TODAY’S S&P 500 SET-UP – April 22, 2013

As we look at today's setup for the S&P 500, the range is 36 points or 1.49% downside to 1532 and 0.82% upside to 1568.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

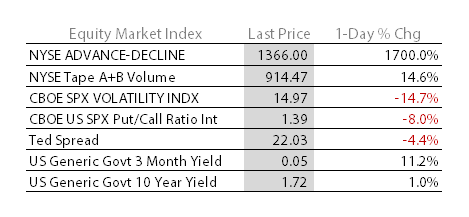

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.50 from 1.48

- VIX closed at 14.97 1 day percent change of -14.75%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Chicago Fed Nat Activity Index, March (prior 0.44)

- 8:30am: Fed’s Dudley speaks at economic conference in New York

- 10am: Existing Home Sales, March, est. 5m (prior 4.98m)

- 11am: Fed to purchase $3b-$3.75b notes in 2019-2020 sector

- 11:30am: U.S. to sell $32b 3M bills, $28b 6M bills

- U.S. Weekly Rates Agenda

GOVERNMENT:

- ITC may issue decision in Apple-Google patent dispute

- Senate Judiciary Cmte holds a hearing on legislation that would set up criteria for those now in U.S. illegally as step toward citizenship

- Secretary of State John Kerry attends NATO foreign ministers summit in Brussels

- Martin Dempsey, chairman of Joint Chiefs of Staff, visits Beijing as U.S. seeks greater Chinese pressure on N. Korea

- Washington Week Ahead

WHAT TO WATCH

- IMF talks over wknd included fight over new debt targets

- S&P early victory in U.S. ratings fraud suit seen as unlikely

- Dealers say no end to QE in 2013, Hatzius sees ’16 rates rise

- ABB to buy Power-One for $1b to add solar inverters

- ANA to finish 787 battery repairs by May after FAA approval

- Elan board unanimously rejects Royalty Pharma takeover offer

- Sales of U.S. existing homes probably climbed for 3rd month

- THQ files bankruptcy plan paying creditors from asset sales

- Bernanke to miss Jackson Hole symposium on schedule conflict

- Allstate said to seek offers for Lincoln Benefit business

- BP may delay development of GoM Mad Dog 2 oil field

- Netflix seen cracking down on acct sharing to bolster profit

- Argentina bondholder rejection sets up U.S. court ruling

- China Premier Li urges focus on rescue as quake toll mounts

- Mining in region was halted, Xinhua said; Toyota temporarily stopped production at Chengdu plant

- “Oblivion” is top weekend movie with $38m in NA sales

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Media/Ent, Real Estate, Transports

- North American M&A Agenda

- Canada Weekly Agendas: Energy, Mining

- Weekly Eco Preview: Growth in U.S. probably picked up in 1Q

- GDP, Apple, Exxon, BOJ, Iron Man 3: Wk Ahead April 22-27

EARNINGS:

- Hasbro (HAS) 6:30am, $0.04 - Preview

- Bank of Hawaii (BOH) 6am, $0.87

- Caterpillar (CAT) 7:30am, $1.38 - Preview

- Halliburton (HAL) 7am, $0.57 - Preview

- NVR (NVR) 8:50am, $7.86

- Lennox International (LII) 8am, $0.27

- Six Flags Entertainment (SIX) 8am, $(1.75)

- BancorpSouth (BXS) 4pm, $0.21

- Hexcel (HXL) 4pm, $0.41

- Swift Transportation (SWFT) 4pm, $0.16

- United Stationers (USTR) 4pm, $0.55

- Woodward (WWD) 4pm, $0.60

- Canadian National Railway (CNR CN) 4:01pm, $1.21 - Preview

- Ameriprise Financial (AMP) 4:05pm, $1.57

- Illumina (ILMN) 4:05pm, $0.38

- Netflix (NFLX) 4:05pm, $0.20 - Preview

- Rogers Communications (RCI/B CN) 4:05pm, C$0.77 - Preview

- Zions Bancorporation (ZION) 4:10pm, $0.40

- Rent-A-Center (RCII) 4:15pm, $0.87

- Texas Instruments (TXN) 4:30pm, $0.30

- Brookfield Canada Office (BOX-U CN) 5pm, C$0.39

- Packaging of America (PKG) 5pm, $0.56

- Crane (CR) 5:15pm, $1.03

- IDEX (IEX) 5:22pm, $0.71

- BBCN Bancorp (BBCN) Aft-mkt, $0.27

- MB Financial (MBFI) Aft-mkt, $0.42

- Pennsylvania REIT (PEI) Aft-mkt, $0.43

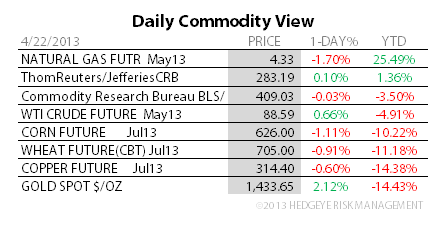

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Advances for Fifth Day in Longest Winning Streak This Year

- Hedge Fund Gold Wagers Defy Worst Slump in 33 Years: Commodities

- Brent Below $100 a Fifth Day as U.S. Funds Reduce Bullish Bets

- Copper Falls as Lower Imports Into China Stoke Demand Concern

- Sugar Falls as Investor Buying Fails to Spur Rally; Cocoa Gains

- China Sugar Stockpile Plan to Reduce Need for Imports, Jia Says

- Corn Slumps to One-Week Low on Demand Concerns for U.S. Grain

- Thai Sugar Premium Drops as Futures Rise in New York: Green Pool

- Shanghai Gold Exchange Benchmark Contract Volume Jumps to Record

- Bullish Crude Wagers Drop the Most in Two Months: Energy Markets

- Singapore’s SGX Said to Gauge Demand for LNG Futures Trading

- Tata Faces Crisis as $20 Billion Spent on Water: Corporate India

- WTI Crude May Rebound in Weekly ‘Triangle’: Technical Analysis

- N.Z. Set for More Rainfall as Residents Assess Weekend Damage

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

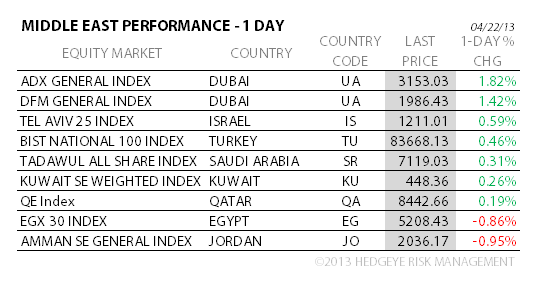

MIDDLE EAST

The Hedgeye Macro Team