in unison.

The sector call still matters (check out Howard Penney's sector strategy work), but now, company-specific revisions matter a lot more than they did a month ago. If you're involved in a name and think that 'a miss is already in the stock,' then I feel for you come earnings day. There are lesser quality names that have set themselves up to smoke estimates in the upcoming quarters - such as CRI, JNY and SKX. Expectations are now lofty and I'm not convinced the upside is coming in a healthy way (setting up for shorts as '10 nears). Then there are others like UA, RL, HIBB, and HBI where I think the upside is meaningful AND warranted. PSS is another, with my lingering concern being the upcoming quarter. It won't be squeaky clean - which probably matters after double in the share price. I think that 2H estimates need to go up by almost half, so I'd keep that name front and center.