Friday’s earnings release from McDonald’s confirms our thesis that the magnitude of acceleration in same-restaurant sales that the Street is expecting in 2013 is unlikely to materialize.

History Repeating Itself?

Knowing that, in late 2003, the aggressive push for positive comparable sales growth via promotion of the dollar menu did not fix the underlying problems of the business, it seems clear that the current value message is merely a stop-gap measure for the recent slide in comparable sales growth. 2014 earnings estimates may be under threat if management is slow to respond to changes in the marketplace and unwilling to correct past mistakes. Part of a sustainable improvement in McDonald’s top line growth will be achieved through driving efficiency in the stores. Of late, sales initiatives seem to be adding to the complexity of the menu and dragging on store-level efficiency.

Addressing these issues will require investment and time and will also likely negatively impact operating margins and EPS over the near-term. The chart below implies that there is a disconnect between earnings expectations and the stock price. Taking the long-term perspective on same-restaurant sales into account, it seems unlikely that the earnings multiple can continue to expand from here.

Earnings

The last earnings call offered little in terms of incremental initiatives that the company is implementing to improve upon the 1Q13 global same-store sales number of -1%. The “three global priorities” of optimizing the menu, modernizing the customer experience, and broadening accessibility to “Brand McDonald’s” around the world comprise a message that is stale and, lately, ineffectual.

United States

1Q13 same-store sales declined -1.2% and operating income declined -3% but management stated that improved trends over the balance of the year will be driven by:

- Premium McWraps: with April same store sales still negative, the impact may not be sufficient

- Egg White Delight: according to GrubGrade 55% of consumer surveyed are NOT excited to try this product

- Blueberry Pomegranate Smoothies (imported from Canada)

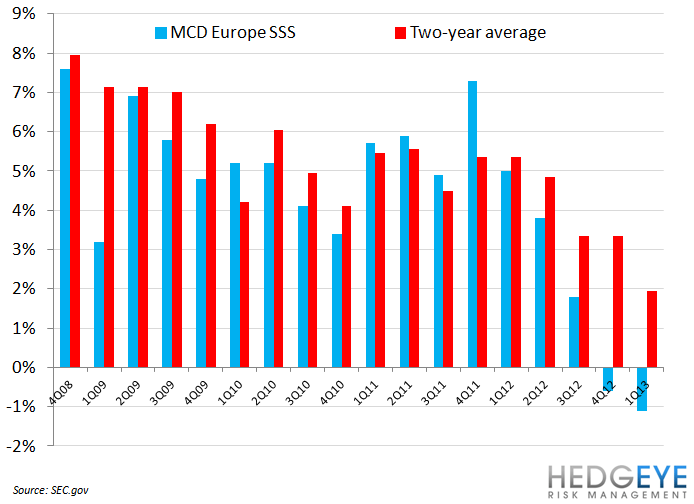

Europe

In 1Q13, same store sales were down 1.1 % and operating income was up 1% (in constant currencies). The countries that were weak in 2012 (Germany and France) continue to remain soft in 2013. The two countries that were strong in 2012 (U.K. and Russia) outperformed 1Q13, but their trends are slowing. Further complicating the problem, the decline in inflation in Russia is limiting the company’s pricing power. Importantly, the U.K. and Russia represent over half of the Europe division’s company-operated margin dollars.

Like the USA, Europe is also focused on value, but at the same time trying to feature premium products and promotions that try to get the consumer to trade-up and increase the average check. This strategy is not well suited for the current challenging consumer environment throughout most of Europe.

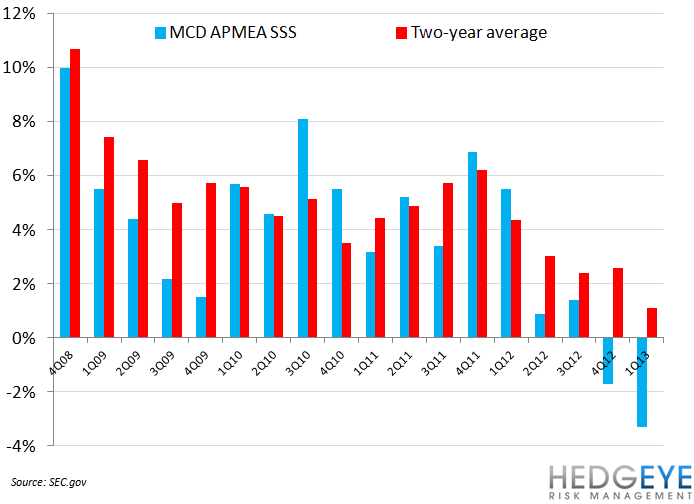

APMEA

While comparable sales were down 3.3 % for the quarter, operating income increased 2 % in constant currencies. Management’s comments highlighted the following:

- Continued emphasis on our value platforms

- Accelerating growth at breakfast (this requires changing consumer behavior)

- Enhancing service and convenience initiatives

In Australia (like Europe), management is trying to balance value initiatives with promotional activities that encourage trade-up. Japan's performance for the quarter was negatively impacted by the difficult economy and management is still trying to evaluate and adjust its plans to complement existing value initiatives. China saw same-store sales of -4.6 % in 1Q13 partly due to the residual effects of consumer sensitivity around the supply chain issue and the recent bird flu is also slowing a potential recovery.

Global Margin Pressure

Margin pressure will likely persist in 2013. In 1Q13 margins declined around the world for McDonald’s and there is no end in sight. The company specifically said they are in a market share battle and they intend to win, which suggests further margin pressure even if sales improve in 2H13. As we have said before, we do not see a sales recovery for MCD in 2H13.

Howard Penney

Managing Director

Rory Green

Senior Analyst