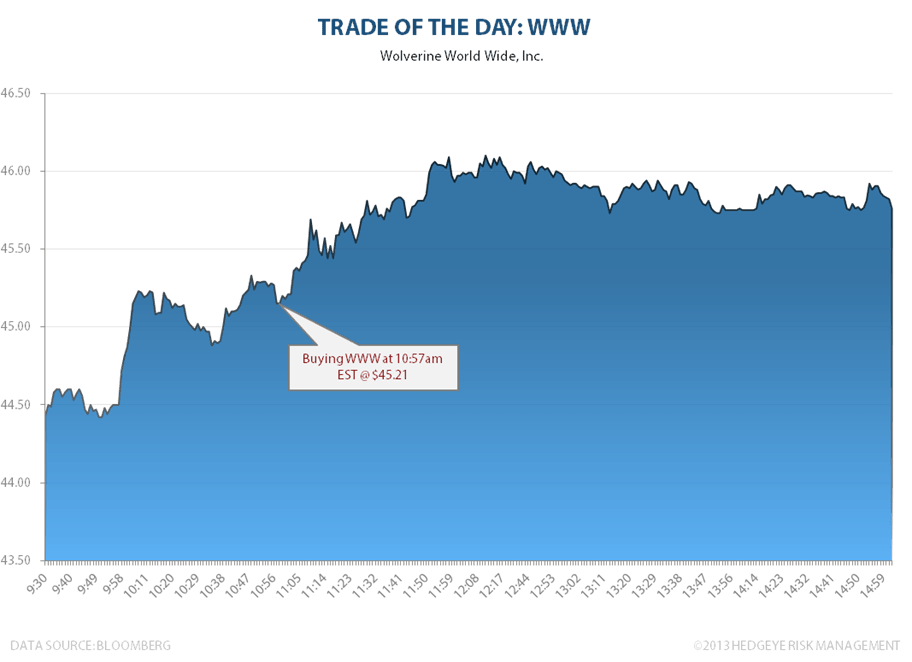

Today we bought Wolverine World Wide (WWW) at $45.21 a share at 10:57 AM EDT in our Real-Time Alerts. This is Hedgeye Retail Sector Head Brian McGough's latest Best Idea and we're adding it to our Institutional Best Ideas list today. Buying it on a sloppy #OldWall downgrade.