"Life only demands from you the strength that you possess. Only one feat is possible; not to run away."

-Dag Hammarskjold, Former Secretary General of the United Nations

Current Position: Long Sweden via EWD

Dag Hammarskjold was called by JFK "the greatest statesman of our century". This giant of a man is as emblematic of the Swedes as their picturesque fjords and championship winning national hockey teams are. As it relates to global stock market performance in 2009 year-to-date, Hammarskjold's quote is an accurate one. Currently, Sweden is one of the leaders in the global stock market performance race with its benchmark OMX Stockholm 30 Index up 17% MTD and 15.3% YTD.

Yesterday, we sold our long position in Germany, via the etf iShares EWG, for an 11% gain and turned around and bought Sweden, via the etf iShares EWD, with the etf down on the day. We like Sweden as a pair against our short position in Switzerland (EWL), which has a dysfunctional financial system.

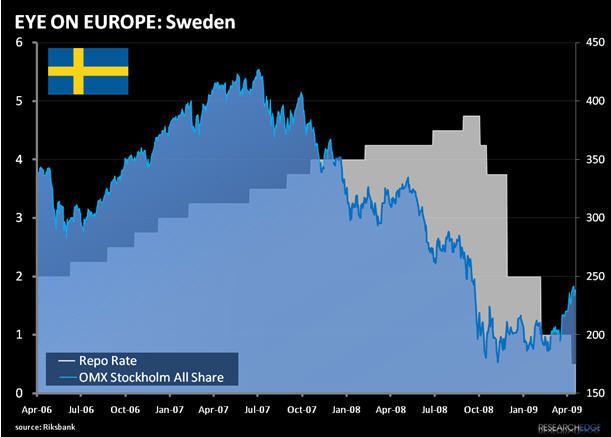

Alongside Germany, Sweden is one of a few countries that we feel pseudo comfortable with from a fundamental standpoint in Europe. Most of Europe has been battered by rising unemployment and budget deficits while output, exports, and consumer demand have crumbled. Strong deflationary pressure has become the norm across the region. Sweden's most recent CPI figure for March decreased to 0.2% Y/Y, the lowest rate in four years, which helped prompt the Swedish Central Bank (Riksbank) to reduce the interest (repo) rate 50bps to 0.5% on 4/21.

While the Swedish Central Bank has limited room to cut, the country has the balance sheet and tax levers to further stimulate. In addition, since it is not a member of the European Monetary Union (does not use the Euro), Sweden has the ability to be much more targeted with its stimulus package, worth $1 Billion or 3% of GDP.

Given its large public sector, with estimated tax revenue at ~47% of GDP, Sweden has inherent stabilizers that have and will allow it to offset the decline in private sector spending and activity that we have seen globally over the last 9 months. From an economic perspective, Sweden has limited exposure to commodity based industries. Specifically, only 2% of GDP is related to agriculture. The Swedes have a highly skilled and educated work force. Almost 50% of output and exports are accounted for by the engineering sector, which will be better shielded in a downturn.

We're bullish on the country's high net fiscal stimulus as a percent of GDP and surgical maneuvering to cut interest rates since Q4 '08 to blunt contraction and spur lending. Sweden's sovereign debt still holds a AAA credit rating from Fitch Ratings, despite tail risk surrounding Swedish banks, many of which were primary lenders to the Baltic states, countries that are now in the deepest recession within Europe.

We believe that strong exporting countries like Sweden and Germany likely stand to benefit more than their European peers from a global economic revival and we will trade Sweden opportunistically versus shorting more structurally challenged countries like the United Kingdom and Switzerland.

Daryl G. Jones

Managing Director

Matthew Hedrick

Analyst